Some Delfi (SGX:P34) Shareholders Have Taken A Painful 80% Share Price Drop

Some stocks are best avoided. We don't wish catastrophic capital loss on anyone. Anyone who held Delfi Limited (SGX:P34) for five years would be nursing their metaphorical wounds since the share price dropped 80% in that time. And we doubt long term believers are the only worried holders, since the stock price has declined 50% over the last twelve months. The falls have accelerated recently, with the share price down 27% in the last three months. But this could be related to the weak market, which is down 25% in the same period.

While a drop like that is definitely a body blow, money isn't as important as health and happiness.

See our latest analysis for Delfi

In his essay The Superinvestors of Graham-and-Doddsville Warren Buffett described how share prices do not always rationally reflect the value of a business. By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

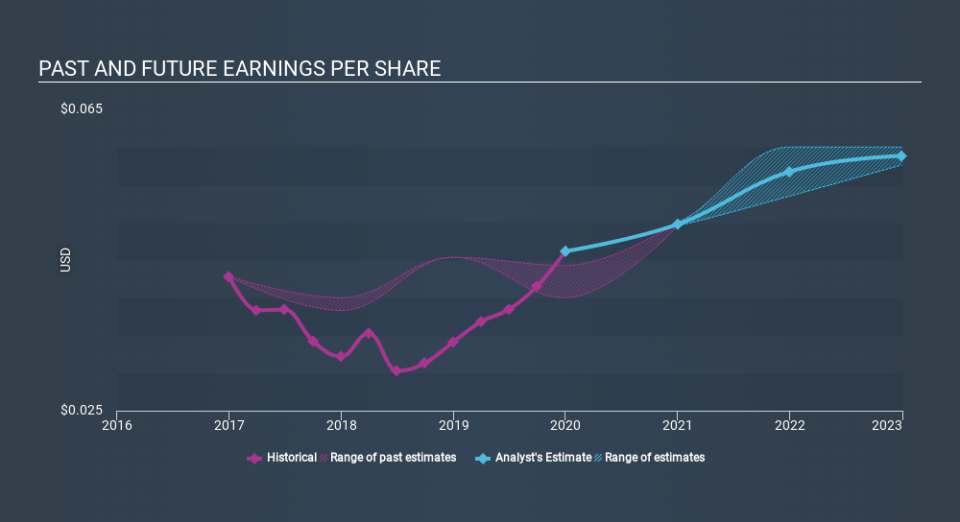

During the five years over which the share price declined, Delfi's earnings per share (EPS) dropped by 10% each year. This reduction in EPS is less than the 28% annual reduction in the share price. So it seems the market was too confident about the business, in the past. The low P/E ratio of 11.05 further reflects this reticence.

The graphic below depicts how EPS has changed over time (unveil the exact values by clicking on the image).

We know that Delfi has improved its bottom line lately, but is it going to grow revenue? If you're interested, you could check this free report showing consensus revenue forecasts.

What About Dividends?

As well as measuring the share price return, investors should also consider the total shareholder return (TSR). Whereas the share price return only reflects the change in the share price, the TSR includes the value of dividends (assuming they were reinvested) and the benefit of any discounted capital raising or spin-off. It's fair to say that the TSR gives a more complete picture for stocks that pay a dividend. As it happens, Delfi's TSR for the last 5 years was -77%, which exceeds the share price return mentioned earlier. And there's no prize for guessing that the dividend payments largely explain the divergence!

A Different Perspective

We regret to report that Delfi shareholders are down 49% for the year (even including dividends) . Unfortunately, that's worse than the broader market decline of 22%. However, it could simply be that the share price has been impacted by broader market jitters. It might be worth keeping an eye on the fundamentals, in case there's a good opportunity. Unfortunately, last year's performance may indicate unresolved challenges, given that it was worse than the annualised loss of 26% over the last half decade. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. It's always interesting to track share price performance over the longer term. But to understand Delfi better, we need to consider many other factors. For example, we've discovered 2 warning signs for Delfi that you should be aware of before investing here.

For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on SG exchanges.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.