CarParts.com vs O’Reilly: Which Auto Retailer Is Poised To Rally Ahead?

Recent results of used-car retailers are indicating consumers’ preference to travel in their own vehicle rather than using public transportation amid rising COVID-19 cases. Also, in a challenging macro environment, consumers prefer maintaining their existing vehicles or buying used cars rather than new cars due to limited spending capacity.

The demand for aftermarket auto parts is also rising at a strong rate mainly because of people spending extra time at home amid the pandemic on DIY repairs and maintenance projects.

Keeping in mind the rising demand in the aftermarket auto parts space, we will use the TipRanks Stock Comparison tool to compare CarParts.com and O’Reilly Automotive and see which retailer is a better pick in the current environment.

CarParts.com (PRTS)

CarParts.com is an e-commerce company that aims to provide a seamless factory-to-consumer online shopping experience. Following its inclusion in the Russell 2000 Index, the company changed its name from U.S. Auto Parts Network to CarParts.com in July to reflect the way it has leveraged technology and e-commerce expertise to increase sales and profitability.

The company directly reaches the customers through its own distribution network, thus cutting out much of the brick-and-mortar supply chain costs. This enables it to offer auto parts and accessories at competitive prices. A notable aspect of CarParts.com is that it also sells its products through third-party marketplaces. Sales on eBay and Amazon accounted for 34.9% of total sales in the first half of 2020.

Pandemic-induced demand changed CarParts.com’s fortunes. The company’s sales grew 39% in the first half of this year following a 3% sales decline in full-year 2019. Notably, sales surged 61.4% to $118.9 million in 2Q driven by triple-digit revenue growth in the company’s flagship website CarParts.com (the company earlier operated other websites too but has now consolidated them into one).

Online sales (includes e-commerce and online marketplace channels) grew about 69% and contributed about 95% of 2Q sales. Meanwhile, offline sales (includes sales from the company’s private-label brand Kool-Vue and wholesale operations) fell 9.6% due to lower sales from wholesale operations.

Meanwhile, 2Q gross margin expanded 480 basis points Y/Y to 34.3% and marked the sixth consecutive quarter of gross margin improvement for the company. The 2Q gross margin was driven by favorable product mix and supply chain optimizations. Strong sales and margin expansion helped the company deliver EPS of $0.03 in 2Q20 compared to a loss per share of $0.04 in 2Q19.

CarParts.com’s expanded distribution footprint, improved site speed and faster shipping times are helping it in meeting the increased demand for auto parts amid the pandemic. On the 2Q conference call, the company said that even after the reopening of the economy after lockdowns, demand continues to be strong and is outpacing supply.

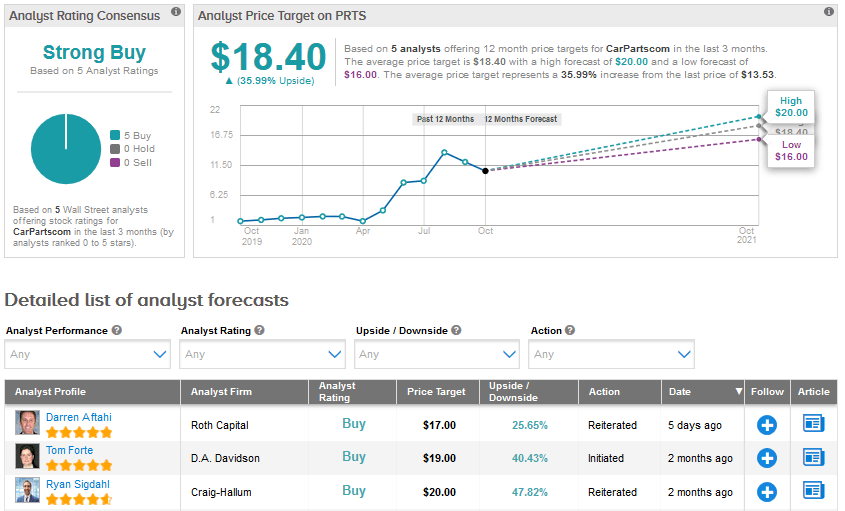

Commenting about the upcoming 3Q results, Roth Capital analyst Darren Aftahi stated “3Q traffic trends to Carparts.com showed improvement q/q from 2Q levels, suggesting strong results could be on the horizon.”

Aftahi reiterated a Buy rating with a price target of $17 and said that he expects revenue growth of about 43.6%, gross margin of about 34.6% and a net loss of $0.01 per share in 3Q. (See PRTS stock analysis on TipRanks)

