The Best Fintech Stocks to Buy in 2019 and Beyond

Fintech, short for financial technology, describes how the financial industry has leveraged technology to make financial services cheaper, faster, more efficient, and more accessible.

Modern fintech applications range from the simple to the complex, including:

Online and mobile banking platforms

Person-to-person (P2P) payment apps

Robo-advisers, or digital financial advice based on algorithms and artificial intelligence (AI), given with little to no human intervention

Blockchain technology and cryptocurrencies

Crowdsourcing platforms

Mobile brokerage apps that feature commission-free trading

Accounting software that automates previously laborious and tedious tasks

And more!

Fintech covers a wide range of applications, from digital wallets and cryptocurrencies to fraud protection and new loan processes. Image source: Getty Images.

Why fintech matters

Fintech is important because it democratizes financial services, making it cheaper and more convenient than ever for the average person to perform basic financial tasks.

There is also growing evidence that fintech is at least partly responsible for the shrinking number of people who are unbanked or underbanked, defined as adults without access to basic financial services such as bank accounts and alternative means of payments beyond cash. In 2017, the World Bank reported there were still 1.7 billion unbanked adults across the globe, a large number to be sure, but far less than the 2.7 billion unbanked population in 2011.

There are many benefits to financial inclusion. The World Bank cited studies from around the world in its 2017 Global Findex Database that showed that people who had access to bank accounts could save more, invest in their own businesses or farms, and spend more on things such as education and more nutritious food.

The World Bank report states, "A growing body of research reveals many potential development benefits from financial inclusion -- especially from the use of digital financial services, including mobile money services, payment cards, and other financial technology (or fintech) applications." Companies such as PayPal Holdings (NASDAQ: PYPL), Mastercard (NYSE: MA), and Square have proactively worked on solutions to help meet this need.

How popular is fintech?

There can be little doubt that the demand for fintech products and services is rising among consumers. In its April 2019 Where Will We Bank Next? study, PYMNTS.com found that "trust" was still the most-cited answer (63%) from consumers asked why their financial institution fit their needs. It was followed closely, though, by other answers such as easy-to-use online banking services (the second-most-cited answer, at 57.6%) and easy-to-use mobile apps (sixth-most, at 44.4%).

In the same survey, 42.5% of respondents stated they would not be interested in looking to another consumer brand for their banking needs. However, among the majority of consumers (57.5%) who stated they would consider nonfinancial institutions to fulfill their banking needs, the top choices were mostly from the ranks of big tech and existing fintech companies. In fact, of the five most popular brands listed:

30.5% said they would consider PayPal

24.8% Amazon.com

17.5% Walmart

14.9% Alphabet

13% Apple

An increasing number of consumers are interested in mobile apps on their smartphone to accomplish basic financial tasks. According to the 2017 Total System Services U.S. Consumer Payment Study, the following percentage of respondents are either interested in or already using their smartphones to:

Stop fraudulent transactions (80%)

Instantly view credit and debit card transactions (72%)

Turn a card on or off based on merchant, time, and location (64%)

Receive instant offers from a store they are visiting (59%)

Keep loyalty and reward points on a phone (56%)

All these categories also show double-digit percentage-point increases from the same study's 2015 results, demonstrating that consumer demand for fintech solutions is only growing. In addition, more than 50% of the survey's respondents said they were using, or interested in using, their phone for P2P payments, making purchases, and changing the PIN on their debit and credit cards.

What's happening in the fintech sector now?

The fintech sector has undergone a great deal of growth and disruption, and it's being funded more from venture capital (VC) investment rounds than initial public offerings (IPOs). In 2018, according to CB Insights, VC-backed fintech companies raised a record $39.75 billion over 1,707 deals, more than twice the amount that was raised through similar deals in 2017. Because venture capital has played such a large role in early-seeding investing for these fintech companies, investors can likely expect that companies will be much larger, on average, when they eventually go public, leaving less upside for individual investors. This influx of private capital has created a number of unicorns in this space -- private companies valued at $1 billion or more.

Among public fintech companies, there has been a great deal of consolidation and dealmaking. So far in 2019, two of the three largest fintech deals ever have occurred, and they were notable for how similar they were to each other.

