These 4 Measures Indicate That Kurgan Generation (MCX:KGKC) Is Using Debt Reasonably Well

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Public Joint Stock Company Kurgan Generation Company (MCX:KGKC) makes use of debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Kurgan Generation

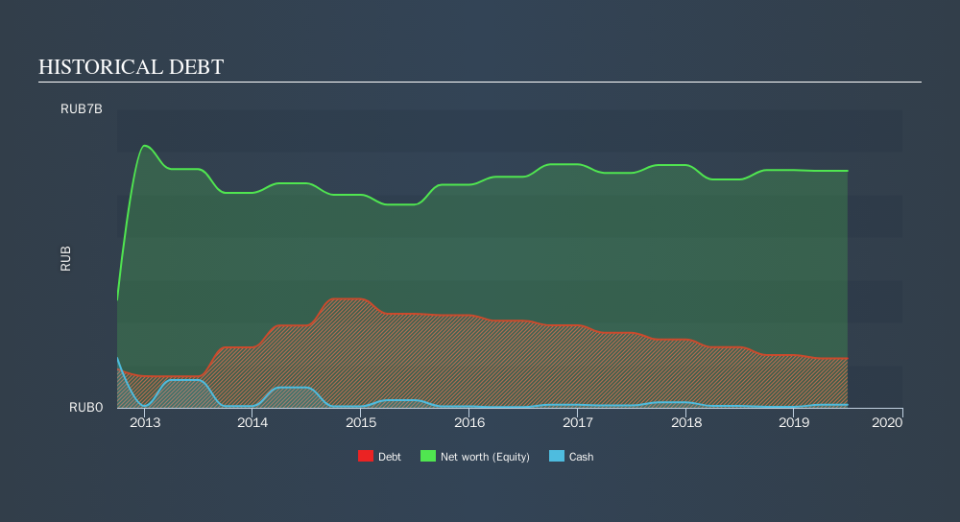

How Much Debt Does Kurgan Generation Carry?

As you can see below, Kurgan Generation had RUруб1.16b of debt at June 2019, down from RUруб1.43b a year prior. However, it does have RUруб72.7m in cash offsetting this, leading to net debt of about RUруб1.09b.

How Strong Is Kurgan Generation's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Kurgan Generation had liabilities of RUруб2.18b due within 12 months and liabilities of RUруб2.90b due beyond that. Offsetting these obligations, it had cash of RUруб72.7m as well as receivables valued at RUруб2.38b due within 12 months. So it has liabilities totalling RUруб2.63b more than its cash and near-term receivables, combined.

This deficit isn't so bad because Kurgan Generation is worth RUруб9.06b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Kurgan Generation has net debt of just 0.88 times EBITDA, indicating that it is certainly not a reckless borrower. And this view is supported by the solid interest coverage, with EBIT coming in at 7.5 times the interest expense over the last year. It was also good to see that despite losing money on the EBIT line last year, Kurgan Generation turned things around in the last 12 months, delivering and EBIT of RUруб848m. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Kurgan Generation will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. In the last year, Kurgan Generation's free cash flow amounted to 35% of its EBIT, less than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

Kurgan Generation's interest cover was a real positive on this analysis, as was its net debt to EBITDA. On the other hand, its conversion of EBIT to free cash flow makes us a little less comfortable about its debt. It's also worth noting that Kurgan Generation is in the Water Utilities industry, which is often considered to be quite defensive. When we consider all the factors mentioned above, we do feel a bit cautious about Kurgan Generation's use of debt. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of Kurgan Generation's earnings per share history for free.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.