How to Avoid Investing in a Zombie Company

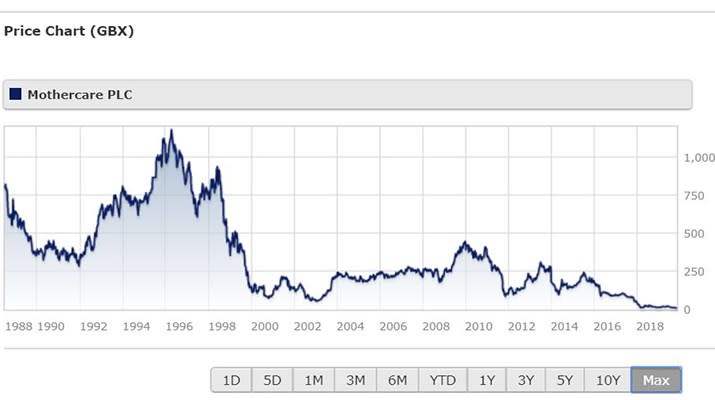

Halloween may be over but there are still plenty of horrors for UK investors to contend with. The high street is littered with the corpses of failed companies, with Mothercare the latest to fall into administration after a multi-year battle to get its finances on track.

But retail isn’t the only sector to contain distressed firms or “zombies” - these are companies that just about cling on to life because of rock-bottom interest rates, cheap borrowing and patient lenders.

And it’s not a UK specific phenomenon either; “zombies” are cluttering up the US, China and Europe, according to the Bank of International Settlements.

There are already signs that UK banks are becoming less keen to keep these companies on life support than in the recent past, and the prospect of recession in the next few years could lead to a further clearout of underperforming companies.

So, how do investors, both retail stockpickers and active fund managers, avoid the curse of companies like Carillion, Thomas Cook and Mothercare?

When a company goes under, the destruction of shareholder value runs into millions of pounds, wiping out individual investors, who rank far behind bondholders when a company is wound up.

But often the financial problems at these companies are signposted well in advance: Thomas Cook’s share price was decimated in 2018 but still fund managers were buying into the stock this year with the hope of a turnaround. Mothercare tapped investors for cash in a 2014 rights issue to help pay off its loans, closed stores in 2018 to shore up its finances, but its UK arm fell into administration in October 2019.

Are All Troubled Firms Zombies?

The Bank of International Settlements, (BIS) the body that supervises global central banks, has written extensively about how “zombie” firms are clogging up the global economy and holding back growth. Its technical definition of a zombie is a company that cannot service its debt from current profits. With interest rates low for a decade after the financial crisis, these firms have proliferated – and the “lower for longer” mantra from central banks looks set to extend their stay of execution.

But BIS’s analysis has some surprising findings: the US market, some 12% of firms in the S&P 1,500 (a much wider index than the S&P 500) can be classed as zombies. The problem is also acute in China, where authorities have started to take action to withdraw life support from ailing companies.

In an era of ultra-low interest rates, why can’t all lenders just extend loans or roll them over indefinitely? As the economy starts to flag ahead of Brexit, banks’ risk appetites are starting to harden, says Mark Swain, manager of the Smith & Williamson Enterprise Fund.

“Ultimately it always comes down to finance,” he says. He argues that high-profile UK blow-ups in recent years can be broken down simply into: too much debt that can’t be refinanced (Thomas Cook) or a business that hasn’t adapted quickly enough to the e-commerce era (Mothercare).

During the financial crisis, many UK banks started to behave like zombies but now they are very conservatively run with large capital buffers and rigorous compliance standards.

However, some European banks are still in dire straits, as the woes of Deutsche Bank show. Swain argues that UK banks are keen to avoid losing their shirts when a company goes under and would rather pull the plug on struggling firms earlier.

Breaching "banking covenants", which are legal agreements between lenders and creditors, is often a sign that a company is about to go under. In a tighter regulatory environment, banks are becoming much tougher with companies that fail to keep up with their repayments.

“You’ve really got to do your credit homework to understand whether there’s a possibility of recovery when the company starts to stumble,” says Eoin Murray, head of investment at Hermes.

Struggling Retailers

Low borrowing costs are helping to prolong the suffering of some UK retailers, argues Nicla di Palma, a retail analyst at Brewin Dolphin. But ailing companies in the sector are already feeling the effect of market forces, as the long list of recent failures demonstrates.

However she thinks that much of the risk is already reflected in the share prices of the companies that do continue to exist. “The share price already reflects the risk that either they won’t exist or the number of stories will be greatly reduced,” di Palma says.

The company voluntary arrangement (CVA) scheme has also been blamed for prolonging the slow death of many retailers. The CVA came into its own during the last UK recession, allowing companies some breathing space to deal with creditors and get back on their feet rather than go bust. But retail landlords like Intu have argued recently that CVAs sometimes gives companies too much time to get their house in order. In Mothercare's case, the CVA just delayed the slide into administration a year later.

A UK investor could be forgiven for thinking that many home-grown retailers are just one step away from blowing up, but it’s clear the problem is a worldwide one. Indeed, Swain argues that that the UK stock market is “regarded as a pretty well functioning blue-chip market”, where the worst companies go under and the best companies prospert.

So where can the next zombies be spotted? Further afield, he argues that many US oil companies are very vulnerable to further oil price weakness and he also has an eye on global airlines and big construction companies, whose projects were launched in more benign economic conditions. “There a lot of guesswork in the numbers and it doesn’t take much for the contracts to become unprofitable,” says Swain.

What Will Kill Off the Zombies?

Global investors have already pushed back their assumptions about when interest rates will “normalise” so in theory that buys troubled firms some more time.

But while rising borrowing costs may not land the fatal blow for zombies, but a global recession could finish them off, argues Murray, who forecasts further business failures in the next two years.

BIS says that more failures of underperforming firms could actually help improve productivity and release capital for more worthy causes, such as infrastructure and the sustainable economy. "Zombies are less productive and may crowd out growth of more productive firms by locking resources," BIS argues. "Specifically, they depress the prices of those firms' products, and raise their wages and their funding costs, by competing for resources."

But Murray points out that, while fewer zombies should be welcomed by economists and investors alike, there is still a human cost in terms of lost jobs. He also notes that a clearout of bad firms could create a serious problem for passive investing, which has grown in popularity in recent years.

"If you slavishly follow the index, and 14% of the index is likely to go to the wall as soon as we get some sort of economic downturn, that’s bad news,” says Murray. This puts a premium on active stock picking, he argues, but not everyone can get it right and avoid buying into the next generation of zombies.