Agilent Technologies (NYSE:A) Seems To Use Debt Quite Sensibly

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Agilent Technologies, Inc. (NYSE:A) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Agilent Technologies

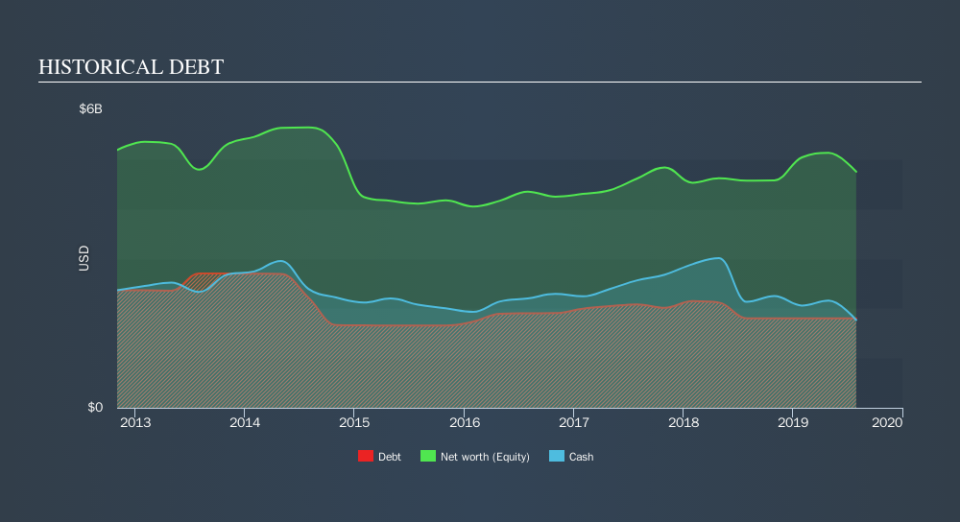

What Is Agilent Technologies's Debt?

As you can see below, Agilent Technologies had US$1.80b of debt, at July 2019, which is about the same the year before. You can click the chart for greater detail. However, it does have US$1.77b in cash offsetting this, leading to net debt of about US$33.0m.

How Healthy Is Agilent Technologies's Balance Sheet?

The latest balance sheet data shows that Agilent Technologies had liabilities of US$1.62b due within a year, and liabilities of US$2.26b falling due after that. Offsetting this, it had US$1.77b in cash and US$856.0m in receivables that were due within 12 months. So it has liabilities totalling US$1.26b more than its cash and near-term receivables, combined.

Since publicly traded Agilent Technologies shares are worth a very impressive total of US$23.1b, it seems unlikely that this level of liabilities would be a major threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. But either way, Agilent Technologies has virtually no net debt, so it's fair to say it does not have a heavy debt load!

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Agilent Technologies has very little debt (net of cash), and boasts a debt to EBITDA ratio of 0.027 and EBIT of 32.6 times the interest expense. So relative to past earnings, the debt load seems trivial. The good news is that Agilent Technologies has increased its EBIT by 5.0% over twelve months, which should ease any concerns about debt repayment. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Agilent Technologies can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, Agilent Technologies recorded free cash flow worth a fulsome 85% of its EBIT, which is stronger than we'd usually expect. That positions it well to pay down debt if desirable to do so.

Our View

The good news is that Agilent Technologies's demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And the good news does not stop there, as its conversion of EBIT to free cash flow also supports that impression! Looking at the bigger picture, we think Agilent Technologies's use of debt seems quite reasonable and we're not concerned about it. After all, sensible leverage can boost returns on equity. We'd be motivated to research the stock further if we found out that Agilent Technologies insiders have bought shares recently. If you would too, then you're in luck, since today we're sharing our list of reported insider transactions for free.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.