AP IMPACT: Flood insurance hikes still a peril

JERSEY SHORE, Pa. (AP) — This small, central Pennsylvania river town doesn't have beach homes or boardwalks, but it shares more than a name with the famous stretch of New Jersey coastline 250 miles to the east.

Both are among the thousands of places around the U.S. where people could face trouble in the years ahead because of the rising cost of government-mandated flood insurance.

Earlier this month, Congress sought to ease their fears of sky-high premiums by rolling back a 2012 reform ending the government's costly practice of offering subsidized insurance for older homes and businesses in flood zones. The president signed the bill Friday.

But while the law was widely hailed as a victory for people who had seen their bills triple, quadruple or even increase 15-fold overnight, pocketbook pain for many has merely been delayed.

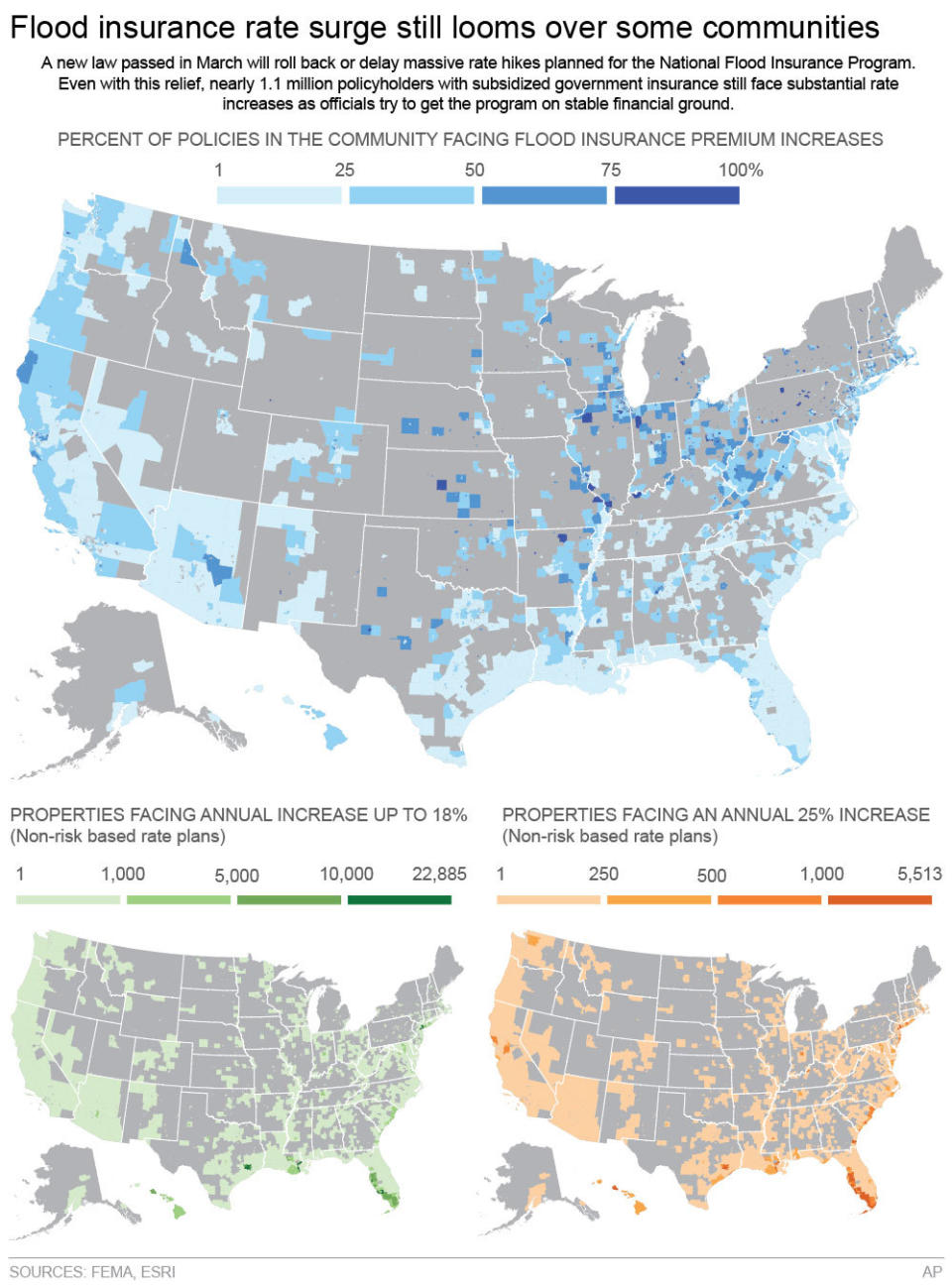

As many as 1.1 million policyholders with subsidized government insurance will still be hit with steady rate increases. While no one is sure yet how high rates will go, there is cause for worry in cities and towns that rely on affordable policies to keep businesses afloat and prop up the local housing market.

