Companies Like Mirriad Advertising (LON:MIRI) Can Afford To Invest In Growth

We can readily understand why investors are attracted to unprofitable companies. For example, Mirriad Advertising (LON:MIRI) shareholders have done very well over the last year, with the share price soaring by 253%. But the harsh reality is that very many loss making companies burn through all their cash and go bankrupt.

Given its strong share price performance, we think it's worthwhile for Mirriad Advertising shareholders to consider whether its cash burn is concerning. For the purpose of this article, we'll define cash burn as the amount of cash the company is spending each year to fund its growth (also called its negative free cash flow). The first step is to compare its cash burn with its cash reserves, to give us its 'cash runway'.

Check out our latest analysis for Mirriad Advertising

How Long Is Mirriad Advertising's Cash Runway?

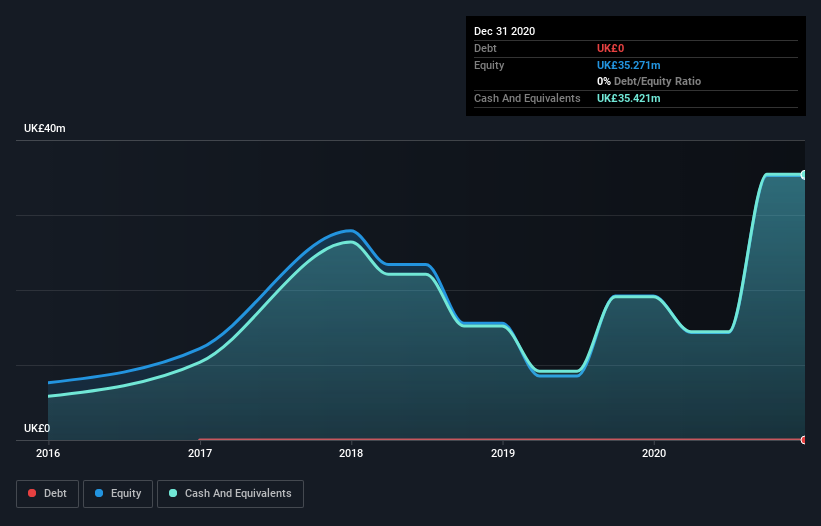

A company's cash runway is calculated by dividing its cash hoard by its cash burn. As at December 2020, Mirriad Advertising had cash of UK£35m and no debt. Looking at the last year, the company burnt through UK£8.1m. Therefore, from December 2020 it had 4.4 years of cash runway. A runway of this length affords the company the time and space it needs to develop the business. You can see how its cash balance has changed over time in the image below.

How Well Is Mirriad Advertising Growing?

It was fairly positive to see that Mirriad Advertising reduced its cash burn by 27% during the last year. Having said that, the revenue growth of 91% was considerably more inspiring. It seems to be growing nicely. While the past is always worth studying, it is the future that matters most of all. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

How Easily Can Mirriad Advertising Raise Cash?

We are certainly impressed with the progress Mirriad Advertising has made over the last year, but it is also worth considering how costly it would be if it wanted to raise more cash to fund faster growth. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. Commonly, a business will sell new shares in itself to raise cash and drive growth. By looking at a company's cash burn relative to its market capitalisation, we gain insight on how much shareholders would be diluted if the company needed to raise enough cash to cover another year's cash burn.

Mirriad Advertising's cash burn of UK£8.1m is about 5.8% of its UK£139m market capitalisation. Given that is a rather small percentage, it would probably be really easy for the company to fund another year's growth by issuing some new shares to investors, or even by taking out a loan.

So, Should We Worry About Mirriad Advertising's Cash Burn?

It may already be apparent to you that we're relatively comfortable with the way Mirriad Advertising is burning through its cash. In particular, we think its revenue growth stands out as evidence that the company is well on top of its spending. Its cash burn reduction wasn't quite as good, but was still rather encouraging! After taking into account the various metrics mentioned in this report, we're pretty comfortable with how the company is spending its cash, as it seems on track to meet its needs over the medium term. Its important for readers to be cognizant of the risks that can affect the company's operations, and we've picked out 3 warning signs for Mirriad Advertising that investors should know when investing in the stock.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies, and this list of stocks growth stocks (according to analyst forecasts)

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.