Consider This Before Buying HCI Group, Inc. (NYSE:HCI) For The 3.5% Dividend

Could HCI Group, Inc. (NYSE:HCI) be an attractive dividend share to own for the long haul? Investors are often drawn to strong companies with the idea of reinvesting the dividends. On the other hand, investors have been known to buy a stock because of its yield, and then lose money if the company's dividend doesn't live up to expectations.

In this case, HCI Group likely looks attractive to dividend investors, given its 3.5% dividend yield and nine-year payment history. It sure looks interesting on these metrics - but there's always more to the story . The company also bought back stock equivalent to around 4.5% of market capitalisation this year. When buying stocks for their dividends, you should always run through the checks below, to see if the dividend looks sustainable.

Click the interactive chart for our full dividend analysis

Payout ratios

Companies (usually) pay dividends out of their earnings. If a company is paying more than it earns, the dividend might have to be cut. Comparing dividend payments to a company's net profit after tax is a simple way of reality-checking whether a dividend is sustainable. Looking at the data, we can see that 106% of HCI Group's profits were paid out as dividends in the last 12 months. A payout ratio above 100% is definitely an item of concern, unless there are some other circumstances that would justify it.

We update our data on HCI Group every 24 hours, so you can always get our latest analysis of its financial health, here.

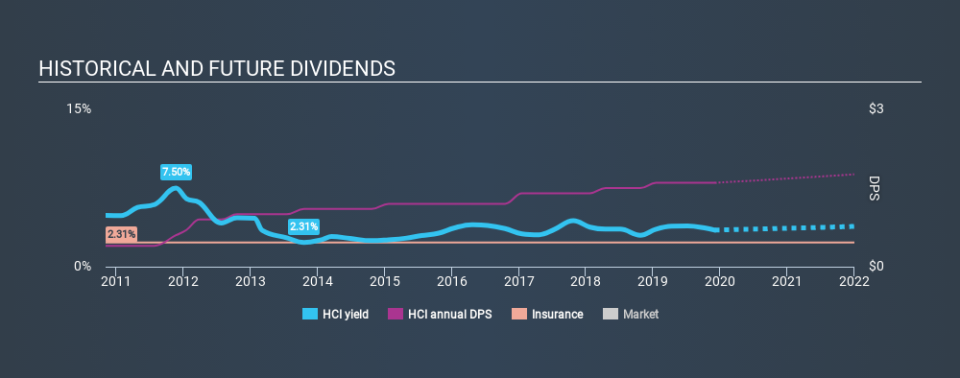

Dividend Volatility

Before buying a stock for its income, we want to see if the dividends have been stable in the past, and if the company has a track record of maintaining its dividend. Looking at the last decade of data, we can see that HCI Group paid its first dividend at least nine years ago. Its dividend has not fluctuated much that time, which we like, but we're conscious that the company might not yet have a track record of maintaining dividends in all economic conditions. During the past nine-year period, the first annual payment was US$0.40 in 2010, compared to US$1.60 last year. Dividends per share have grown at approximately 17% per year over this time.

HCI Group has been growing its dividend quite rapidly, which is exciting. However, the short payment history makes us question whether this performance will persist across a full market cycle.

Dividend Growth Potential

While dividend payments have been relatively reliable, it would also be nice if earnings per share (EPS) were growing, as this is essential to maintaining the dividend's purchasing power over the long term. Over the past five years, it looks as though HCI Group's EPS have declined at around 24% a year. With this kind of significant decline, we always wonder what has changed in the business. Dividends are about stability, and HCI Group's earnings per share, which support the dividend, have been anything but stable.

Conclusion

When we look at a dividend stock, we need to form a judgement on whether the dividend will grow, if the company is able to maintain it in a wide range of economic circumstances, and if the dividend payout is sustainable. First, it's not great to see how much of its earnings are being paid as dividends. Earnings per share are down, and to our mind HCI Group has not been paying a dividend long enough to demonstrate its resilience across economic cycles. With any dividend stock, we look for a sustainable payout ratio, steady dividends, and growing earnings. HCI Group has a few too many issues for us to get interested.

Now, if you want to look closer, it would be worth checking out our free research on HCI Group management tenure, salary, and performance.

Looking for more high-yielding dividend ideas? Try our curated list of dividend stocks with a yield above 3%.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.