Central Bankers Used to Keep Out of Politics. Not Any More

- Oops!Something went wrong.Please try again later.

- Oops!Something went wrong.Please try again later.

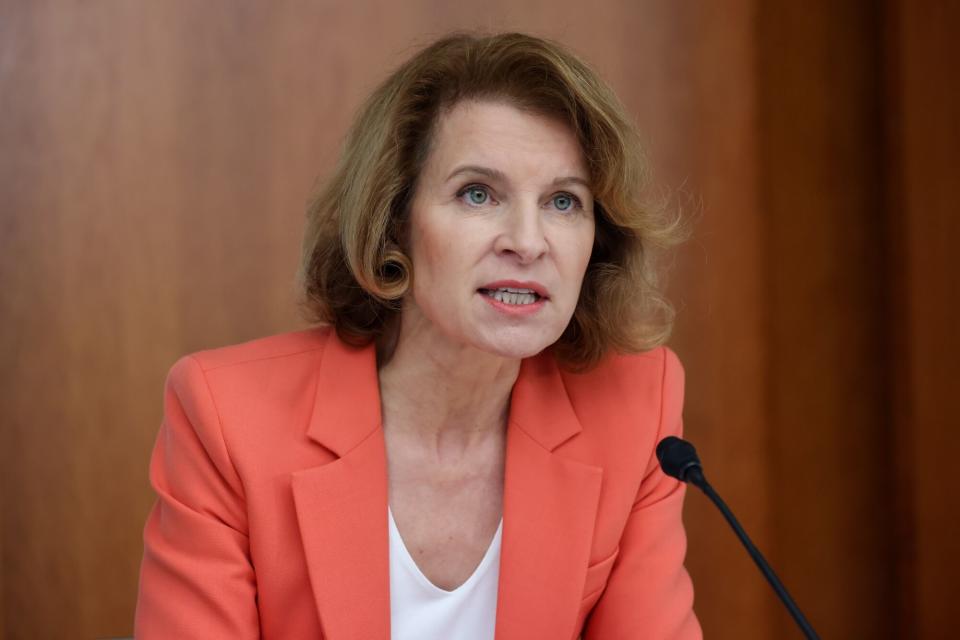

(Bloomberg) -- Bundesbank board member Sabine Mauderer stepped uneasily from side to side as she waited to speak.

Most Read from Bloomberg

Apple to Wind Down Electric Car Effort After Decadelong Odyssey

How Much Wealth You Need to Join the Richest 1% Around the World

Flawed Valuations Threaten $1.7 Trillion Private Credit Boom

Supreme Court to Weigh Trump Immunity, Keeps DC Trial Paused

From the stage she could watch the crowds of anti-fascist demonstrators filling Frankfurt’s central square and hear the chants that have rung out across Germany in response to the rise of the far-right AfD. Such rallies have become common this year after a surge in its support. But for a central banker to speak at one is unusual, still, and risky.

Central banks consider their independence sacrosanct. The European Central Bank says it couldn’t successfully target inflation without it. But monetary policymakers are starting to test that independence as they grapple with the threat from populists in a year of elections around the globe.

Mauderer, 53, who joined the Bundesbank after climbing the ranks in risk management and compliance, was about to step into the most contentious political debate that Germany has faced for years. “Anti-democratic groups are dividing our society,” she told the throngs gathered in Frankfurt. “They’re damaging Germany’s reputation in the world.”

The Bundesbank’s statutes — like those of the ECB — are designed to protect central bankers from the interference of democratically elected officials, and not the other way around. The taboo against these technocrats involving themselves in politics operates mainly as a matter of convention, and it’s beginning to fray.

This year Bundesbank President Joachim Nagel and ECB Executive Board member Isabel Schnabel have both joined demonstrations like the one Mauderer spoke at. The continent’s chief monetary guardian, Christine Lagarde, has been vocal on a theme that deters more cautious colleagues, repeatedly lashing out against the threat a Donald Trump reelection would pose to European stability.

The central banks portray these actions as apolitical: “The commitment of Sabine Mauderer and Joachim Nagel against xenophobia and exclusion is in line with the independence of the German Bundesbank,” a spokesperson said, in response to Bloomberg questions. “As representatives of a large federal agency, they see it as their duty to defend the basic democratic values of our country.”

The defense of democratic principles should be uncontroversial, essentially.

But another lesson Europeans gleaned from the Trump presidency is that that isn’t always the case. In Germany, in particular, the argument that taking a stand against xenophobia and exclusion constitutes a vanilla civic duty is complicated by the presence of a political party that’s making both those things central to its offer to voters.

All the more so when a huge chunk of the population is rushing to support it. The AfD or Alternative for Germany, whose far-right politics were once seen as a fringe concern, has lately climbed to second place in nationwide polls.

