2 Stocks to Buy That Have Dividends Yielding More Than 5%

Wall Street is near a record high, but the S&P 500 Index is offering a paltry 1.8% yield. It seems like the only way to find a good yield is to step out on the risk spectrum.

But if you look hard enough, you can find some high-yielding names where the risk/reward trade-off looks like it's skewed in your favor. Two names to look at are oil major Royal Dutch Shell (NYSE: RDS-B) and midstream stalwart Magellan Midstream Partners (NYSE: MMP). Here's a primer to get you started.

Solid plans for the future

Royal Dutch Shell is one of the world's largest integrated energy companies, with operations that span the upstream (oil and natural gas drilling), midstream (pipeline), and downstream (refining and chemicals) sectors. And it's now focused on building up a large electricity business that it hopes will someday rival its other operations in size. The company is hoping to be a diversified global energy company and not just an oil company, so it can better compete in the changing energy market.

Image source: Getty Images.

The stock offers investors a fat 5.7% yield, partly because it operates in the volatile oil sector. Although the dividend hasn't been increased in a few years, management recently laid out a robust plan for returning cash to shareholders.

In the near term, Royal Dutch Shell will be focusing on buying back stock, but longer term, dividends will start to take on more importance. Until then, management appears strongly committed to supporting the current payment. The company boasts a reasonable debt-to-equity ratio of around 0.34, so there's no reason to doubt it can keep paying.

On the growth front, management has plans to invest around $30 billion a year through 2025. Around $20 billion of that is sustaining capital spending, with the rest focused on growth across the entire business.

Notably, Royal Dutch Shell is emphasizing oil and gas projects with low break-even points -- around $30 per barrel of oil -- to ensure that its business is robust in the face of volatile commodity markets. With the company projecting around $35 billion in free cash flow annually, it should have no problem hitting the high end of its spending goals, while sustaining capital spending should be achievable, even if oil prices fall.

All the while, the company will be diversifying into electricity to protect itself from the larger move toward clean energy sources. That's a balanced plan that should comfortably allow investors to collect Shell's over-5% yield while it plays out.

Slow and steady

Magellan is a midstream limited partnership that's pretty much the epitome of slow and boring. That's not a negative, though, since even more aggressive investors should be happy to sit back and collect the fat 6.1% yield offered here. And that yield is backed largely by fee-based assets where cash flow is reliant on the demand for energy, not commodity prices. So Magellan's business is pretty solid and should remain that way for a long time.

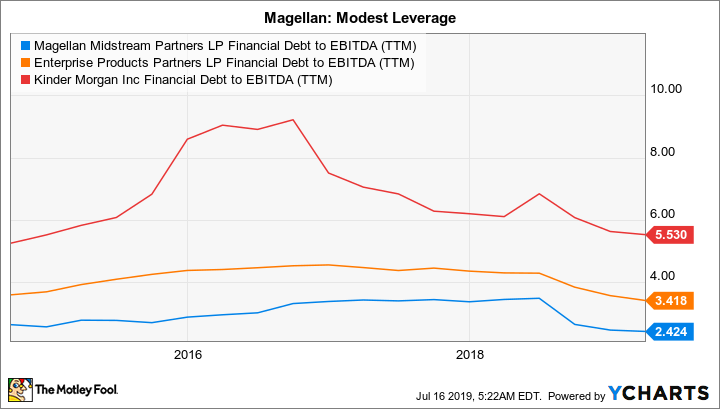

The partnership's conservative approach, meanwhile, has allowed it to raise the distribution every single quarter since it came public in 2001. It covers the distribution by around 1.2 times, which is a strong number in the midstream space. And Magellan's use of leverage is modest relative to peers, so there's little reason to doubt it can support the current distribution.

MMP Financial Debt to EBITDA (TTM) data by YCharts.

The question mark here is the potential for distribution growth. Magellan is targeting mid-single-digit growth but recently canceled some projects. So it has $1.1 billion in spending planned for 2019 but just $150 million in 2020. That has investors worried and is putting a damper on the shares.

But this is an opportunity, since the partnership has a sterling track record when it comes to growing its business over time. Sure, there may be a lull today, but Magellan deserves the benefit of the doubt based on its strong history. And investors will get paid handsomely for sticking around via the well-supported distribution while the partnership works to fill the project pipeline with new growth-enhancing opportunities.

Risks worth taking

If you're looking for large dividend yields, you have to think carefully about what you buy. You can take on big risks to get big yields or step it back just a little and get sizable 5%-plus yields from companies that have the financial strength to keep paying (and perhaps growing) them.

Royal Dutch Shell and Magellan fall into that second category, and I think they're well worth the far-more-modest risks they're dealing with. As I see it, even conservative income investors can feel comfortable considering Royal Dutch Shell and Magellan for their portfolios.

More From The Motley Fool

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool recommends Magellan Midstream Partners. The Motley Fool has a disclosure policy.