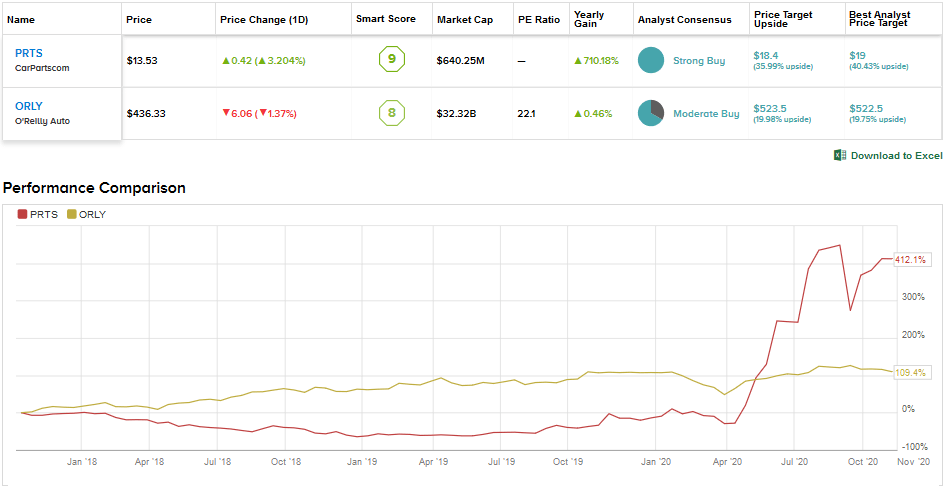

Carparts.com scores a Strong Buy rating from the Street based on 5 unanimous Buys. Shares have surged by a staggering 515% year-to-date and the average analyst price target of $18.40 indicates further upside potential of about 36% in the coming months.

O’Reilly Automotive (ORLY)

O’Reilly Automotive is one of the largest aftermarket auto parts specialty retailers and operates 5,592 stores in the US and 21 stores in Mexico. The company also sells its products through its e-commerce site. O’Reilly’s performance has been quite consistent. It has delivered comparable sales growth for 27 consecutive years and double-digit EPS growth for 11 straight years.

The company’s first-quarter sales growth of 2.7% reflected the impact of lockdowns. But, business bounced back in 2Q and sales grew 19.4%. Aside from pandemic-induced demand for auto parts, O’Reilly and its peers have also credited government stimulus and unemployment benefits for the growing demand in the aftermarket auto parts industry in recent months.

On Oct. 28, O’Reilly reported better-than-expected 3Q results. Sales grew 20.3% to $3.2 billion with comparable sales rising 16.9% on strong DIY demand. The company said that its professional or DIFM (do-it-for-me) business also performed better-than-anticipated. The 3Q EPS increased 39.2% Y/Y to $7.07 driven by higher sales and increased operating margin.

The company’s operating margin expanded 250 basis points Y/Y to 22.6% in 3Q driven by strong sales and expense management. However, gross margin contracted 96 basis points Y/Y to 52.4% as the comparable quarter in the prior year gained from sell-through of pre-tariff on-hand inventory. Also, the lower gross margin sales from the acquired Mayasa stores impacted the 3Q gross margin.

Following the upbeat performance in the recent quarters, O’Reilly raised its share repurchase authorization by $1 billion, bringing the overall authorization under its buyback program to $14.75 billion.

Looking ahead at 4Q, O’Reilly stated that comparable store sales are so far strong and are trending slightly below its 3Q exit rate in the low double-digit range.

Meanwhile, O’Reilly continues to expand its store fleet. It opened 153 net new stores in the first nine months of 2020. The company also opened a distribution center in Lebanon, Tennessee in 1Q and plans to open another facility in Horn Lake, Mississippi, in the first half of 2021.

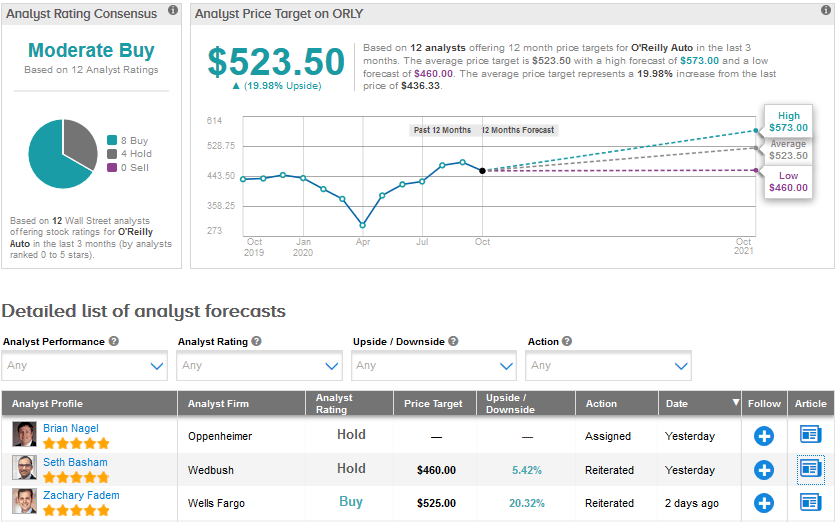

Following the earnings release, Wells Fargo analyst Zachary Fadem reiterated a Buy rating and a price target of $525 for O'Reilly, saying “While gross margin (-96bps) could prove the single blemish on an otherwise exceptional print, we believe ORLY is taking outsized share and anticipate another round of upward EPS revisions. All in, we continue to view auto part retailers as underappreciated in today’s environment, and are constructive on ORLY’s best-in-class execution, non-discretionary assortment and NT [near time] upside from share gains and incremental stimulus.”

The analyst also said that he sees “increasingly favorable risk/reward and would be aggressive buyers on weakness.” (See ORLY stock analysis on TipRanks)

The Street is cautiously optimistic about O’Reilly. A Moderate Buy consensus for the stock is based on 8 Buys and 4 Holds with no Sells. The average analyst price target of $523.50 indicates an upside potential of about 20% to the current levels. Shares are down 0.46% year-to-date.

Conclusion

O’Reilly is a consistent performer and a well-established auto parts retailer. However, in the current business environment, CarParts.com’s e-commerce business model looks lucrative. Right now, CarParts.com stock appears to be more attractive than O’Reilly as reflected by the Street’s highly bullish stance and greater upside potential in the stock.

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment