Should You Buy Douglas Emmett, Inc. (NYSE:DEI) For Its Upcoming Dividend In 4 Days?

It looks like Douglas Emmett, Inc. (NYSE:DEI) is about to go ex-dividend in the next 4 days. Investors can purchase shares before the 27th of September in order to be eligible for this dividend, which will be paid on the 16th of October.

Douglas Emmett's next dividend payment will be US$0.3 per share. Last year, in total, the company distributed US$1.0 to shareholders. Calculating the last year's worth of payments shows that Douglas Emmett has a trailing yield of 2.5% on the current share price of $42.3. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! So we need to investigate whether Douglas Emmett can afford its dividend, and if the dividend could grow.

Check out our latest analysis for Douglas Emmett

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Fortunately Douglas Emmett's payout ratio is modest, at just 42% of profit. While Douglas Emmett seems to be paying out a very high percentage of its income, REITs have different dividend payment behaviour and so, while we don't think this is great, we also don't think it is unusual. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. Thankfully its dividend payments took up just 39% of the free cash flow it generated, which is a comfortable payout ratio.

It's positive to see that Douglas Emmett's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

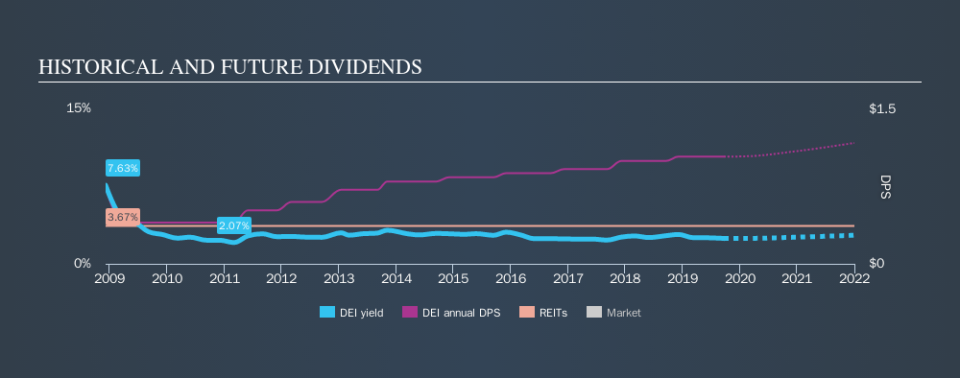

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. For this reason, we're glad to see Douglas Emmett's earnings per share have risen 17% per annum over the last five years. Earnings per share have been growing rapidly and the company is retaining a majority of its earnings within the business. Fast-growing businesses that are reinvesting heavily are enticing from a dividend perspective, especially since they can often increase the payout ratio later.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. In the past ten years, Douglas Emmett has increased its dividend at approximately 3.3% a year on average. Earnings per share have been growing much quicker than dividends, potentially because Douglas Emmett is keeping back more of its profits to grow the business.

The Bottom Line

Has Douglas Emmett got what it takes to maintain its dividend payments? It's great that Douglas Emmett is growing earnings per share while simultaneously paying out a low percentage of both its earnings and cash flow. It's disappointing to see the dividend has been cut at least once in the past, but as things stand now, the low payout ratio suggests a conservative approach to dividends, which we like. Overall we think this is an attractive combination and worthy of further research.

Curious what other investors think of Douglas Emmett? See what analysts are forecasting, with this visualisation of its historical and future estimated earnings and cash flow.

A common investment mistake is buying the first interesting stock you see. Here you can find a list of promising dividend stocks with a greater than 2% yield and an upcoming dividend.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.