Central Bankers in Bunkers Keep Ukraine’s War Economy Afloat

(Bloomberg) -- The deputy governor of Ukraine’s central bank woke early on Feb. 24 to a phone call from his mother, who was abroad. Her flight back to Kyiv had been cancelled. She’d also seen news reports that Russian tanks had crossed the border.

Most Read from Bloomberg

US Says 3 Mystery Objects Likely Private, With No China Link

America's Priciest Neighborhoods Are Changing as the Ultra-Rich Move to Florida

US Scrambles Jets for ‘Routine’ Intercept of Russian Warplanes

New Cars Are Only for the Rich Now as Automakers Rake In Profits

Minutes later, Serhiy Nikolaychuk was racing to the office for an emergency meeting. Thus began a year in which he and his colleagues — more accustomed to supervising banks and targeting inflation from the peaceful confines of a boardroom — would find themselves managing a war economy by pulling monetary policy levers as much in hope as belief.

“I had several feelings: One was fear for my family, and my second was a huge sense of responsibility,” recalled Nikolaychuk, 41. “I realized that something really horrible is happening and keeping the financial system afloat would be the challenge of a lifetime.”

It’s been a tricky 12 months for monetary-policy makers across the world given inflation and the threat of recession. But that turbulence barely registers compared with having to flee a city under siege, assess interest rates from safe houses and secure a loan from a bomb shelter.

The National Bank of Ukraine in Kyiv already had a tough enough job steering an economy dependent on foreign aid through internal political wrangling and endemic corruption. Those challenges were replaced by how to operate while at risk of bombardment and how to make sure events on the battlefield didn’t cloud its judgement with no end to the conflict in sight.

As Vladimir Putin upended the post-Cold War order, the central bank’s board and several department chiefs gathered on the first day of the invasion in the red and grey Russian revival style palace in Ukraine’s government quarter. The initial task was to quickly approve Decree No. 18, a list of 16 emergency measures to prevent panic, shore up the banking system and impose capital controls.

The document, whose wording was quickly finalized in a brainstorming huddle, included a 100,000 hryvnia ($2,708) daily limit on cash withdrawals for households, a ban on withdrawing foreign currency and a freeze of the official exchange rate. By 10 a.m. Kyiv time it was in force. Next was to ensure the transactions system kept working, according to Kateryna Rozhkova, a first deputy governor.

“I was fully focused — there was no fear,” said Rozhkova, 50. What’s more, having experienced a financial crisis after Russia annexed Crimea in 2014, the bank had stashed reserves in excess of $27.5 billion, she said. “This time, we had a buffer including foreign reserves and financial sustainability, and we used this buffer.”

Then came the war effort: The bank created an account for donations to the military and even coordinated the delivery of armored cash transport trucks from commercial banks to the army.

After that, everything ground to a halt. Putin’s invasion turned the economy on its head, cutting off supply lines. It shut down entire industries as millions of Ukrainians flooded out of the combat zones to safety in western Ukraine or abroad. Rozhkova remembered hurrying through a deserted Kyiv among metal tank traps and the smoking sites of missile strikes.

“That was amid the news of the occupation of Ukrainian cities like Mariupol and Melitopol, horrible things were happening,” Rozhkova said. “You realize that it’s not happening somewhere far away, it is near you, and you know that not from the newspapers, but from your own experience.”

President Volodymyr Zelenskiy and his entourage have gained international kudos — as well as more rounds of military aid — for their resistance to Russia, as have the troops on the front line. But between the top of government and the resilience of ordinary Ukrainians, the actions of central bankers and state bureaucrats have just about managed to keep the country functioning.

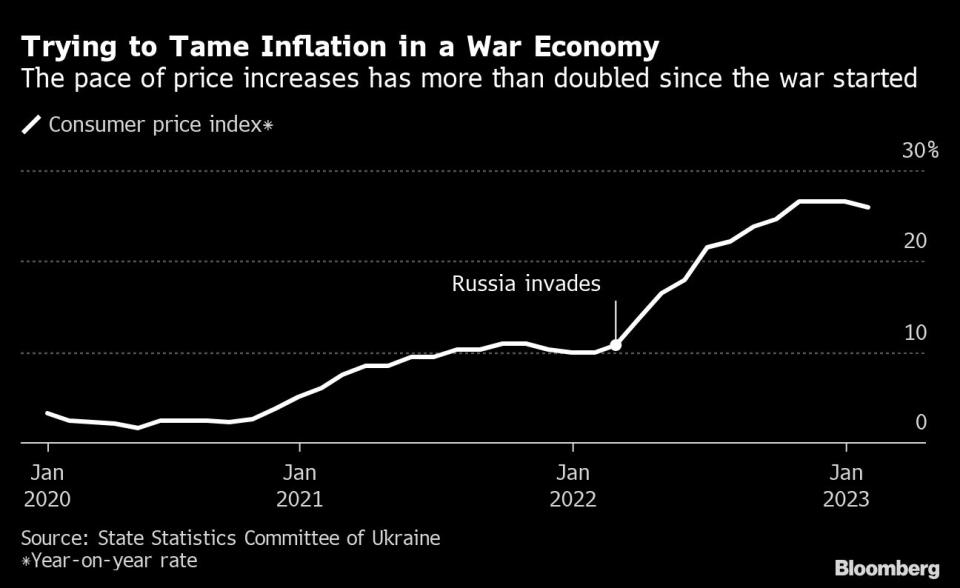

As Russian forces attacked Kyiv, the National Bank of Ukraine’s board delayed a decision on monetary policy on March 3, freezing the key rate at 10%. It said it would go back to inflation-targeting and a floating exchange rate after Ukraine was “freed from Russian invaders.”