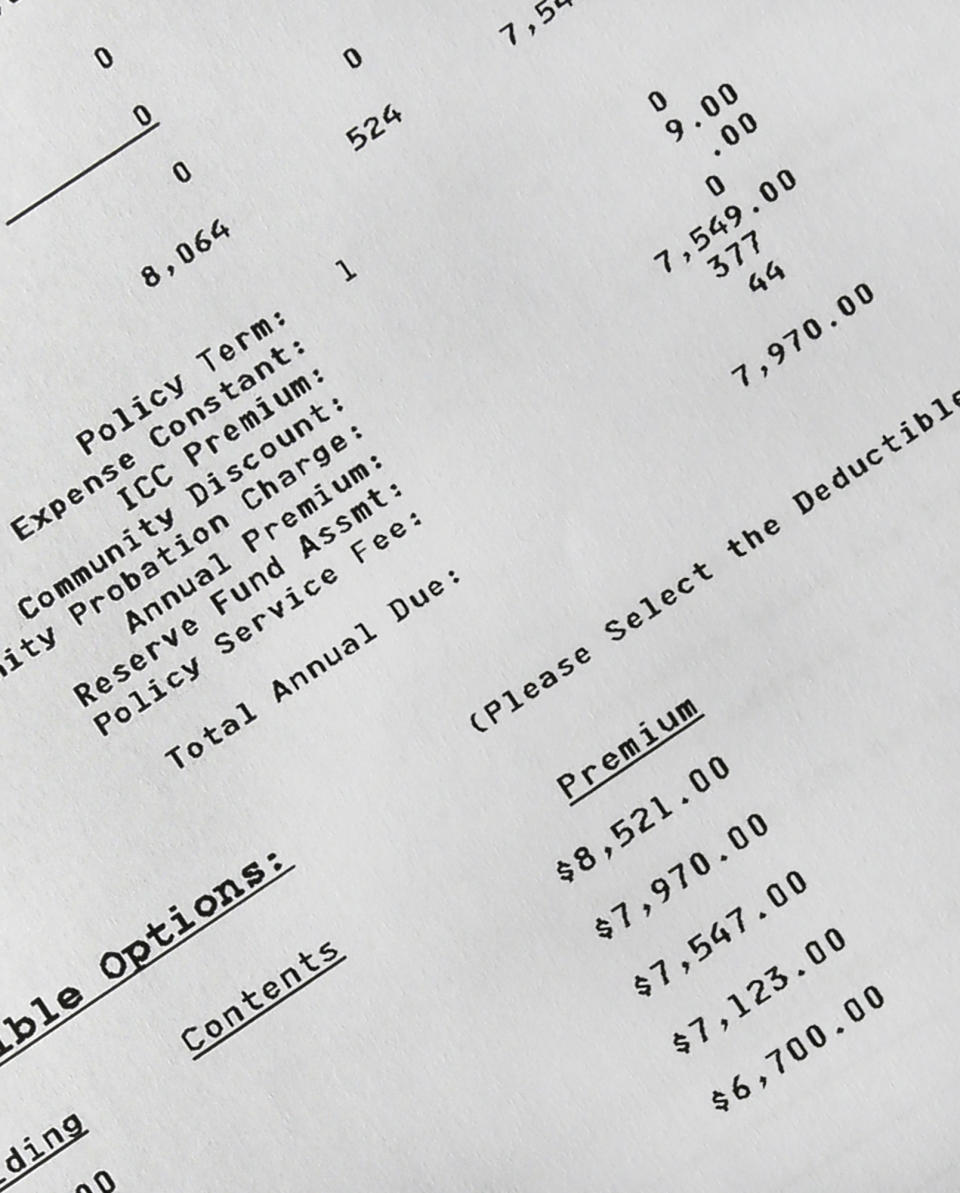

Lurie and Michael Portanova are lifelong residents of Jersey Shore, which sits in a flat flood plain along the banks of the West Branch of the Susquehanna River. They bought up a row of quaint, 19th-century brick shops on the town's main street and have been lovingly restoring them. They found out a few months ago that the annual flood insurance premium on two buildings they bought in 2012 had soared from less than $3,000 to a minimum of $26,868 for a high-deductible policy, or up to $33,000 if they kept their original coverage.

