These 4 Measures Indicate That Cortina Holdings (SGX:C41) Is Using Debt Safely

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about. So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Cortina Holdings Limited (SGX:C41) does carry debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Cortina Holdings

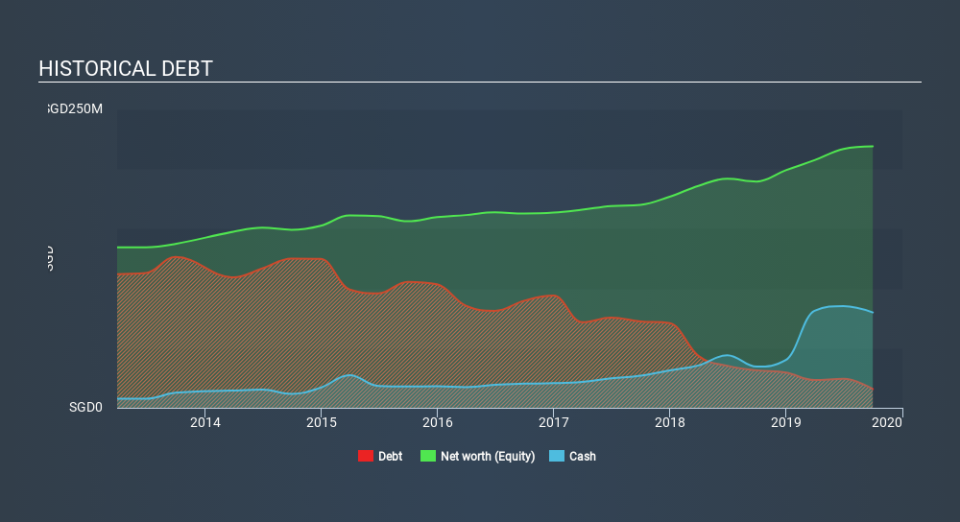

What Is Cortina Holdings's Net Debt?

You can click the graphic below for the historical numbers, but it shows that as of September 2019 Cortina Holdings had S$15.7m of debt, an increase on S$31.5, over one year. However, it does have S$79.9m in cash offsetting this, leading to net cash of S$64.2m.

A Look At Cortina Holdings's Liabilities

We can see from the most recent balance sheet that Cortina Holdings had liabilities of S$80.3m falling due within a year, and liabilities of S$37.6m due beyond that. On the other hand, it had cash of S$79.9m and S$20.5m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by S$17.5m.

Of course, Cortina Holdings has a market capitalization of S$283.1m, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. While it does have liabilities worth noting, Cortina Holdings also has more cash than debt, so we're pretty confident it can manage its debt safely.

On top of that, Cortina Holdings grew its EBIT by 48% over the last twelve months, and that growth will make it easier to handle its debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is Cortina Holdings's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. Cortina Holdings may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last three years, Cortina Holdings actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing up

While it is always sensible to look at a company's total liabilities, it is very reassuring that Cortina Holdings has S$64.2m in net cash. The cherry on top was that in converted 174% of that EBIT to free cash flow, bringing in S$84m. So we don't think Cortina Holdings's use of debt is risky. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Consider for instance, the ever-present spectre of investment risk. We've identified 1 warning sign with Cortina Holdings , and understanding them should be part of your investment process.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.