On the subject of speaking out, the ECB toes a similar line to its Frankfurt neighbor. “ECB Executive Board members, as representatives of a European Union institution, support and stand for EU values such as mutual respect, dignity and freedom from discrimination,” a spokesperson said.

Some analysts regard these actions a little differently.

“It’s about self-preservation,” said Leah Downey, a Cambridge University academic who writes about the politics of monetary policy. “Central banking involves making political decisions disguised as technocracy all the time. Now populists are beginning to pose a threat to that technocratic privilege, policymakers are having to get explicitly political.”

In less guarded moments, Lagarde has herself been frank about the stakes. Regarding her censure of the possible next president of the US, she told CNN that being “politically correct” on the Trump question entails “a risk of not seeing the reality and preparing for it.”

The ECB president has said it’s a regime of punitive tariffs that she fears, and she has good reason. Should he retake office, Trump plans to target the EU with a slew of combative trade measures, Bloomberg has reported.

Although assaults on the ECB from inside the 20-nation euro zone have been comparatively harmless compared to what peers outside it endure, looking over at these precedents may encourage policymakers to see attack as the best form of defense. From Thailand to Turkey, a series of high profile controversies about the pressure heaped on monetary policymakers has sharpened the debate.

In Europe, one risk is that officials make themselves a target for the same extremists they’re seeking to deter. On Tuesday the AfD accused the Bundesbank of costing German taxpayers billions by mishandling its bond-buying program — a distorted take on the complex matter of central-bank accounting, but one that may gain traction with voters all the same.

The erosion of central-bank independence is, to some degree, a return to the historical norm. Although Milton Friedman and others mooted the independence of monetary policy from government objectives as early as the 1960s, it only became a standard across much of the developed world thirty years later.

Still, it ought to be no surprise that politicians and central bankers are at odds right now, according to Volker Wieland, a professor of monetary economy at Goethe University Frankfurt and a former member of Germany’s council of economic advisers.

“There are times when monetary policy and fiscal policies are aligned in their objectives,” he said — such as during the pandemic. “More recently, however, with high inflation partly due to expansionary policies, monetary tightening was needed to help ensure a sustained return to price stability, while fiscal authorities remained reluctant to step back from expansionary policies.”

The division between monetary and fiscal competences was blurred by the Great Financial Crisis, the sovereign-debt crisis that followed and the Covid-19 pandemic. Policymakers stepped in as lender of last resort — not only to banks but governments as well, buying trillions of euros of debt issued to fund aid packages. Under Lagarde, the ECB has also jumped into fighting climate change, something that was — at least initially — a controversial course.

“What’s left is a gray area between politics and central banking that’s getting wider, muddier and harder to navigate,” said David Marsh, chairman of the Official Monetary and Financial Institutions Forum. That’s why, he said, “central bankers must think very carefully about what they say, and try to make things better rather than worse.”One reason there are few rules preventing central bankers from opining on politics is that democratically elected officials are at greater liberty to ignore them. The ECB’s code of conduct enjoins independence on its members not for the politicians’ sakes but because of reputational risk to the institutions themselves.

Whether policymakers categorize their actions as political, they must grapple with the fact that others do. And politicians may be especially emboldened to tell monetary officials to butt out when the latter are falling short on their day jobs.

“We need to have less politics and more price stability,” was the advice to Lagarde of European parliament member Engin Eroglu earlier this week. “Everything else you should leave to politicians.”

The ECB president’s statements about Trump have precedent in the intervention of former Federal Reserve Bank of New York President William Dudley, who in 2019 provoked backlash when he wrote in a Bloomberg opinion piece that policymakers “should consider how their decisions will affect the political outcome in 2020.” Former Treasury Secretary Lawrence Summers said at the time it “might be the least responsible statement by a former financial official in decades.”

Lagarde’s recent anti-Trump tirades haven’t sparked similar outrage. Maybe because — as the former President’s campaign suggested — Americans don’t care about “a handful of people in Europe.” Maybe it’s because people are used to her not mincing her words. And it may be partly because the notion of central banks as apolitical institutions is starting to invite less and less credence.

“It seems like the heyday of central-bank independence is gone,” said Michael Gavin, a researcher at the University of Ottawa who together with his Toronto University colleague Mark Manger has documented the ratcheting of populist pressures on monetary policymakers. “If I were a central banker in Europe, I’d be sticking my neck out now and trying to get ahead of it.”

--With assistance from Simon White.

Most Read from Bloomberg Businessweek

Elon Musk’s Vegas Tunnel Project Has Been Racking Up Safety Violations

China’s Piano Dreams Are Fading for a Cash-Strapped Middle Class

Hollywood Is Banking on Dune: Part Two to Revive the Blockbuster Experience

©2024 Bloomberg L.P.