Now, thanks to the congressional rollback, that rate will reset to where it was before — only to immediately start climbing again, year after year. Within five years, the bill will be more than $8,700. Within a decade, it will be more than $26,000.

"There's no way we can afford that. Just no way," said Michael Portanova. "We'd have to let it go back to the bank and walk away from it."

The Portanovas and people like them are at mercy of forces — both political and natural — much greater than themselves.

For years, they've relied on insurance that was far cheaper than the risks warranted, and the federal government paid the difference. When Congress tried to stem the red ink by raising rates to reflect the real costs, people in the flood plains screamed — and the politicians listened.

But many say even the adjusted premiums will soon be beyond their means, though the question remains: Will the government continue to subsidize insurance in places that are increasingly untenable as sea levels rise and storms become more severe?

The Associated Press analyzed records from the Federal Emergency Management Agency for roughly 18,500 communities where the government offers subsidized rates.

The National Flood Insurance Program data show there are communities in every state where even a few years of price hikes could leave many affected owners unable to afford their properties. Hundreds of small river towns and coastal communities with significant numbers of homes and businesses in flood hazard zones are at risk.

FEMA's records also show why there is pressure to raise rates. Some communities with a large proportion of subsidized properties have been tremendously costly for the flood program. But there are just as many places where those policy discounts have cost taxpayers almost nothing — yet.

Late last year, a small but growing number of people felt the effects of the 2012 reform of the National Flood Insurance Program. Their rates rose dramatically.

Facing a widespread public outcry in an election year, Congress came to the rescue, rolling back parts of the 2012 law.

But at least 820,000 homeowners will still get hit with rate increases of up to 18 percent each year until the program is collecting enough revenue to cover a $24 billion shortfall created by the long-running discounts and a series of catastrophic storms.

Owners of another quarter million businesses or second homes will see their rates rise 25 percent each year, until their premiums reach rates that match what building elevation surveys indicate is the true risk of flooding.

For homeowners in Jersey Shore who know rates will be going up but don't know by how much or for how long, the future is as muddied as the waters of the Susquehanna.

Paul Garrett, who now pays $2,200 per year for flood insurance on a house that sits on the high riverbank, said he could take a year or two of 10 or 15 percent increases. But he says the threat that rates might go higher could render the house both unaffordable and potentially unmarketable.

"It's going to turn the towns that are on the river into ghost towns. Because nobody's going to want to pay that. Nobody's going to want to live here. Property values are going to plummet," he said.

There are indications that rising premiums already have had an effect. Records reviewed by the AP show that national enrollment in the insurance program dropped by nearly 80,000 in the 12-month period that ended Jan. 31, with the great majority of that decline coming after rates began going up on Oct. 1 under the 2012 law.

The FEMA datasets analyzed by the AP included all historical insurance payouts by the NFIP, a tally of the annual premium each community in the program is currently paying, and a breakdown of policies on homes and receiving a discounted rate.

That data show that 1,402 communities nationwide have at least 100 homes or businesses facing gradual price hikes. Of those, 765 communities have at least 200 policyholders who will steadily lose their discounts.

While the rate hikes will unquestionably affect the largest numbers of people in subtropical coastal cities like New Orleans, Miami and St. Petersburg, Fla., they also have the potential to deliver crippling blows to old river towns and port cities that have little in common with the eroding beach communities that have earned the flood program so much scorn.

The list includes places like Hoquiam, Wash., an old logging port on an estuarine bay where the great majority of the city's 8,700 residents live in a flood hazard area.

So far, Hoquiam has been a bargain for the flood insurance program. Its roughly 1,200 policyholders — nearly all of whom are subsidized — now pay a collective $1.3 million per year in premiums, yet the program has only paid out $436,723 in claims in the city since the mid-1970s.

But concern about rising premiums has been severe enough in Hoquiam that the mayor and local real estate agents say it is getting tough to sell homes because of concerns about where rates could go.

"While Congress was able to make the glide path a little more gentle ... they still did nothing, zero, to really address the affordability issues," said Chad Berginnis, executive director of the Association of State Floodplain Managers.

In Brunswick, Ga., a port city where nearly 1,200 policyholders are set to gradually lose their subsidized rates, the new legislation will offer temporary relief to people like Ray Bodrey, whose annual premiums had surged from under $700 to more than $4,700 before the rollback.

But if FEMA opts for an average increase of 15 percent each year, his annual payments would top $2,800 within a decade, and keep climbing — rates he says will push the limit of what he can afford.