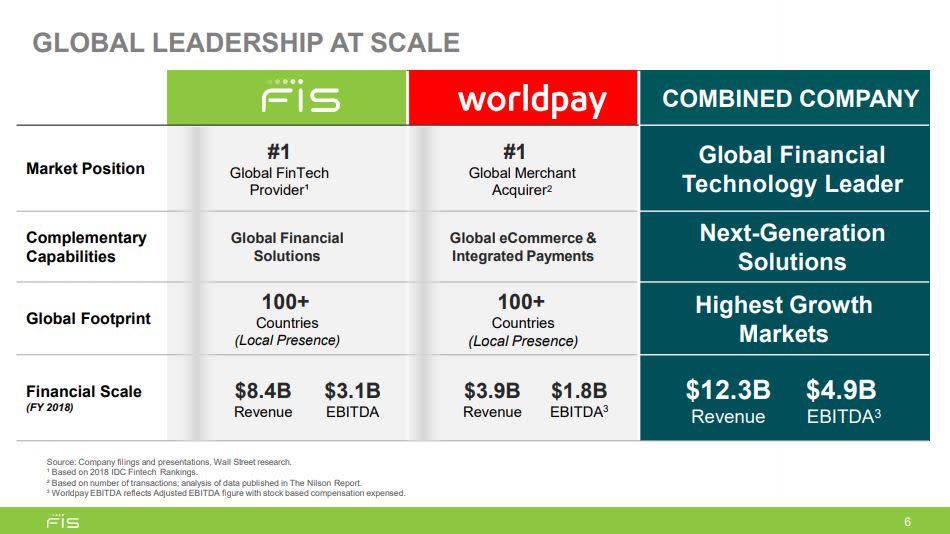

In January 2019, Fiserv acquired First Data for approximately $21.8 billion. Less than two months later, Fidelity National Information Services, commonly referred to as FIS, acquired Worldpay for $35.3 billion. In both cases, the deals featured some of the largest issuing processors, Fiserv and FIS, targeting some of the largest merchant processors, First Data and Worldpay. (Issuing processors settle and authorize credit and debit card payments for financial institutions, while merchant processors, also called acquirer processors, facilitate card and digital payments for merchants).

The FIS acquisition of Worldpay in early 2019 was the largest deal in fintech history. Image source: Fidelity National Information Services, Inc.

Separately, these two deals would be notable, but they are far from alone. Ultimate Software Group, a company that provides a cloud-based, software-as-a-service (SaaS) human capital management platform, was gobbled up by a private investment group for just under $11 billion.

This is on top of a number of acquisitions made by larger payments and financial services companies in recent years. In 2018, PayPal made four acquisitions for a combined total close to $3 billion. Mastercard is developing a reputable track record of making smart acquisitions to augment its services-based revenue, most notable among them its $920 million deal to buy VocaLink, a company specializing in enabling instant bank account transfers. Visa (NYSE: V), after finishing its integration with Visa Europe, has also begun making acquisitions again, most notably outbidding Mastercard for Earthport, a cross-border payments specialist.

The sector's vast consolidation, merger activity, and VC funding speaks to its opportunity and risk. Smaller disruptors are shaking up the industry from below, racing to find customers with their innovative solutions before larger financial institutions and legacy financial services innovate enough to keep their account holders within the fold.

What to look for in fintech investments

As with any growing industry, when investing in fintech companies, investors will want to look at important metrics such as revenue growth rates, gross and operating margins, and the company's total addressable market. However, when I invest in fintech companies, the most important question I want answered is whether the company is just selling a nifty product or service, or an entire ecosystem of products and services.

In my experience, companies that sell a product can be mimicked and have little competitive advantage. A company that sells ecosystems, however, soon has its customers so wrapped up in its offerings that leaving would be almost unthinkable, even if similar products and services could be found elsewhere. When a company continues to foster a culture of innovation, it can develop product lines strategically,

One of the best examples of this is Square. When Square was founded, it introduced a product that allowed small merchants to accept credit and debit card payments with a simple dongle that plugged into smartphones and tablets. The product was revolutionary, opening a world of opportunity to small businesses. Yet this was soon copied and mimicked by most other payment processing companies. If Square maintained just this one product, without growing out its ecosystem, it would have never grown into the $30-billion-plus payments behemoth it is today. Instead, it grew its product line to include all sorts of services, including everything from in-app payments and food delivery to payroll services and business loans.

