The Ticket

The TicketChoosing the Right Prediction and Predictor in the U.S.’s Ongoing Debt Crisis

This summer's debt ceiling crisis has come and gone, but the debt crisis continues. Congress narrowly avoided a government shutdown at the end of September and the prediction market Intrade now points to a non-negligible likelihood of a government shutdown at the end of the year.

Reporters have cited a great deal of data surrounding the debt controversy, but few news outlets did a good job delineating what the data was predicting. So it was hard for most people following the issue to determine which data they should be following, or which data mattered.

Much of the core confusion surfaced at the height of the battle over the debt ceiling. Media coverage essentially conflated four key questions with each other. First, would the debt ceiling be raised? Second, would the major credit agencies downgrade the paper that the United States held on its debt? Third, would the crisis make it more expensive for the United States to borrow money (i.e., higher interest rates) in either the short or long term? And finally, would the United States default on its debt?

These questions were all quite plainly inter-related: If the United States failed to raise the debt ceiling, that could mean deferred payments on the debt--and an ensuing downgrade of the nation's credit, thanks to a spike in short-term borrowing. And that downgrade should, in turn, correlate with a higher likelihood of default and thus higher long term borrowing costs.

Yet as the aftermath of the summer debt-ceiling showdown demonstrated, U.S. credit was downgraded even after the White House and Congress reach an accord to raise the ceiling. And the markets doubt whether downgrading was correlated with a higher likelihood of default.

So what has all this meant for ordinary Americans. The four questions that clustered around the debt furor break down into a clear hierarchy of importance for most people.

Most people suffered no direct fallout from Standard and Poor's decision to downgrade U.S. credit. Since major buyers of U.S. debt perform independent analyses of its quality, the judgment of rating agencies is far from the only force dictating the behavior of investors. There are better predictors of America's credit-worthiness or likelihood of default, as I will discuss below.

Regardless, if U.S. debt were downgraded drastically, say, to non-investment status, that action would trigger a huge automatic selloff of U.S. debt, clearly making it more expensive for the U.S. to borrow in the long term. But this summer's reclassification of American debt from AAA to some form of AA proved to be relatively unimportant to most people.

This is, of course, all in sharp contrast to things such as mortgage backed securities, which had been filled with unsecured subprime loans or worse--and which produced very little in the way of independent analysis. In that market a downgrade became an unmistakable warning sign--a huge indicator of potential default, spurring investors to stop providing low-interest loans to such securities.

As for the shorter-term debt picture, a failure to raise the debt ceiling would have, at least, meant the U.S. would have had to defer some payments; although many observers assumed that America would pay off debt obligations ahead of any other payments. A viable solution to the debt crisis was, in other words, a critically important matter for anyone expecting regular checks from the U.S. Treasury, such as Medicare and Social Security recipients. As matters played out, however, the volatile state of the country's short-term debt produced greater longer-term fallout for the political actors , and no serious consequences for the millions of Americans expecting regular checks from the Treasury.

So much for the first two main questions in the debt imbroglio. The third such question--concerning the interest rates available to the U.S. Treasury--bore enormous potential consequences for ordinary Americans. That's because the present deficits Washington is now running up create a huge ripple effect for any shift in the price of borrowing. Once you pile additional debt onto a $10 trillion borrowing tab--whose interest rates alone now make up about 6.1 percent of the federal government's budget to service. "Since the United States will continue to borrow money to finance expenditures in the near term, any increase in the cost of borrowing will have a large effect on the national debt", notes Rob Ready, an Assistant Professor of Finance at the University of Rochester.

Any U.S. default in this scenario would create enormous, direct effects on recipients of checks from the Treasury--and for everyone with a stake in U.S. debt and currency. In short, that means everyone. As the arcane particulars of the debt showdown played out, what most concerned citizens beyond the Beltway was the prospect of and actual U.S. default, which in turn create long-term increases in the cost of U.S. borrowing.

This may sound obvious--but whenever you see a prediction, think carefully about what it is actually predicting. Prediction markets, which assess the likelihood that upcoming events will or will not occur, expend a great deal of virtual ink on the details of seemingly straightforward prediction. To take one related example, consider the rules associated with Intrade's market sizing up the chances that California will default on its debt by the end of the year. Intrade now gives this outcome a negligible likelihood. And in spelling out the rules governing that call, InTrade lists six different, specific events that would constitute a default. Other prospective indicators of future outcomes and market behaviors aren't as carefully designed to yield solid predictions--and as a result, interpreters have to handle their direct implications with care.