"It doesn't help me at all. We've still got the same problem," Bodrey said. "I saw this politician saying something on CSPAN, out in Texas, and he said he was tired of Joe Blow subsidizing all these rich people on the coast. Well, not everybody who lives on the coast is a millionaire. I don't even make $40,000 per year. I'm working class like everybody else."

And yet, if rates don't climb, taxpayers will surely have to spend increasingly vast sums to bail out a struggling flood insurance program that makes it easy for people to keep on living in dangerous spots in an age of potentially stronger storms and rising seas.

"We've solved a very short-term problem and made it a long-term problem," said Sen. Tom Coburn, R-Okla. "We didn't really do our work because we were in such a hurry to take the political pressure off of the increases in the flood insurance rates."

Congress created the National Flood Insurance Program in the late 1960s, in part because private insurers had abandoned the market. Today, in most places, it is the only option for buying flood insurance, though a small number of private insurers have lately re-entered some markets on a limited basis.

Much of the program is aimed at ensuring that any new construction will stay dry in most floods. Almost everyone getting a mortgage on a property in a flood hazard zone is required to buy flood insurance. Rates for new properties not built above the required elevation expected to be inundated in a so-called "100-year flood" are exorbitant.

But the original program also made policies available at discounted rates for homes and businesses built in those hazard areas before 1975, when there were few rules and few accurate flood maps. These properties were the most at risk of catastrophic damage, but rates were kept low — subsidized by the U.S. Treasury — because owners otherwise would be priced out of their properties.

Today, these subsidized properties make up about 20 percent of the 5.5 million policies in the program, but they are an albatross, producing less in premiums than they are collectively paid in claims.

In Owego, N.Y., a village of 3,900 people near the Pennsylvania border where 378 policyholders get insurance at a discounted rate, repeated flooding from another branch of the Susquehanna in recent years has led to $28.1 million in flood insurance payouts.

The problem became a monster after Hurricane Katrina, when the program had to borrow $17 billion to cover payouts. After Superstorm Sandy, the program's debt topped $24 billion.

In Toms River, N.J. — on the other Jersey Shore — the insurance program has shelled out $519 million in payments so far, much of it as a result of catastrophic flooding during Sandy, compared to the $9.5 million all policyholders there paid last year.

Congress decided just months before Sandy struck that the subsidies had to go.

With broad bipartisan support, lawmakers abolished an old rule limiting rate increases to 10 percent per year, eliminated subsidies immediately for any property that changed ownership, and erased old grandfathering rules that protected properties from price increases if updated flood maps put them in a new flood zone.

Owners of properties that lost subsidies had to undergo an elevation survey, which was used to set rates based on actual risk.

The revised law does offer rate relief where many say it is needed most.

It restores those lost grandfathered protections, meaning new flood maps won't trigger massive, immediate rate increases.

A change of ownership also will no longer trigger an immediate jump to a risk-based rate. People hit by sky-high premiums after buying a new policy on a previously subsidized home will even be able to claim a refund.

The law does not, however, offer relief to the owners of vacation homes, businesses or buildings that have suffered repeat flooding. They will see mandatory annual increases of 25 percent until they switch to a rate based on an elevation survey.

Others will see rate hikes that are harder to predict. The law caps the increase of any individual policy at 18 percent. Increases for most property classes are capped at an average of 15 percent per year, meaning individual increases could be lower.

FEMA could increase overall rates less than that, but it has estimated that it needs to squeeze $1 billion to $2 billion more per year from policyholders still enjoying subsidies to put the program on solid actuarial ground.

Congress tried to deal with the issue of large numbers of policyholders being hit with premium hikes beyond their means by including language asking FEMA to "strive to minimize" the number of policies with an annual premium that exceeds $1 for every $100 in insurance coverage.

Yet, that suggestion would be impossible for FEMA to follow without giving huge new discounts to the policyholders now paying above that rate.

All of that adds up to a big question mark for homeowners.

How high will their rates ultimately go?

One FEMA-funded study, conducted in 1999, estimated that 550,000 homes across the country would see premiums top $6,800 per year if they were required to pay a premium based on the true flooding risk.

That leaves homeowners like Regina Bachman, of Loveland, Ohio, simply guessing how bad it might get.

After stretching her finances to buy a $95,000 home near a creek last September, she was belatedly hit with an annual flood insurance bill of $7,900. The previous owner had paid under $700.

Now, she's getting a reprieve. But with rate hikes coming, one drip at a time, she isn't sure how long it will last. She is hoping rates will stay low long enough for Congress to overhaul the program again, when it is up for legislative renewal in 2017.

"Because it can only go so high before we can't afford it. We're going to lose our home."