Are Atrys Health, S.A.'s (BME:ATRY) Interest Costs Too High?

While small-cap stocks, such as Atrys Health, S.A. (BME:ATRY) with its market cap of €79m, are popular for their explosive growth, investors should also be aware of their balance sheet to judge whether the company can survive a downturn. Assessing first and foremost the financial health is essential, as mismanagement of capital can lead to bankruptcies, which occur at a higher rate for small-caps. The following basic checks can help you get a picture of the company's balance sheet strength. However, potential investors would need to take a closer look, and I’d encourage you to dig deeper yourself into ATRY here.

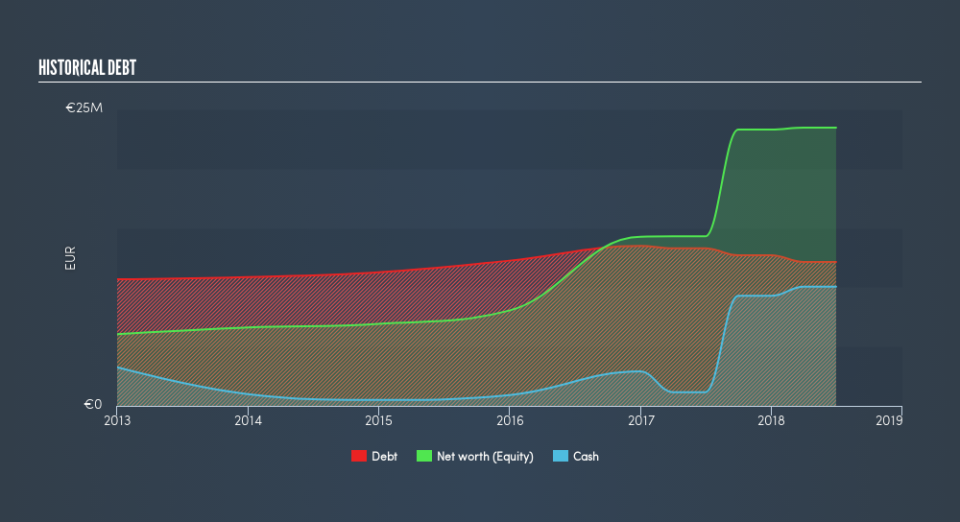

Does ATRY Produce Much Cash Relative To Its Debt?

Over the past year, ATRY has reduced its debt from €13m to €12m , which also accounts for long term debt. With this debt repayment, ATRY currently has €10m remaining in cash and short-term investments , ready to be used for running the business. Moreover, ATRY has produced €407k in operating cash flow during the same period of time, resulting in an operating cash to total debt ratio of 3.4%, meaning that ATRY’s debt is not covered by operating cash.

Can ATRY pay its short-term liabilities?

Looking at ATRY’s €3.9m in current liabilities, it appears that the company has maintained a safe level of current assets to meet its obligations, with the current ratio last standing at 3.73x. The current ratio is calculated by dividing current assets by current liabilities. Having said that, a ratio greater than 3x may be considered by some to be quite high, however this is not necessarily a negative for the company.

Does ATRY face the risk of succumbing to its debt-load?

ATRY is a relatively highly levered company with a debt-to-equity of 52%. This is a bit unusual for a small-cap stock, since they generally have a harder time borrowing than large more established companies. We can check to see whether ATRY is able to meet its debt obligations by looking at the net interest coverage ratio. A company generating earnings before interest and tax (EBIT) at least three times its net interest payments is considered financially sound. In ATRY's, case, the ratio of 0.4x suggests that interest is not strongly covered, which means that debtors may be less inclined to loan the company more money, reducing its headroom for growth through debt.

Next Steps:

Although ATRY’s debt level is towards the higher end of the spectrum, its cash flow coverage seems adequate to meet obligations which means its debt is being efficiently utilised. This may mean this is an optimal capital structure for the business, given that it is also meeting its short-term commitment. This is only a rough assessment of financial health, and I'm sure ATRY has company-specific issues impacting its capital structure decisions. I suggest you continue to research Atrys Health to get a more holistic view of the small-cap by looking at:

Historical Performance: What has ATRY's returns been like over the past? Go into more detail in the past track record analysis and take a look at the free visual representations of our analysis for more clarity.

Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.