2 Incredibly Cheap Bank Stocks

The past year hasn't been very good to bank investors. The SPDR S&P Bank ETF (NYSEMKT: KBE), which tracks the banking entities in the S&P 500, is down 14% over the past year, compared to 6.7% in gains for the S&P 500 over the same period. In short, Mr. Market continues to have a dim outlook for bank stocks in the near term.

And that view is for good reason. The U.S. Federal Reserve recently held firm on its benchmark overnight lending rate while indicating it may not raise rates later this year, either. And while keeping rates steady is good for both consumers and businesses, the Fed's move sends a clear signal that its governing body has concerns about the U.S. economic outlook and jobs picture.

By nearly any measure, these two bank stocks are cheap today. Image source: Getty Images.

Yet even within the noise of this short-term worry, there's a clear opportunity for investors with a long-term outlook to buy some great banks at discounted valuations. Two that look especially cheap at recent prices are Axos Financial (NYSE: AX) and Bank of America (NYSE: BAC). Here's a closer look at what makes them attractive at recent prices, and why investors would do well to buy now.

This online bank's surprising advantage

Axos Financial has been considered a big innovator because of its online-only presence. Its branchless model is a competitive advantage, giving it some of the cheapest operating costs you'll find.

For instance, Axos' efficiency ratio -- which measures how much of its revenue goes to operating expenses -- was 46.5% in its most recent quarter. That's up from 40.6% (lower is better) from last year, but Axos still sports a much more efficient operating profile than banks with retail branches.

For comparison, Bank of America's efficiency ratio was 58% last quarter, an improvement from 62% year over year. To be clear, that's a good efficiency ratio for a commercial bank, but BofA spends about 25% more of its revenue than Axos does to fund operations.

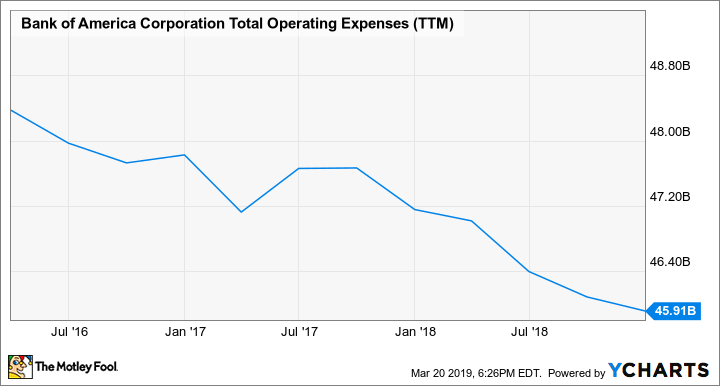

But that efficiency advantage isn't likely to prove durable over time. BofA is an excellent example of why, having closed underutilized branches and prioritized its online platform, driving costs down significantly in recent years:

BAC Total Operating Expenses (TTM) data by YCharts

Don't get me wrong: Axos' lower expense ratio today is an advantage since it means more retained cash to invest toward growth. It's just not likely to prove sustainable.

But what sets Axos apart is its executive leadership, particularly CEO Greg Garrabrants. When Garrabrants took over as CEO in 2007, Axos (then BofI Holding) was essentially a Southern California jumbo mortgage lender. This was right at the cusp of the Global Financial Crisis.

Fast-forward 11 years, and Axos not only survived the Great Recession but has also grown earnings nearly 3,000% while expanding its business across the gamut of commercial banking. And having only recently reached $10 billion in assets, it remains a small bank, with quite strong growth prospects.

Here's the kicker: Investors can buy this high-quality, growing bank for less than 12 times earnings and about 1.9 times book value. Axos has rarely traded for those multiples in recent years:

AX PE Ratio (TTM) data by YCharts

Combined with its growth potential, beneficial structure, and excellent management, Axos' current valuation is dirt cheap.

BofA is still undervalued

Based on its book value multiple and the historical price investors have been willing to pay, Bank of America may not look particularly cheap:

BAC Price to Book Value data by YCharts

That's particularly true after I just spent a few hundred words using that argument to call Axos Financial cheap. But these are two very different banks, with two very different recent histories.

While Axos emerged from the Financial Crisis mostly unscathed, BofA spent most of the past decade as one of the most hated companies in America, paying tens of billions in fines and legal settlements for a litany of bad practices. And until the last of its major legal issues was resolved in 2017, investors -- rightfully -- would only buy BofA at a discount to its book value.

Since taking over in 2010, CEO Bryan Moynihan has led it through a remarkable turnaround. It has closed hundreds of underutilized branches and reduced costs substantially, while also developing one of the best-regarded online banking platforms in the industry that its customers have embraced: Mobile banking usage was up 16% last quarter.

Simply put, plenty of customers now love BofA, or at the very least find its ease of use sticky enough to not move their accounts somewhere else, as its 5% deposit growth last quarter shows.

But the biggest proof of BofA's turnaround is its rates of return:

BAC Return on Equity (TTM) data by YCharts

With the financial impact of its past indiscretions paid and done, and Moynihan's strategy to leverage online banking and cut low-performing branches reducing expenses, Bank of America's returns have gone from well below the 10% and 1% benchmarks for a bank's return on equity and return on assets, respectively, to well above.

Today's book value multiple is higher than it was a few years ago, but for very good reason: Its legal exposure is substantially reduced, and its profitability is substantially increased. And 1.1 times book value is pretty cheap, considering the returns BofA is getting from those assets.

Furthermore, its earnings multiple is also bargain-bin levels, trading for 11 times 2018 earnings and 9.9 times expected 2019 earnings.

Two excellent "buy on the dip" deals in banking

Whether measured by stock price, earnings, or book value, both Axos and Bank of America shares trade for steep discounts to fair valuations, and are far lower than investors happily paid at their recent highs. And it's almost entirely due to the market's concerns over near-term things that aren't likely to have lasting implications for either. That makes both excellent buys for opportunistic investors looking for a long-term payoff.

Whether you're looking for the deeper value represented in Bank of America, or the low price for the growth prospects represented in Axos Financial, both are cheap today, and with top-tier management that should lead them to better -- and more profitable -- years to come.

More From The Motley Fool

Jason Hall owns shares of Axos Financial and Bank of America. The Motley Fool owns shares of and recommends Axos Financial. The Motley Fool has a disclosure policy.