Is China Tian Lun Gas Holdings (HKG:1600) A Risky Investment?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about. It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, China Tian Lun Gas Holdings Limited (HKG:1600) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for China Tian Lun Gas Holdings

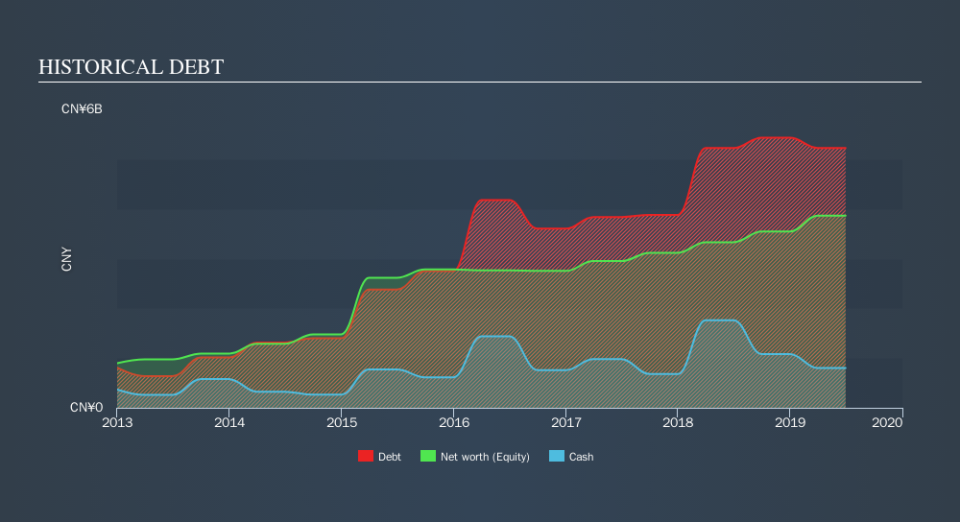

How Much Debt Does China Tian Lun Gas Holdings Carry?

As you can see below, China Tian Lun Gas Holdings had CN¥5.22b of debt, at June 2019, which is about the same the year before. You can click the chart for greater detail. On the flip side, it has CN¥798.8m in cash leading to net debt of about CN¥4.43b.

How Healthy Is China Tian Lun Gas Holdings's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that China Tian Lun Gas Holdings had liabilities of CN¥3.22b due within 12 months and liabilities of CN¥4.54b due beyond that. On the other hand, it had cash of CN¥798.8m and CN¥2.14b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥4.82b.

This deficit is considerable relative to its market capitalization of CN¥6.68b, so it does suggest shareholders should keep an eye on China Tian Lun Gas Holdings's use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

China Tian Lun Gas Holdings's debt is 2.5 times its EBITDA, and its EBIT cover its interest expense 6.1 times over. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. Notably, China Tian Lun Gas Holdings's EBIT launched higher than Elon Musk, gaining a whopping 109% on last year. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine China Tian Lun Gas Holdings's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, China Tian Lun Gas Holdings reported free cash flow worth 19% of its EBIT, which is really quite low. That limp level of cash conversion undermines its ability to manage and pay down debt.

Our View

When it comes to the balance sheet, the standout positive for China Tian Lun Gas Holdings was the fact that it seems able to grow its EBIT confidently. But the other factors we noted above weren't so encouraging. For example, its conversion of EBIT to free cash flow makes us a little nervous about its debt. We would also note that Gas Utilities industry companies like China Tian Lun Gas Holdings commonly do use debt without problems. Looking at all this data makes us feel a little cautious about China Tian Lun Gas Holdings's debt levels. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of China Tian Lun Gas Holdings's earnings per share history for free.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.