The next move came on June 2, when they hiked it to 25%. The bank said it had to more than double borrowing costs to shore up the currency, stabilize the economy and stem soaring inflation.

At the same time, it admitted that the ordinary tools of monetary policy had lost their effectiveness because of the war, which drove more than a third of Ukrainians from their homes and devastated businesses. Moreover, the invasion has made any economist's task of trying to model the future via indicators such as unemployment and retail sales just about impossible.

The benchmark remains at that level today, with the hryvnia locked to a peg against the dollar that the bank had to devalue by 20% in July to protect its foreign-currency reserves.

Another issue undermining monetary policy is a dispute with the Finance Ministry. While the central bank raised interest rates, the ministry has refused to match them when selling debt to avoid paying much higher costs. The result is that lenders prefer to park their excess funds in the central bank’s higher-yielding deposit certificates instead of lending them to the government — or anyone else — closer to market rates.

“The cost of making a mistake, given the circumstances, has risen,” Andriy Pyshnyi, the central bank’s governor, said in an interview in December as air-raid sirens sounded across Kyiv. “This makes me spend more time on analysis and designing decisions than when there was peace.”

That peace vanished in a moment. Nikolaychuk told his friends that everything was pointing toward an invasion and to be ready. Everyone in the central bank had been briefed and prepared — “go bags” packed with essentials near the door and plans for evacuations out of Kyiv if necessary.

It was still a shock when it happened, he said. “After giving advice to everyone, I was not ready at all,” he said with a laugh over dinner at a restaurant in the city last month.

The bank evacuated staff in an 18-hour trip through traffic jams to an undisclosed location in western Ukraine. Later, they moved to Lviv, a city close to the Polish border.

In between, there were many moments in shelters, a far cry from the varnished table in their regular boardroom at the National Bank of Ukraine headquarters. In March, an air-raid alarm interrupted a crucial call on securing a $1.4 billion emergency-aid deal with the International Monetary Fund. So the officials headed underground to safety.

“The board had gathered in front of the laptop in a narrow four-square-meter room and continued consultations,” Nikolaychuk said. “I think the IMF’s team was impressed.”

There was also a new display of professional solidarity. Former Governor Kyrylo Shevchenko had angered his colleagues and drawn criticism from Zelenskiy and the IMF for his authoritarian style and for pushing out reform-minded personnel.

Rozhkova said they put the disagreement aside, citing a line from Rudyard Kipling’s “The Jungle Book:” Enemies don’t fight at watering holes in times of drought. “Now we’ll have water truce,” Rozhkova said she told Shevchenko. “After the war ends, we’ll return to our former positions.”

That didn’t transpire, though. Shevchenko was accused of misappropriation of funds from a state lender he once ran. He stepped down and was replaced by Pyshnyi in October and has since left Ukraine. He has denied wrongdoing and said he didn’t want to comment on private matters when reached by Bloomberg.

Almost a year later, the economy is mired in the devastation of war. The final 2022 tally included a more than 30% drop in gross domestic product, inflation exceeding 26% and the central bank eating into its reserves.

But as the conflict has changed, and so have the central bank’s worries. Despite a campaign of rocket and drone strikes against civilian infrastructure including the energy grid, Ukrainians are now used to bombardments and air-raid sirens, often ignoring shelters.

At the central bank, fears of being hit by a cruise missile or that fleeing Ukrainians would trigger a bank run have been replaced by concern that blackouts may paralyze banks. To keep its staff safe — and ready — the central bank now has a well-equipped shelter below downtown Kyiv that includes family living quarters so that critical staff can stay overnight.

While Ukrainians look for ways to help with the effort to thwart Russia, Nikolaychuk is grateful he has a clearly defined purpose away from the fog of war. “It was a big advantage that we had this mission,” he said. “You had to be focused on making decisions in the most efficient way. You realized that this is your contribution to the resilience of the country and future victory.”

--With assistance from Jody Megson.

Most Read from Bloomberg Businessweek

Aiming to Be the Next Emirates, Air India Makes Record Jet Buy

China’s ‘Zero-Dollar’ Tourists Are Getting a Cautious Welcome

Survey Response Rates Are Down Since Covid. That's Worrying For US Economic Data.

©2023 Bloomberg L.P.