Should You Be Adding Choice Properties Real Estate Investment Trust (TSE:CHP.UN) To Your Watchlist Today?

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in Choice Properties Real Estate Investment Trust (TSE:CHP.UN). While profit isn't the sole metric that should be considered when investing, it's worth recognising businesses that can consistently produce it.

See our latest analysis for Choice Properties Real Estate Investment Trust

How Fast Is Choice Properties Real Estate Investment Trust Growing Its Earnings Per Share?

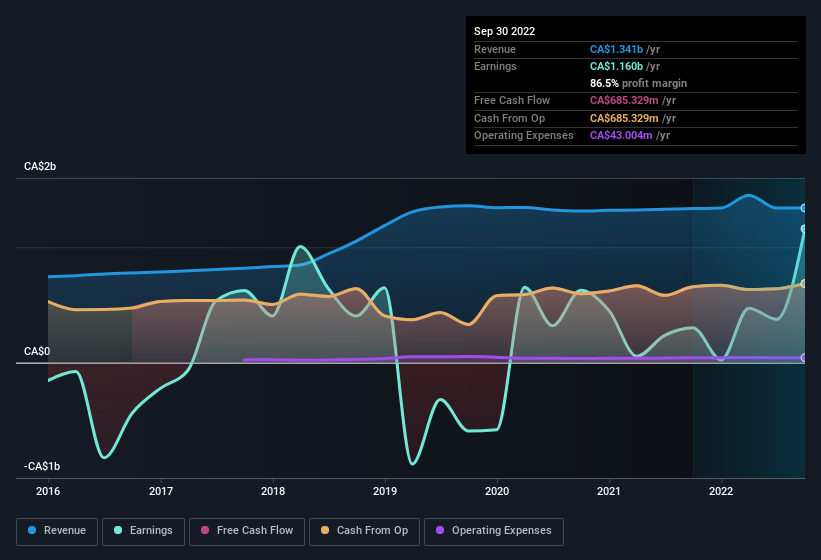

Strong earnings per share (EPS) results are an indicator of a company achieving solid profits, which investors look upon favourably and so the share price tends to reflect great EPS performance. So for many budding investors, improving EPS is considered a good sign. It's an outstanding feat for Choice Properties Real Estate Investment Trust to have grown EPS from CA$0.92 to CA$3.54 in just one year. Even though that growth rate may not be repeated, that looks like a breakout improvement.

It's often helpful to take a look at earnings before interest and tax (EBIT) margins, as well as revenue growth, to get another take on the quality of the company's growth. Our analysis has highlighted that Choice Properties Real Estate Investment Trust's revenue from operations did not account for all of their revenue in the previous 12 months, so our analysis of its margins might not accurately reflect the underlying business. It seems Choice Properties Real Estate Investment Trust is pretty stable, since revenue and EBIT margins are pretty flat year on year. That's not bad, but it doesn't point to ongoing future growth, either.

You can take a look at the company's revenue and earnings growth trend, in the chart below. For finer detail, click on the image.

Fortunately, we've got access to analyst forecasts of Choice Properties Real Estate Investment Trust's future profits. You can do your own forecasts without looking, or you can take a peek at what the professionals are predicting.

Are Choice Properties Real Estate Investment Trust Insiders Aligned With All Shareholders?

Investors are always searching for a vote of confidence in the companies they hold and insider buying is one of the key indicators for optimism on the market. Because often, the purchase of stock is a sign that the buyer views it as undervalued. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

Although we did see some insider selling (worth CA$85k) this was overshadowed by a mountain of buying, totalling CA$4.2m in just one year. We find this encouraging because it suggests they are optimistic about Choice Properties Real Estate Investment Trust'sfuture. It is also worth noting that it was President & CEO Rael Diamond who made the biggest single purchase, worth CA$1.5m, paying CA$14.38 per share.

Along with the insider buying, another encouraging sign for Choice Properties Real Estate Investment Trust is that insiders, as a group, have a considerable shareholding. Indeed, they hold CA$25m worth of its stock. This considerable investment should help drive long-term value in the business. Despite being just 0.2% of the company, the value of that investment is enough to show insiders have plenty riding on the venture.

While insiders already own a significant amount of shares, and they have been buying more, the good news for ordinary shareholders does not stop there. The cherry on top is that the CEO, Rael Diamond is paid comparatively modestly to CEOs at similar sized companies. The median total compensation for CEOs of companies similar in size to Choice Properties Real Estate Investment Trust, with market caps between CA$5.4b and CA$16b, is around CA$6.3m.

Choice Properties Real Estate Investment Trust offered total compensation worth CA$3.5m to its CEO in the year to December 2021. That is actually below the median for CEO's of similarly sized companies. While the level of CEO compensation shouldn't be the biggest factor in how the company is viewed, modest remuneration is a positive, because it suggests that the board keeps shareholder interests in mind. It can also be a sign of good governance, more generally.

Should You Add Choice Properties Real Estate Investment Trust To Your Watchlist?

Choice Properties Real Estate Investment Trust's earnings per share have been soaring, with growth rates sky high. Just as heartening; insiders both own and are buying more stock. This quick rundown suggests that the business may be of good quality, and also at an inflection point, so maybe Choice Properties Real Estate Investment Trust deserves timely attention. Even so, be aware that Choice Properties Real Estate Investment Trust is showing 3 warning signs in our investment analysis , and 1 of those is a bit concerning...

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Choice Properties Real Estate Investment Trust, you'll probably love this free list of growing companies that insiders are buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here