These 4 Measures Indicate That Wing Tai Holdings (SGX:W05) Is Using Debt Extensively

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk. So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Wing Tai Holdings Limited (SGX:W05) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Wing Tai Holdings

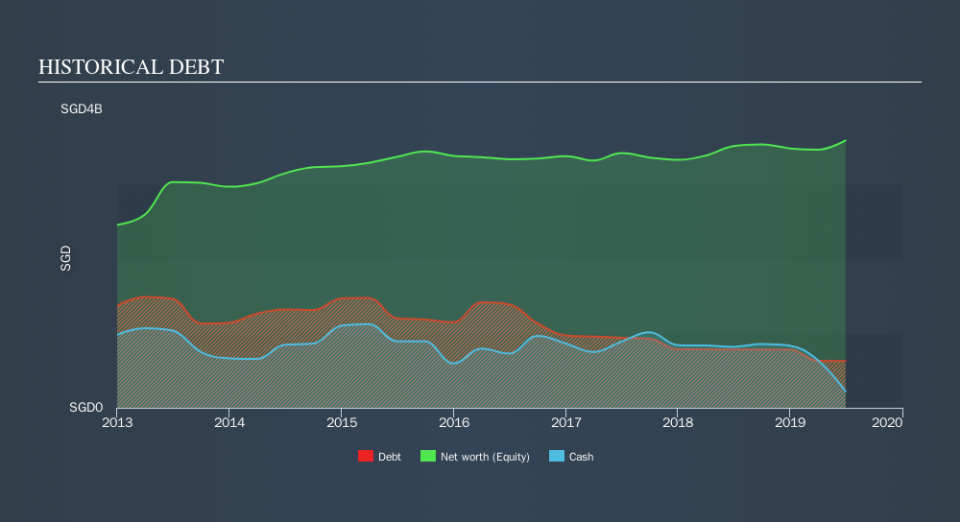

What Is Wing Tai Holdings's Net Debt?

The image below, which you can click on for greater detail, shows that Wing Tai Holdings had debt of S$627.1m at the end of June 2019, a reduction from S$780.1m over a year. However, it also had S$221.6m in cash, and so its net debt is S$405.5m.

How Healthy Is Wing Tai Holdings's Balance Sheet?

According to the last reported balance sheet, Wing Tai Holdings had liabilities of S$95.7m due within 12 months, and liabilities of S$681.3m due beyond 12 months. Offsetting this, it had S$221.6m in cash and S$1.14b in receivables that were due within 12 months. So it actually has S$582.5m more liquid assets than total liabilities.

This luscious liquidity implies that Wing Tai Holdings's balance sheet is sturdy like a giant sequoia tree. On this basis we think its balance sheet is strong like a sleek panther or even a proud lion.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Wing Tai Holdings shareholders face the double whammy of a high net debt to EBITDA ratio (38.8), and fairly weak interest coverage, since EBIT is just 0.12 times the interest expense. This means we'd consider it to have a heavy debt load. Worse, Wing Tai Holdings's EBIT was down 92% over the last year. If earnings continue to follow that trajectory, paying off that debt load will be harder than convincing us to run a marathon in the rain. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Wing Tai Holdings can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. During the last two years, Wing Tai Holdings burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

To be frank both Wing Tai Holdings's conversion of EBIT to free cash flow and its track record of (not) growing its EBIT make us rather uncomfortable with its debt levels. But on the bright side, its level of total liabilities is a good sign, and makes us more optimistic. Overall, we think it's fair to say that Wing Tai Holdings has enough debt that there are some real risks around the balance sheet. If everything goes well that may pay off but the downside of this debt is a greater risk of permanent losses. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of Wing Tai Holdings's earnings per share history for free.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.