Can Blockchain Payment Platforms Become A Vanguard For Democracy?

Intensely disputed elections pose a bad omen for any society, both culturally and economically. With the solution in the form of blockchain staring us in the face, blockchain payment platforms can exert a pressure wave to adopt the innovative technology in voting as well.

Blockchain Exuberance Depleted?

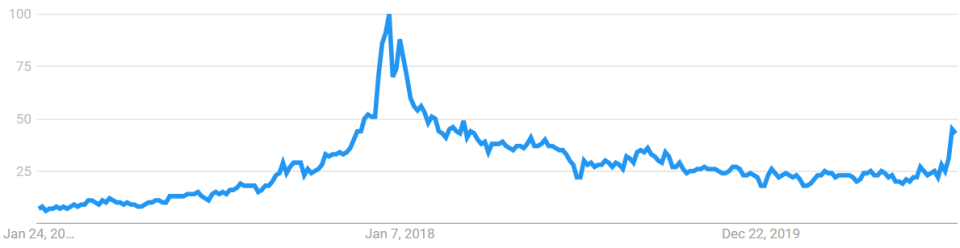

Those following the crypto space closely may remember a period when blockchain was the star of public conversation. Hundreds of articles had been written about blockchain as a revolutionary technology that was just about to penetrate every sector of human endeavor. From governmental agencies and military logistics to payment and voting systems, blockchain had been hailed as the next big thing after the internet itself.

Just take a look at the following Google Trends chart, which illustrates interest in the term “Blockchain” over the last five years:

Source: Google Trends

However, following that initial exuberance, a period of disillusionment settled in. This doesn’t mean that blockchain technology is not as important as it had been portrayed, but it does mean that the practical challenges it faces somewhat dampened the expectations for blockchain’s mainstream adoption. To understand why that is and where blockchain is heading, let’s quickly review its key features.

From age immemorial, whenever two parties traded with each other, the issue of trust always came up. Trust forms out of identity and security:

Ability to verify one’s identity so that feedback and reputation could occur, be it positive or negative.

Ability to securely complete a trade while incurring the lowest cost for that security possible.

From the bronze age to the digital age, people have tried their best to maximize those two pillars of trade. Deservedly so, blockchain entered the scene as the holy grail of transactions:

Each block in the interlinked chain records the nature (amount) of the transaction, participants’ identification (though pseudonymous to real-world identities), and timestamp of the transaction.

This record is impervious to manipulation because each block, with all the chains, is distributed across a publicly accessible network. In other words, this record– a distributed ledger–undergoes automatic verification across all the network’s nodes with each transaction.

The distributed record then becomes a permanent block in the chain, easily accessible at any time, without the possibility of being altered.

Ancient accountants would have marveled at such a financial innovation. Honest individuals may have even hailed it as perfection incarnated, while the dishonest would have been dismayed at the complete removal of possibility for financial books to be “fixed”.

Blockchain as a Guardian of Democracy?

When one understands blockchain, it is easy to grasp its many groundbreaking applications. Not just in the payments sector, but also in vital societal arenas such as voting. Across the globe, voting has always been a hot-button issue. In fact, governments tend to use voting irregularities in other countries as leverage to delegitimize those governments.

Belarus, Venezuela, Russia, Iran...any country that in some way opposes the United States’ interests can be delegitimized without any evidence. On the other hand, when there are accusations of election fraud in the US, other governments can’t employ the same leverage to the same effect.

Thanks to its immutability, decentralized security, and transparency, blockchain has all the key ingredients to clear up the air, both by removing the dishonest leverage by competing nations and by serving as an unparalleled force of legitimization. Given the fact that the last two presidential elections in the United States were intensely disputed, each from the opposite end of the political spectrum, there is clearly an urgent need for blockchain voting. That is, if social cohesion is to be maintained.

Fortunately, blockchain voting platforms are within our grasp if we only have the will to take advantage of them. By tying already established KYC (know-your-customer) identity verification protocols with private keys, blockchain voting can eliminate voting calculation errors, calculation speed, corruption, high cost, accessibility, and lack of ID verification.

Ready-to-go voting apps using blockchain are already present:

For example, Voatz had already been used in the 2018 West Virginia election for overseas voters. Likewise, in 2019 for Colorado, Denver, and Utah County. Needless to say, blockchain voting represents a severe obstacle for political parties to abuse the voting system, so it is difficult to say if such a system will ever be implemented as a default voting solution.

