AutoZone vs Advance Auto: Which Retail Stock Is A Better Pick?

The auto industry is gradually recovering from the sales slump experienced during the pandemic-led lockdown period earlier this year. According to General Motors, total industry vehicle sales came in at 15.9 million units (at a seasonally adjusted annualized rate) in the third quarter, reflecting an increase of about 4 million units from the second quarter. Consumers are preferring owned-vehicles to public transportation due to the COVID-19 outbreak. Also, the demand for used cars has been strong over recent months. Challenging macro conditions are impacting consumers’ spending capacity, thus boosting the demand for used vehicles compared to new vehicles.

Auto parts retailers have also gained momentum over recent months as people are spending their extra time at home toward DIY (do-it-yourself) vehicle repairs and maintenance activity. Against this backdrop, we will use the TipRanks Stock Comparison tool to place AutoZone and Advance Auto Parts alongside each other and see which auto parts retailer offers a more compelling investment opportunity.

AutoZone (AZO)

AutoZone, the largest US retailer of automotive replacement parts and accessories, operates 5,885 stores in the country, 621 stores in Mexico and 43 stores in Brazil. After facing challenges in 3Q FY20 due to the temporary closure of stores amid pandemic-led lockdowns, the company’s domestic same-store sales grew 21.8% in 4Q FY20 (ended Aug 29). According to CEO Bill Rhodes, 4Q same-store sales growth marked the company’s largest quarterly growth since going public in 1991.

Overall, 4Q FY20 sales increased 14% to $4.5 billion year-over-year with same-store sales of the company’s DIY business rising 24%. The DIY category benefited as people had more time at their hands to pursue car enhancement and maintenance projects. The company also attributed the demand to COVID-19 unemployment benefits.

In addition, AutoZone experienced strong growth in its online channels. However, online sales still account for less than 5% of the DIY business. Meanwhile, total DIFM (do-it-for-me) sales increased 16.8% to $976 million year-over-year. Strong top-line growth helped the company deliver EPS of $30.93 in 4Q FY20, reflecting a 47.6% growth on an adjusted basis.

AutoZone did not provide guidance for FY21 due to COVID-related uncertainties. At the same time, the company said that it expects sales growth to moderate over time. However, it continues to foresee high demand for its products and services given the challenging economic conditions in which consumers tend to improve their existing vehicles rather than buy a new one.

The company expects to open about 150 new stores in the US and 50 international stores in FY21. That's up from the opened 113 US stores and 25 stores across Mexico and Brazil in FY20. It also plans to gradually resume its share buyback program in 1Q FY21 after the temporary suspension in March. (See AZO stock analysis on TipRanks)

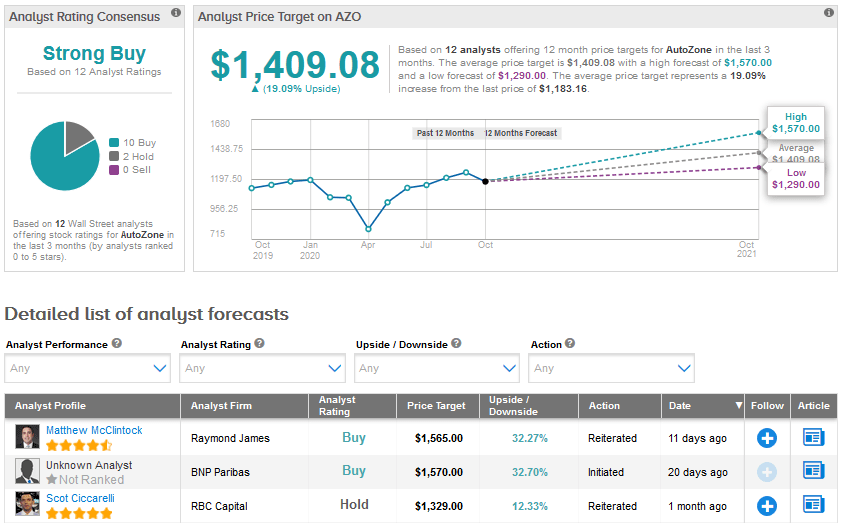

On Oct. 13, Raymond James analyst Matthew McClintock raised the stock's price target to $1,565 from $1,500 and reiterated his Buy rating. The analyst called AutoZone his top pick and noted “Management gave rare forward commentary for the first time in at least five years, and we certainly believe it was positive for both the forward quarter (1Q21) and forward year (FY21).”

Commenting on the commercial business, the analyst added “After more than five years of long-term investments in the DIFM business (as well as persistent skepticism from the investment community), AZO began to deliver outstanding growth and returns for this segment over a year ago, which was only further demonstrated by recent results. We firmly believe that market consolidation opportunities in a post COVID world should only increase our pre COVID expectations for growth in this segment.”

