What's Really Going to Drive Carvana's Growth

There's a lot to like about Carvana (NYSE: CVNA) from both a consumer and investor standpoint. It offers car buyers a pressure- and dealership-free environment with no salespeople or haggling, and a quick and easy website purchasing platform. The company will even deliver your vehicle or let you pick it up at a unique car vending machine.

On the other side of the equation, investors surely love Carvana: The stock has soared over 600% since its initial public offering and recently notched its 22nd consecutive quarter of triple-digit revenue growth.

Let's discuss the most important part of Carvana's growth currently, the negative aspects that come with explosive growth, and what's going to drive the top and bottom lines as the company eventually slows its number of market entries.

First things first

The most important measure of Carvana's growth currently is the number of retail units sold. Every one sold opens up multiple revenue streams besides the original sale, including finance receivables if consumers use Carvana's financing services, sales of vehicle service contracts (VSCs) and gap-waiver coverage for insurance, and the sale of vehicles acquired from trade-ins.

Because retail-unit growth drives the business, the obvious way to grow revenue is by expanding into untapped markets. Carvana opened its initial market in Atlanta in 2013 before entering two additional markets in 2014 and six in 2015, but has recently accelerated its rate of expansion, entering 52 markets during the first half of 2019 to reach a total of 137.

One of Carvana's car vending machines. Image source: Carvana.

As Carvana continues to enter new markets, its results have soared. During the second quarter, its retail units sold jumped 95%, pushing revenue 108% higher to $986 million.

The downside of such rapid expansion is that it comes at a steep cost. While Carvana's top line is moving higher, its second-quarter net loss also increased 25%. Its cash pile has dwindled from $172.7 million at the end of 2017 to $78.9 million at the end of 2018, and $40 million at the end of the second quarter 2019.

Increasing costs and a dwindling cash pile led to Carvana diluting shareholders with secondary offerings. On April 30, 2018, it offered 6.6 million shares of Class A common stock at $27.50 per share, generating roughly $172.3 million; another 4.2 million shares offered at $65 on May 24, 2019, generated roughly $258.8 million. Carvana also took on $250 million in senior notes due in 2023.

So far, investors have accepted the widening net losses and share dilution as its market expansion has sent revenue soaring. But eventually the number of new markets will slow, and growth on the top and bottom lines will need to come from somewhere else -- and there's good news on that front.

Growth from multiple avenues

With so much focus on Carvana's new markets, investors often overlook incremental sales and market-share gains in existing locations.

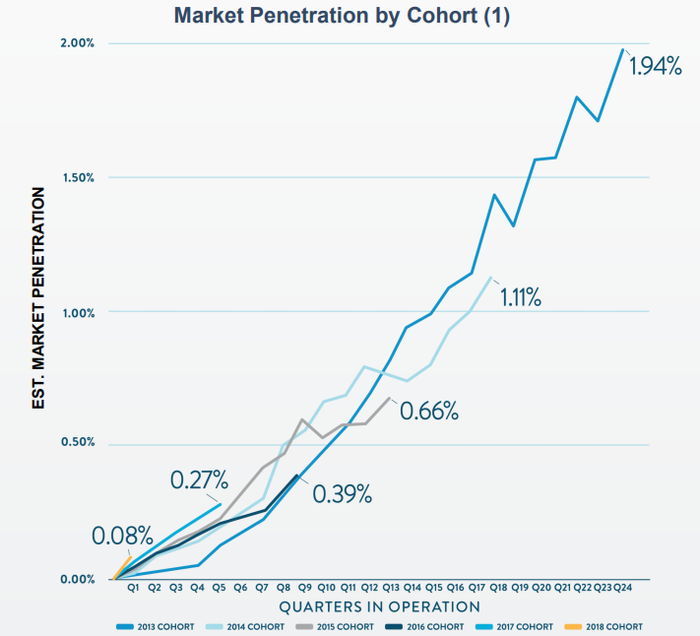

Graphic source: Carvana presentation, August 2019.

The above graph can look a little confusing, but there are two key takeaways from the data. The first is that Carvana has yet to reach peak penetration in its oldest market, which means all 137 markets at the end of the second quarter have substantial untapped market share gains. The second takeaway is that if you look at the two newest cohorts --the group of markets it entered in a particilar year -- you can see more-rapid growth in market share in the early months of entering a market.

Faster market penetration shouldn't come as a surprise, as the company's overall brand awareness grows and as it gets more effective and efficient with advertising, marketing, and operations. What's great about incremental growth in existing markets is that it's cheaper! As the up-front cost of entering markets fades, each will become more lucrative over time as the company gains penetration, does it more quickly, and lowers the costs of acquiring customers.

At the end of 2018, Carvana's penetration across its then 85 markets was 0.36%, leaving much business upside as the newer markets gain share to equal its original Atlanta market at 1.94%.

Another trend is gaining momentum for Carvana: the purchase and resale of consumers' vehicles. When Carvana announced it would ramp up purchases of consumer vehicles -- even if the consumers weren't buying a vehicle from Carvana -- most investors yawned. But reselling these vehicles is more profitable than reselling vehicles bought at auction. As previously mentioned, the strategy to buy consumers' vehicles is gaining speed: Total vehicles purchased this way were up 232% during the first quarter of 2019 versus the prior-year period. And consumer vehicles purchased as a percentage of retail units jumped from 24% during the first quarter of 2018 to 40% during the same period in 2019. When top-line growth inevitably slows from Carvana's impressive streak of triple-digit gains, selling a higher percentage of more-profitable vehicles bought from consumers will help grow the bottom line.

In addition to Carvana gaining incremental market share in older markets, and increasing its sales mix to more-profitable vehicles, improving operations can also enhance growth.

We saw a great example as second-quarter gross profit per unit (GPU) soared. Carvana impressed investors with its second-quarter GPU of $3,175, a staggering increase from the prior year's $2,173 -- and a step ahead of its midterm $3,000 goal, which many assumed wouldn't be reached for some time. The substantial improvement was due to a number of factors, including lowering its days to sale from 66 to 61, improved loan monetization, and higher attachment of VSC and gap-waiver coverage.

What it all means

Right now, investors are buying Carvana's growth story, and it's easy to understand why: its rapid market expansion and soaring top-line growth. Eventually, that top-line growth will slow, and it will have to boost the top and bottom lines in other ways to satisfy investors and reach profitability.

It can do this by buying more vehicles from consumers and reselling them; expanding its servicing, financing, and extended-warranty coverages; and gaining incremental market penetration.

The question is: Can Carvana execute those strategies fast enough to satisfy investors. It will be an interesting journey for the young used-car retailer and its shareholders.

More From The Motley Fool

Daniel Miller has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

This article was originally published on Fool.com