Column: Painful signs emerge that Fed is moving too far, too fast with aggressive rate increases

We have a term for the intentional infliction of pain on others: cruelty. So what are we to make of the Federal Reserve Board?

The Fed, in statements associated with its campaign to bring down inflation, has referred to the challenge of bringing about a "soft landing" — that is, reducing inflation without significantly slowing the economy or even provoking a recession.

Asked at his news conference Wednesday about the consequences of the Fed's efforts at "restoring price stability," Fed Chairman Jerome H. Powell replied that "no one knows whether this process will lead to a recession or if so, how significant that recession would be."

The present danger...is not so much that current and planned moves will fail eventually to quell inflation. It is that they collectively go too far and drive the world economy into an unnecessarily harsh contraction.

Economist Maurice Obstfeld

Powell's comments came directly after the Fed board voted to increase interest rates by a historically high three-quarters of a percentage point, its third such monthly increase in a row.

Few would disagree that bringing the inflation rate down from its current annual rate of more than 8% is imperative.

As Powell observed, the question is how to do so without imposing the pain of the process on those least able to shoulder it — job holders, especially those with lower-income jobs who might be the first to be fired in a recession.

What may be more pertinent to the current economic situation is whether the Fed's rate increases thus far this year have already achieved a good part of its goal. The answer to that is: We don't know.

That's why a growing chorus of economic experts is saying that the danger of the Fed's policy is no longer that it won't move aggressively enough to cool price increases, but that it is moving too aggressively.

Their argument is that the Fed, like other central banks that have followed its lead in raising rates, has not given its prior rate increases time to take effect.

The truth is that inflation already has cooled significantly on a month-to-month basis. The consumer price index in July did not rise at all from its level in June. In August, overall prices rose a mere 0.1% from July. Curiously, economic commentators interpreted the August figure, which was announced Sept. 13, as a "hot" increase.

That provoked expectations that the Fed would respond with another three-quarters of a percentage point increase in rates, as it did a few days later. Yet the month-to-month changes in the CPI were the lowest since October 2020, when the U.S. economy was still mired in a pandemic-triggered slump.

The consequences of overshooting the inflation mark could be dire.

We reported this summer on the alarming notion, increasingly popular among economic policy wonks, that inflation could not be brought down without an increase in unemployment along with a slowdown in wage growth.

Its most uncompromising iteration came from former Treasury Secretary Lawrence H. Summers, who told a London audience that “we need five years of unemployment above 5% to contain inflation — in other words, we need two years of 7.5% unemployment or five years of 6% unemployment or one year of 10% unemployment.” (The U.S. unemployment rate, as measured in August, was 3.7%.)

Powell appears to have accepted this general idea, if not Summers' specific figures. "We’re never going to say that there are too many people working," he said Wednesday. "We have got to get inflation behind us. I wish there were a painless way to do that — there isn’t."

As translated by Ben Carlson of Ritholtz Wealth Management and the economics blog A Wealth of Common Sense, Powell's words were: "We’re not saying there are too many people working but we’re also not not saying that." (Emphasis mine.)

The Fed's evident determination to forge ahead with a policy undermining economic growth, at least in the short and medium term, has rattled stock investors. The benchmark Standard & Poor's 500 index has fallen about 24% during the rate-tightening cycle this year, placing it firmly in a bear market.

As veteran market watchers know, it's not the prospect of an economic slowdown that creates bear markets, but uncertainty about where the Fed intends to take us. (Stock prices tend to rise when there's a consensus about economic prospects, whether they're good or bad — it's doubt that causes market downturns.)

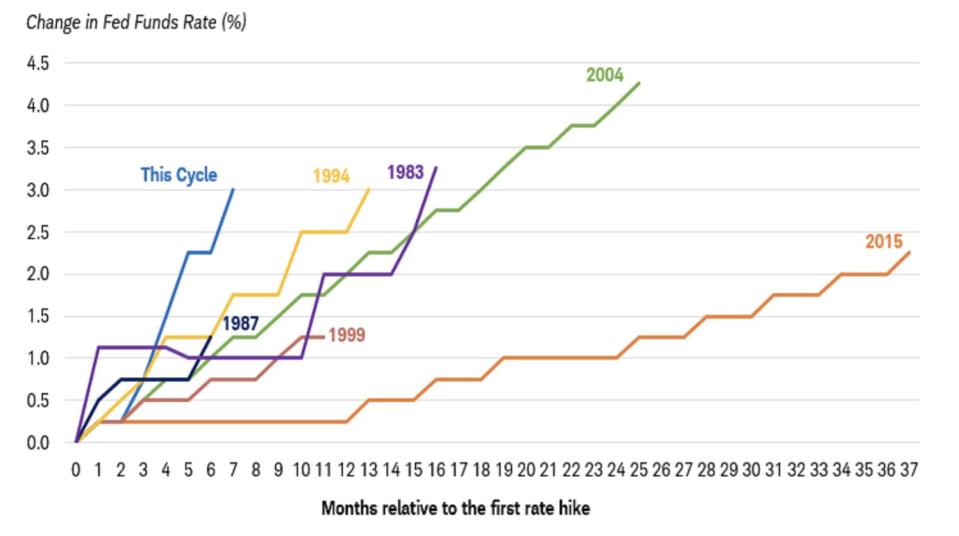

The Fed's current tightening is the fastest since the early 1980s, observes Kathy Jones, an interest rate expert at Charles Schwab & Co.