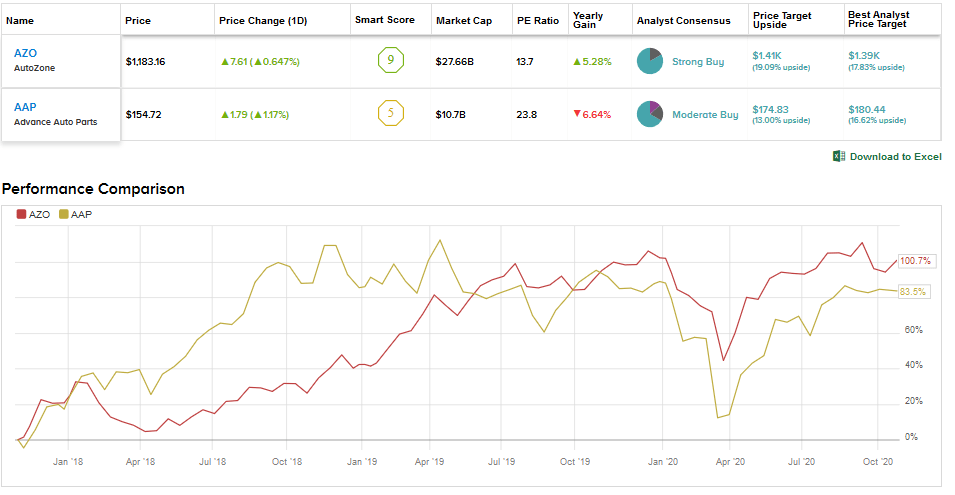

The Street is in line with McClintock’s bullish stance. A Strong Buy consensus on AutoZone stock is based on 10 Buys versus 2 Holds and no Sells. With shares down 0.74% year-to-date, the average analyst price target of $1,409.08 implies upside potential of 19.1% in the 12 months ahead.

Advance Auto Parts (AAP)

Auto aftermarket parts retailer Advance Auto Parts sells its products to professional installers and DIY customers through its 4,819 stores and 167 Worldpac branches in the US, Canada, Puerto Rico and the US Virgin Islands. The company also serves a network of 1,262 independently owned Carquest brand stores.

Following an 8.6% decline in 1Q FY20 sales, Advance Auto bounced back in 2Q FY20 (ended Jul. 11) with sales rising 7.3% to $2.5 billion year-over-year. Comparable store sales growth of 7.5% in 2Q marked the highest quarterly growth rate for the company in nearly 10 years. The company attributed strong sales momentum to a spike in industry demand driven by government stimulus, unemployment benefits and a rise in DIY projects.

Notably, the company’s DIY omnichannel business drove comparable sales growth in the second quarter and performed better than the DIFM business. The DIY omnichannel business benefited from the company’s nationwide launch of the same-day delivery facility and initiatives to strengthen the front-end user experience on the online platform, which helped in boosting site traffic and conversion rates.

However, the DIFM business was hit by the temporary closure of garages across North America due to the pandemic. Plus, Advance Auto’s Professional business derives a significant proportion of its sales from the Northeast, Mid-Atlantic and the West Coast regions, which were severely impacted by COVID-19.

Robust sales growth coupled with margin expansion due to favorable channel mix, supply chain efficiencies and cost savings helped in driving 46% growth in 2Q adjusted EPS to $2.92. In addition, Advance auto has been enhancing its supply chain through improved execution and standardization in its distribution centers.

It has resumed its single warehouse management system or WMS initiative after halting it in 2Q. Under this initiative, Advance Auto is consolidating its warehouse management system across all its distribution centers. The company aims to complete WMS implementation in its large distribution centers by the end of 2021.

Backed by the results, Advance Auto lifted the temporary suspension of its share repurchase program. Looking ahead, the company did not provide a forecast for 3Q but said that DIY momentum in the second quarter continued into the third quarter. (See AAP stock analysis on TipRanks)

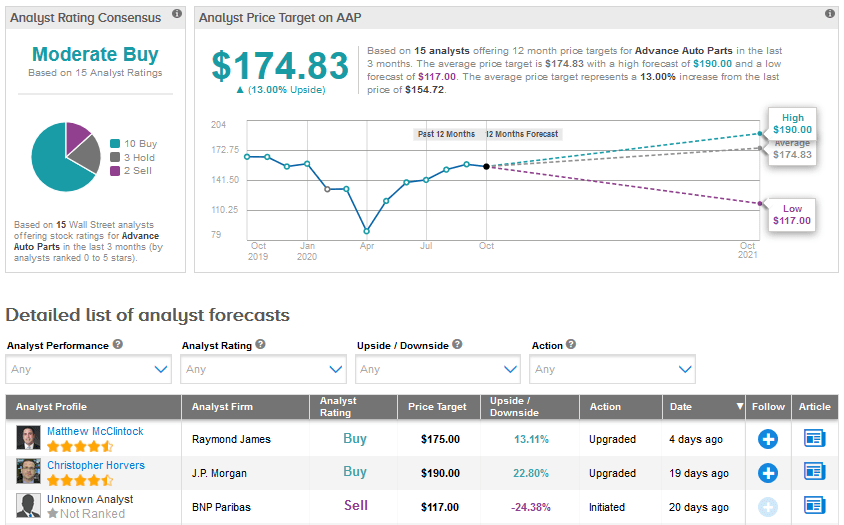

Earlier this month, JPMorgan analyst Christopher Horvers upgraded AAP to Buy from Hold and raised the price target to $190 from $183.

The analyst cited five reasons for the upgrade “(1) strong/sustainable current trends bridging to an easy winter weather comparison with this year looking relatively better vs. an acutely warm winter last year that hurt AAP more than peers (one of the reasons why we downgraded in January); (2) 'own the Pro in 2021' given AAP’s ~50% DIFM mix combined with the exaggerated impact COVID-19 had on DIFM trends in its core Northeast market; (3) increasing top-line benefits from the peak repair cohort (6-12 years old) in 2021 and 2022; (4) AAP’s margin story blossoms in 2021 and more so in 2022 as the company progresses on its transformation; and (5) stock underperformance relative to the market."

Overall, the Street is cautiously optimistic on the stock with 10 Buys, 3 Holds and 2 Sells adding up to a Moderate Buy analyst consensus. The average analyst price target of $174.83 implies upside potential of 13% over the coming 12 months. That's after shares declined 3.4% so far this year.

Conclusion

The Street has a more bullish outlook on AutoZone stock compared to Advance Auto Parts. Moreover, a lower valuation multiple and higher upside potential make AutoZone stock a better retail pick than Advance Auto currently.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment