Is Astra Microwave Products (NSE:ASTRAMICRO) A Risky Investment?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Astra Microwave Products Limited (NSE:ASTRAMICRO) does carry debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Astra Microwave Products

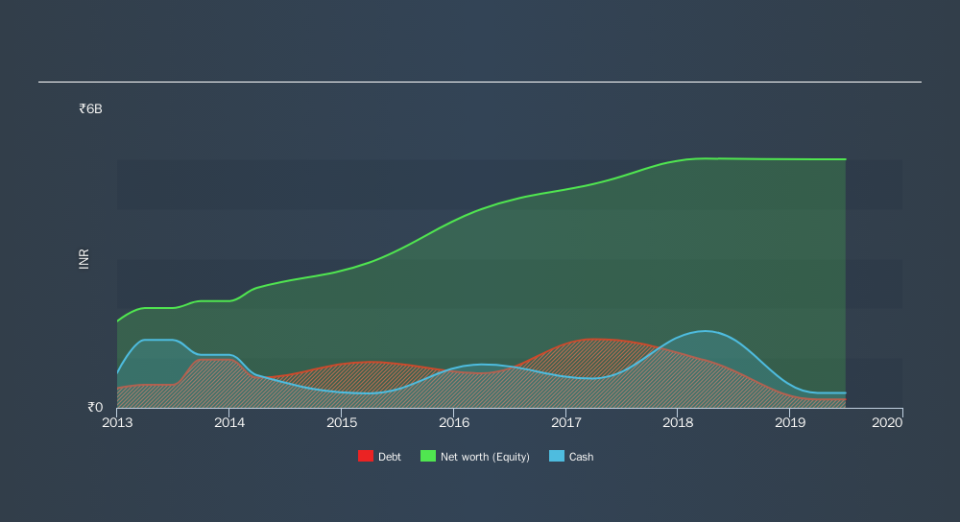

What Is Astra Microwave Products's Net Debt?

The chart below, which you can click on for greater detail, shows that Astra Microwave Products had ₹168.0m in debt in March 2019; about the same as the year before. But on the other hand it also has ₹300.5m in cash, leading to a ₹132.5m net cash position.

A Look At Astra Microwave Products's Liabilities

The latest balance sheet data shows that Astra Microwave Products had liabilities of ₹1.07b due within a year, and liabilities of ₹97.1m falling due after that. Offsetting these obligations, it had cash of ₹300.5m as well as receivables valued at ₹1.92b due within 12 months. So it can boast ₹1.06b more liquid assets than total liabilities.

This surplus suggests that Astra Microwave Products is using debt in a way that is appears to be both safe and conservative. Given it has easily adequate short term liquidity, we don't think it will have any issues with its lenders. Simply put, the fact that Astra Microwave Products has more cash than debt is arguably a good indication that it can manage its debt safely.

Importantly, Astra Microwave Products's EBIT fell a jaw-dropping 46% in the last twelve months. If that earnings trend continues then paying off its debt will be about as easy as herding cats on to a roller coaster. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Astra Microwave Products can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. Astra Microwave Products may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, Astra Microwave Products produced sturdy free cash flow equating to 61% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Summing up

While it is always sensible to investigate a company's debt, in this case Astra Microwave Products has ₹132.5m in net cash and a decent-looking balance sheet. So we are not troubled with Astra Microwave Products's debt use. Of course, we wouldn't say no to the extra confidence that we'd gain if we knew that Astra Microwave Products insiders have been buying shares: if you're on the same wavelength, you can find out if insiders are buying by clicking this link.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.