"The rapid pace of tightening raises the risks of a more significant downturn in the economy in the near term," Jones wrote after the last rate increase. "Monetary policy works with a lag. Changes in interest rates today can take a year or more to have a significant impact on the economy. Since this has been the fastest rate hiking cycle in decades, a lot of tightening has already taken place and may have yet to work its way through the economy."

Jones isn't alone in warning about the risk of central banks' overshooting their inflation-reduction targets. Others point to the dangers of so many central banks raising rates in tandem: the Bank of England, the European Central Bank and the Bank of Canada have all raised rates in unison with the Fed.

The central bankers are understandably stung by the accusation that they waited too long to quell inflation by raising rates and cooling their economies.

"Central banks nearly everywhere feel accused of being on the back foot," Maurice Obstfeld, a former chief economist at the International Monetary Fund and former chair of the economics department at UC Berkeley, wrote recently.

"The present danger, however, is not so much that current and planned moves will fail eventually to quell inflation," Obstfeld wrote. "It is that they collectively go too far and drive the world economy into an unnecessarily harsh contraction. Just as central banks ... misread the factors driving inflation when it was rising in 2021, they may also be underestimating the speed with which inflation could fall as their economies slow."

Economic statistics show that the Fed's interest rate increases already have had an effect on economic activity and on inflation. As my colleague Andrew Khouri has reported, home sales in Southern California have slowed sharply, with sales of new and existing houses, condos and town homes dropping in August by 28.3% from a year earlier.

The same phenomenon has emerged nationwide, plainly in response to mortgage rates that have surged above 6%, more than doubling from a year earlier; the issuance of new building permits fell in August by 14.4% from the level of August 2021.

It's proper to question, however, whether the Fed is reading the numbers correctly — or even reading the right numbers.

Powell acknowledged that the U.S. economy has slowed markedly, with real economic growth (that is, accounting for inflation) now projected at a mere 0.2% this year and 1.2% in 2023. He cited slowdowns in consumer spending growth, "reflecting lower real disposable income and tighter financial conditions." He noted that the housing sector had "weakened significantly."

Powell didn't mention this during his Wednesday news conference, but the public's expectations of inflation a year ahead have fallen, from 6.8% in June to 5.75% in August, according to the New York Federal Reserve Bank.

That probably reflects the sharp decline in gasoline prices, which are prime carriers of inflation fears, but it's a welcome sign that inflation expectations aren't becoming embedded in consumer behavior, a phenomenon that keeps central bankers awake at night.

Yet Powell and his colleagues don't seem to have absorbed the prospect that the slowdown in inflation currently will show up in annual figures in fairly short order, even though that's basic math (as the year progresses, the abnormally high monthly increases of late 2021 and earlier this year, peaking at 1.2% in March over February, will fall away and the more recent, modest increases will take their place.

Nor do they appear to recognize that much of what drove inflation over the last year wasn't the tightness in the job market but the unnatural constrictions in international supply chains and gasoline production, which have largely ebbed. In any case, the Fed's ability to influence those factors by raising interest rates was effectively zero.

Instead, they are reverting to the economic responses of the 19th century and the early 20th century, when the answer to price increases was to liquidate labor. Powell repeatedly argues that the labor market must accept pain now so it will be stronger in the future — "Reducing inflation is likely to require a sustained period of below-trend growth, and there will very likely be some softening of labor market conditions," he counseled Wednesday.

"The inflation rate is certainly high by historical standards, but it has clearly peaked," observes economist James W. Paulsen of the Leuthold Group, a research house for institutional investors. "Evidence across a wide variety of measures — commodity prices, wage inflation, most core inflation gauges, import prices, tech prices, vehicle prices, trucking and shipping rates, and retail price discounts due to high and rising inventories — imply that inflation is decelerating."

Normally, these trends would signal that the Fed should pause its tightening regime, at least temporarily. Despite that, the Fed is still sounding extremely hawkish notes in its projections of future rates.

In other words, we have to destroy the economic village in order to save it. Does this make sense? Millions of workers whose jobs and lives are upended in the name of a healthier economy for the survivors won't think so.

This story originally appeared in Los Angeles Times.