These 4 Measures Indicate That XPO Logistics Europe (EPA:XPO) Is Using Debt Reasonably Well

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about. So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, XPO Logistics Europe SA (EPA:XPO) does carry debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for XPO Logistics Europe

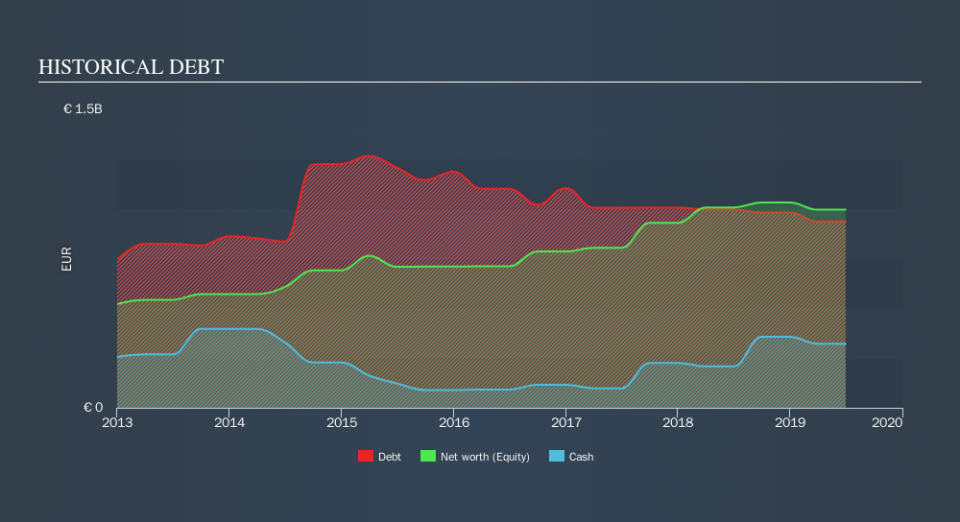

What Is XPO Logistics Europe's Debt?

You can click the graphic below for the historical numbers, but it shows that XPO Logistics Europe had €936.7m of debt in June 2019, down from €1.14b, one year before. On the flip side, it has €321.6m in cash leading to net debt of about €615.1m.

A Look At XPO Logistics Europe's Liabilities

The latest balance sheet data shows that XPO Logistics Europe had liabilities of €2.65b due within a year, and liabilities of €1.60b falling due after that. Offsetting these obligations, it had cash of €321.6m as well as receivables valued at €1.83b due within 12 months. So it has liabilities totalling €2.10b more than its cash and near-term receivables, combined.

This deficit is considerable relative to its market capitalization of €2.90b, so it does suggest shareholders should keep an eye on XPO Logistics Europe's use of debt. This suggests shareholders would heavily diluted if the company needed to shore up its balance sheet in a hurry.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

XPO Logistics Europe's net debt is sitting at a very reasonable 1.5 times its EBITDA, while its EBIT covered its interest expense just 3.4 times last year. While these numbers do not alarm us, it's worth noting that the cost of the company's debt is having a real impact. Unfortunately, XPO Logistics Europe saw its EBIT slide 4.4% in the last twelve months. If earnings continue on that decline then managing that debt will be difficult like delivering hot soup on a unicycle. When analysing debt levels, the balance sheet is the obvious place to start. But it is XPO Logistics Europe's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, XPO Logistics Europe recorded free cash flow worth a fulsome 94% of its EBIT, which is stronger than we'd usually expect. That puts it in a very strong position to pay down debt.

Our View

When it comes to the balance sheet, the standout positive for XPO Logistics Europe was the fact that it seems able to convert EBIT to free cash flow confidently. However, our other observations weren't so heartening. For instance it seems like it has to struggle a bit to cover its interest expense with its EBIT. When we consider all the factors mentioned above, we do feel a bit cautious about XPO Logistics Europe's use of debt. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. Over time, share prices tend to follow earnings per share, so if you're interested in XPO Logistics Europe, you may well want to click here to check an interactive graph of its earnings per share history.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.