Considering that over 80% of Americans own a smartphone, in the context of 66% voter turnout for 2020 elections, the only remaining obstacle to what could be vastly superior blockchain voting is political will.

Blockchain’s Speed and Fees

Compared to blockchain voting, blockchain as a payment infrastructure seems a minor issue. After all, increased social instability due to lack of transparent voting ultimately yields a negative effect on the entire economy. However, there is no better way to mature blockchain technology, and help people trust it, than to use it in the payment arena. In turn, the people could demand its application in the political arena as well.

According to PwC’s report from 2020, the interest to transition to blockchain is certainly there. Unfortunately, this transition represents a departure from the existing legacy systems, which takes much development time and training. Consequently, based on the PwC’s survey, over half of respondents—57%—reported uncertainty on how to take full advantage of blockchain technology, despite being aware of its benefits:

“Blockchain systems could be far cheaper than existing platforms because they remove an entire layer of overhead dedicated to confirming authenticity. In a distributed ledger system, confirmation is effectively performed by everyone on the network, simultaneously. This so-called ‘consensus’ process reduces the need for existing intermediaries who touch the transaction and extract a toll in the process.”

Of the most pressing technical issues plaguing the still-early stage of blockchain is its transaction per second (TPS) speed. For example, the dominant cryptocurrency blockchain with a market cap that even surpassed Visa and MasterCard – Bitcoin (BTC) – can only handle 7 TPS. On the other hand, Visa can reach 24,000 TPS. Such an enormous capacity disparity yields a difference in seconds vs hours or even days.

Nonetheless, Bitcoin has been designed as a conservative deflationary currency serving the role of digital gold. Therefore, people don’t prioritize Bitcoin’s blockchain speed. For the purpose of transactions that can compete with the likes of Visa and SWIFT, other blockchains were developed:

Ethereum – a programmable blockchain responsible for creating smart contracts, which essentially means code is executed whenever predefined conditions are met. Its undergoing transition to Ethereum 2.0 should eventually yield a 4,000 TPS.

Ripple (XRP) – specifically designed as a rival to SWIFT infrastructure, it can handle 1,500 TPS, with a theoretical cap of 50,000.

Stellar (XLM) – a fork of Ripple capable of handling 1,000 TPS.

As you can see, these blockchain alternatives are still far removed from VISA’s 24,000 TPS. However, keep in mind that PayPal, the largest payment processor, can only handle 193 TPS. When we go over the 1,000 TPS threshold, we are talking about a matter of seconds, which is perfectly suitable for the vast majority of usage cases. Further, smart automated payment platforms, such as Wave, report no issues in quickly serving their customers.

In the end, people may prefer slower TPS to a higher transaction processing fee. Cumulatively, average credit card processing fees, 1.3 – 3.3%, can incur a high cost. According to the 2019 Federal Reserve Payments Study, an average American family must depart with roughly $1,800 for transaction fees alone. In contrast, the minimum fee offered by Ripple is 0.00001 XRP (~0.31USD), thus providing both fast and quick borderless transactions.

Can Blockchain Supplant the Existing Payments Systems?

The current barrier to blockchain adoption as a payment system is one of maturation. Multiple blockchain ecosystems are in the game, signifying that one cannot deploy one blockchain for all purposes. This makes it difficult for financial institutions and developers to dedicate themselves to a single blockchain solution. As we have seen with the success of eToro, thanks largely to its CopyTrader feature, people don’t like closed ecosystems. Instead, they prefer to reach across the aisle to maximize their trading performance.

After all, if they develop a proprietary blockchain, they will likely end up in a closed ecosystem, with a high likelihood of another alternative emerging with even lower fees, at faster speeds. The most obvious solution to this problem is open-source blockchain interoperability - facilitating payments across blockchains. Interledger Protocol STREAM seems to be the future for this model going forward.

Moreover, the incentive to harness such blockchain interoperability has never been stronger. After the decision by the OCC to allow US banks to access public blockchains, and serve themselves as ledger nodes, we should expect to see an intensified penetration of blockchain into payment platforms. As this momentum builds up, people will demand blockchain’s fortifying property to be applied to other areas of human congress - voting.

See more from Benzinga

© 2021 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.