These 4 Measures Indicate That LPA Group (LON:LPA) Is Using Debt Extensively

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that LPA Group Plc (LON:LPA) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for LPA Group

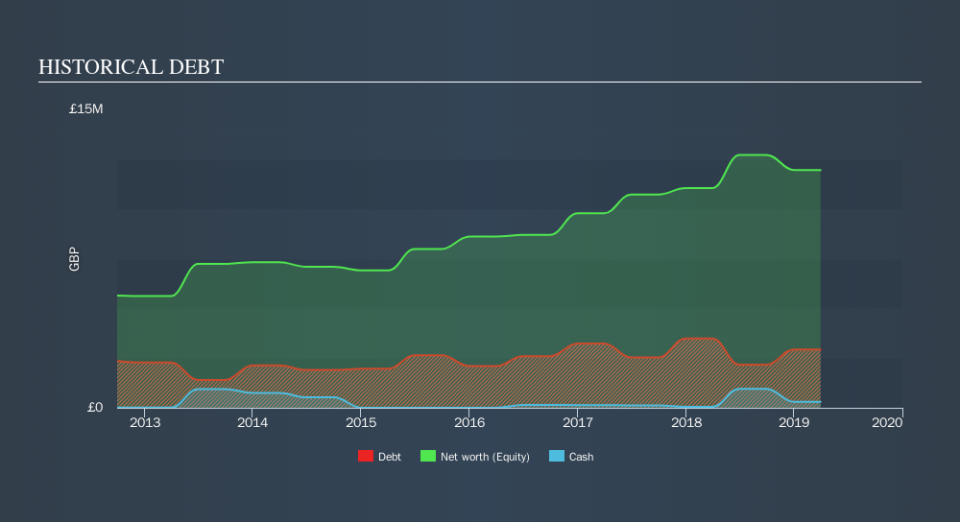

How Much Debt Does LPA Group Carry?

You can click the graphic below for the historical numbers, but it shows that LPA Group had UK£2.17m of debt in March 2019, down from UK£3.49m, one year before. However, it also had UK£304.0k in cash, and so its net debt is UK£1.87m.

How Strong Is LPA Group's Balance Sheet?

According to the last reported balance sheet, LPA Group had liabilities of UK£4.24m due within 12 months, and liabilities of UK£2.79m due beyond 12 months. On the other hand, it had cash of UK£304.0k and UK£4.80m worth of receivables due within a year. So its liabilities total UK£1.92m more than the combination of its cash and short-term receivables.

Given LPA Group has a market capitalization of UK£11.8m, it's hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

LPA Group's net debt is only 0.92 times its EBITDA. And its EBIT covers its interest expense a whopping 20.8 times over. So we're pretty relaxed about its super-conservative use of debt. The modesty of its debt load may become crucial for LPA Group if management cannot prevent a repeat of the 41% cut to EBIT over the last year. When it comes to paying off debt, falling earnings are no more useful than sugary sodas are for your health. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if LPA Group can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. Looking at the most recent three years, LPA Group recorded free cash flow of 25% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Our View

Neither LPA Group's ability to grow its EBIT nor its conversion of EBIT to free cash flow gave us confidence in its ability to take on more debt. But its interest cover tells a very different story, and suggests some resilience. Looking at all the angles mentioned above, it does seem to us that LPA Group is a somewhat risky investment as a result of its debt. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. Given LPA Group has a strong balance sheet is profitable and pays a dividend, it would be good to know how fast its dividends are growing, if at all. You can find out instantly by clicking this link.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.