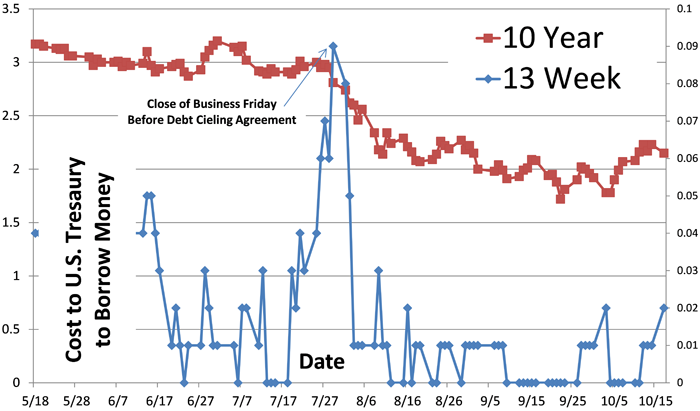

For instance, the 13-week Treasury Bill proved to be a meaningful indictor of whether the negotiations to raise the debt ceiling were going well. At the height of the debt-ceiling crisis, such loans cost the government more. That meant that short term Treasury bills peaked during the weekend of the final negotiations and plummeted after the deal was struck. The market's message was fairly easy to read in this instance: Failing to raise the debt limit would harm the value of short-term U.S. debt--either because the United States would defer payments until the crisis was resolved, or because America would actually default on the debt.

Note: 10 Year is CBOE Interest Rate 10-Year T-No (^TNX) and 13 Week is 13-Week Treasury Bill (^IRX)

Meanwhile, the cost of long-terms loans for the U.S. government, 10 and 30 year treasury notes, continued to go down throughout this crisis. This, too, is a trend that's very simple to interpret: People commonly flock to longer-term government securities when other investing options start to look volatile and risky, and their fairly consistent performance over the course of the debt ceiling furor meant that investors weren't especially spooked by all the high drama in Washington. In other words, investors didn't see the long term solvency of the U.S. Treasury being significantly at risk.

Any increased likelihood of default would affect the cost of servicing the nation's long term debt; therefore, the market was placing the likelihood of such a default as negligible. "The United States would never default on dollar denominated debt because we can always print money," Ready said. "This is opposed to Greece, which is stuck with the Euro and so will actually default if they cannot make a payment--or, in the same way, California."

There actually is a direct market for U.S. default, which trades in America's credit default swaps--i.e., bets on the likelihood of an actual default. And while it's true that the cost of credit default swaps went up during the crisis, there are several problems with this market. First, most people are under the impression that United States would have a grace period of a few days in a default scenario--meaning that it would take any late payment outside that grace period to trigger a credit default swap. In other words, default-swap markets were partially indicating a deferred payment as well as a default.

Another problem with the default market is that it is not very liquid, with just about $5.5 billion in net coverage, in 1,505 contracts, for more than $10 trillion in outstanding debt. There's also the problem of the market's own clear interest in sidestepping a collapsed debt ceiling. If a massive crisis forced the United States actually to default, institutions providing default swaps as a means of insuring investors against debilitating risk would be ruined--as AIG famously was during the 2008 mortgage meltdown. And that would mean, in turn, they couldn't make good on their outstanding paper, lowering the value of any credit-default policy. Credit default swaps are better indicators of late payments, such as 13-week Treasury Bills, rather than actual default indicators like the market for 10- and 30-year Treasury Notes.

Even though the ins and outs of markets in debt speculation can be quite arcane, the overall lesson here applies with strikingly parallel force to the markets for election predictions. In that world, most people closely followed the latest poll of voter intention as a prime indicator of future outcomes. Now, it is relatively easy to translate those poll numbers into a probability of victory, but no one bothered to do so until recently. Further, polls of voter intention suffer from well-known biases relative to the expected vote share that are also easy to correct. Yet, only in the last few cycles have people been more aggressive about aggregating polls and turning them into expected vote shares.

Likewise, all indicators in the debt crisis pointed to a political dustup that presented very few long-term, real-word consequences for things that genuinely concern most people. Yet press coverage of the crisis often lost sight of both the kinds of outcomes that would really matter in people's lives, and which indicators people could productively consult to learn of likely outcomes. And in both instances, ordinary citizens should keep in mind a simple caveat lector disclaimer: Always think about what you really want to know--and about what the information you are seeing is actually telling you.

David Rothschild is an economist at Yahoo! Research. He has a Ph.D. in applied economics from the Wharton School of Business at the University of Pennsylvania. His dissertation is in creating aggregated forecasts from individual-level information. Follow him on Twitter @DavMicRot and email him at PredictionBlogger@Yahoo.com.