Risks to investing in fintech

There are three primary risks to investing in fintech:

Credit exposure. This risk is especially applicable for companies whose entire business model is based on making loans; it will not be at all applicable to companies with no exposure. A good rule of thumb to remember is that companies with credit exposure will almost always get a lower valuation multiple from the market than companies with no such liability.

Consolidation. Fintech is shaking up the financial industry quickly, and it is often hard to know what the eventual winners will be. In some cases, it will undoubtedly be the nimble upstarts; in other cases, deeper-pocketed legacy players that react quickly enough to keep account holders within the fold.

Regulation. Consider Robinhood, the mobile-based brokerage app that offers commission-free trading. Robinhood's plans to offer checking and savings accounts with 3% interest rates to account holders were interrupted by federal regulators, who stated that the money would not be insured by either the Federal Deposit Insurance Corporation (FDIC) or the Securities Investor Protection Corporation (SIPC).

Who should invest in fintech?

Whether you are an income, value, or growth investor, there are fintech companies offering solid investment returns within your wheelhouse. For income investors, there are big banks investing heavily in technology while still offering decent yields. For value investors, there are unloved credit card companies and banks that trade at P/E ratios far below the S&P 500's average. Of course, dividend-paying banks with low P/E ratios will naturally have limited growth due to fintech initiatives alone, and come with all the risks listed above: They are exposed to debt, heavily regulated, and risk losing market share to more nimble industry upstarts.

That's why fintech will probably prove to be the greenest pasture for growth investors, since the sector includes companies growing revenue and earnings at double-digit rates, with large addressable markets still untapped. We'll explore several companies fitting that description later in this article.

Fintech ETFs, the easy way to invest in fintech

With fintech behind so many large trends, it's easy to see why investors would want to look for ways to profit from this theme. One of the easiest ways to do so is by investing in an ETF -- a basket of securities collected under one entity that can be traded on major exchanges -- designed to track the fintech industry. Besides being simple, ETFs offer instant diversification within the sector, limiting the risk of only being invested in a few different stocks. Two such ETFs match this criteria, including the Global X FinTech Thematic ETF and the Ark FinTech Innovation ETF. These ETFs offer investors instant diversification within the fintech sector and preclude them from having to pick individual winners.

The Global X FinTech Thematic ETF says it "seeks to invest in companies on the leading edge of the emerging financial technology sector, which encompasses a range of innovations helping to transform established industries like insurance, investing, fundraising, and third-party lending through unique mobile and digital solutions." Since its inception in late 2016, it has beaten the S&P 500 index by a significant margin. This is not surprising given that its top holdings include PayPal, Intuit, and Square.

The Ark FinTech Innovation ETF invests in companies that it says are "engaged in the theme of Fintech innovation," which is determined by whether a company has derived "a significant portion of its revenue or market value from the theme of Fintech innovation, or ... has stated its primary business to be in products and services focused on the theme of Fintech innovation." Be aware that this definition sometimes seems to be loosely interpreted when it translates to Ark's holdings, as some of its top-allocated positions include Apple, NVIDIA, and Zillow Group.

Top fintech stocks for 2019 and beyond

Top Fintech Stocks | Bullish elevator pitch |

|---|---|

Alibaba Group Holding (NYSE: BABA) | Alipay is one of world's largest mobile payments platform, and Ant Financial is the largest investor in fintech unicorns around the globe. |

BlackLine (NASDAQ: BL) | An SaaS company that automates tedious and laborious accounting practices for its enterprise clients. |

Global Payments (NYSE: GPN) | Payment processing company that is embedding its payment services into vertical software stacks serving niche industries. |

JPMorgan Chase (NYSE: JPM) | One of the best-run big banks that possesses the means to (and is not afraid to) invest heavily in new technology. |

MarketAxess Holdings (NASDAQ: MKTX) | This company operates the world's largest electronic fixed-income investment trading platform. |

Mastercard | The world's second-largest payments network has made a number of acquisitions to build out its supplemental services in areas such as AI-powered fraud prevention and data analytics. |

MercadoLibre (NASDAQ: MELI) | This Latin American powerhouse is much more than an e-commerce platform, with a fast-growing digital payments platform that can be used off-site and even a new asset management platform in Argentina. |

PayPal Holdings | Digital wallet platform with more than 267 million user accounts, including 21 million merchants. |

Q2 Holdings (NYSE: QTWO) | Its software products allow small banks to compete with the big banks by providing the digital tools necessary to build out the digital and mobile platforms that today's consumers demand. |

Visa | The world's largest payments network is showing a renewed interest in making sure it stays ahead of the times, after making a key acquisition. |

Let's take a closer look at some of these stocks to see what makes them particularly attractive for investors over the next several years.

Alibaba Group Holding

It is getting harder and harder to leave Alibaba Group Holding off any "best of" fintech list, thanks to its large stake in Ant Financial, the company behind Alipay, the mobile payments provider with more than one billion active global users. Its mobile payments platform includes 390 million users who can make secure payments based on their own biometric identification.

Ant Financial invested $14 billion in fintech unicorns in 2018. Image source: Alibaba Group Holdings Ltd.

Ant Financial is much more than a mobile payments platform; it also offers a set of solutions for asset management, insurance, and lending. For instance, its insurance solutions promise to use AI so that individuals receive the best policy based on their own personalized risk assessment. Its asset management platform offers optimized investment advice within seconds.

The best part about owning Alibaba is that it gives shareholders access to the world's largest investor in private fintech unicorns. In 2018, almost $40 billion was invested in private fintech start-ups through more than 1,700 deals. Incredibly, $14 billion of this funding, or about 35% of the total, came from one source -- Ant Financial. Most of these investments were spread across Southeast Asia in mobile payments and other fintech platforms that are exploding in popularity in their home countries, where cash is still heavily used and credit cards have never gained meaningful traction.

BlackLine

BlackLine offers a cloud-based, accounting software-as-a-service platform to its enterprise customers. BlackLine's platform enables companies to practice continuous accounting, rather than batch processing. Batch process accounting involves doing a large amount of work to close and reconcile books near the end of a pre-determined period, such as a month or quarter. Continuous accounting allows companies to reconcile in real time, as data from transactions and sales become available.

BlackLine founder and CEO Therese Tucker compares continuous to batch processing accounting:

There are some people of an age that remember ... you got paper bank statements in the mail and you would take those paper bank statements and you would compare them to your actual checkbook. That's gone away by now. But most companies still operate as though they have to wait for the paper in the mail to arrive before they can close their books each month, OK?

Tucker says investors would be "astonished by the level of manual work that goes into closing the books." By switching to continuous accounting, companies can make decisions using up-to-date data and free up key personnel for analysis and more important tasks.

BlackLine is not just a one-trick pony, however, as it has been working hard to expand its line of products to include other valuable accounting tools. In a February 2019 conference call, Tucker said, "We put a lot of effort into product innovation and bringing the market new products that drive real accounting and finance transformation and help expand our strategic value." These products include tools that automate and simplify traditionally difficult and labor-intensive accounting tasks, such as financial closes, bank statement reconciliations, and credit card matching.

Once companies switch to BlackLine, away from the tedious methods of manual accounting, they find it incredibly difficult to leave the company's platform, as evidenced by its 98% customer renewal rate in 2018.

Global Payments

Global Payments offers payment processing services to businesses, allowing merchants to accept card and digital payments both online and at the point of sale. Payment processing is a fiercely competitive business where it is hard to stand out without massive scale that allows companies to compete at cost.

What Global Payments has managed to do, however, is embed its payment processing services in mission-critical, software vertical stacks in a variety of niche industries. CEO Jeff Sloan said he expects 60% of the company's revenue to come from this "technology-enabled distribution" by the conclusion of 2020.

Global Payments has done this through a series of partnerships and acquisitions to help it achieve this goal. For instance, in August 2017, the company acquired ACTIVE Network for about $1 billion, an athletic-event planning software platform whose customers include Ironman and the YMCA. In 2018, Global Payments purchased AdvancedMD for $700 million, which provides back-office software solutions for small, U.S.-based physicians offices.

By intertwining its payment services with these software platforms, Global Payments has given itself a successful software makeover, making it extremely costly for its customers to leave for a payment processing rival, especially in terms of training and convenience.

Mastercard

This global payments network hardly needs an introduction. Mastercard has more than 2.5 billion credit and debit cards in global circulation, almost all issued from financial institutions to account holders, and moves more than $1.5 trillion each quarter from purchases made using its cards. One of the best things about Mastercard's business model is that it is not directly exposed to any debt liability, removing one of the primary risks involved when investing in fintech companies discussed above.

This asset-light business model allows Mastercard -- and Visa, which shares a similar business model -- to sport an extremely high operating margin, which almost always comes in above 50%, which is the threshold that management lists as its long-term target. Such a high operating margin also allows Mastercard to invest heavily back into its business, including offering supplementary services to its enterprise clients. These services range from fraud prevention to loyalty program management to data analytics. By the end of 2018, this suite of services, collectively accounted for under the company's "Other revenues" segment, was its fastest-growing division and generating almost $1 billion per quarter.

These services, once sold to financial institutions, make it a difficult proposition for a company to consider leaving Mastercard's ecosystem. Once a customer is relying on Mastercard for payment services, fraud prevention, and other crucial services, it cannot easily decide to leave because a competitor is offering a slightly better price.

PayPal Holdings

PayPal operates a digital payments platform that lets its users transfer money via digital means as an alternative to using cash or writing checks. By the end of 2018, PayPal had reached a total of 267 million active user accounts, including 21 million merchant accounts. Management expects this total to surpass 300 million active users by 2020. The platform's fast-growing user base is quickly allowing the company to achieve a powerful network effect, meaning that its service gains in value the more users it has.

In a January 2019 conference call, CEO Dan Schulman stated:

[T]he virality of Venmo and the network effects on core PayPal are clearly coming into play. You've got 21 million-plus merchants accepting PayPal. Consumers see that, want to be a part of it. You've got 246 million-plus consumers using PayPal. Every merchant now wants to be a part of that. So you've got a good network effect both on core PayPal and on Venmo.

One of the primary drivers of PayPal's user growth is that its platform is completely agnostic to what bank users belong to, what device-maker or operating system users prefer, or which merchant the customer is shopping at. Consider a simple P2P payments example, where diners wish to split a bill. To use Apple Pay for this simple task, everyone would need to own an iPhone. For Zelle to be used, everyone would need to belong to a participating bank or credit union. PayPal is agnostic to all these elements, and the fact that its user base is so much larger than competitors' makes it the most likely platform (or its fast-growing Venmo subsidiary) to be used for such a task.

Investing in fintech

Technology is changing every industry, and its mark on the financial industry will be no less profound. Fintech is important as it democratizes crucial financial services to the world's underbanked population and lessens the cost for global consumers to move and manage their own money. These companies are not only offering catalysts for this change, they also offer investors the best chance to profit from these trends.

More From The Motley Fool

John Mackey, CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool's board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool's board of directors. Matthew Cochrane owns shares of Alibaba Group Holding Ltd., Alphabet (A shares), Amazon, BlackLine, Inc., Global Payments, JPMorgan Chase, Mastercard, NVIDIA, PayPal Holdings, and Square. The Motley Fool owns shares of and recommends Alphabet (A shares), Alphabet (C shares), Amazon, Apple, Intuit, MarketAxess Holdings, Mastercard, MercadoLibre, NVIDIA, PayPal Holdings, Q2 Holdings, Square, Visa, and Zillow Group (C shares). The Motley Fool owns shares of BlackLine, Inc and has the following options: long January 2020 $150 calls on Apple and short January 2020 $155 calls on Apple. The Motley Fool recommends Ultimate Software Group. The Motley Fool has a disclosure policy.