Despite Its High P/E Ratio, Is PSC Insurance Group Limited (ASX:PSI) Still Undervalued?

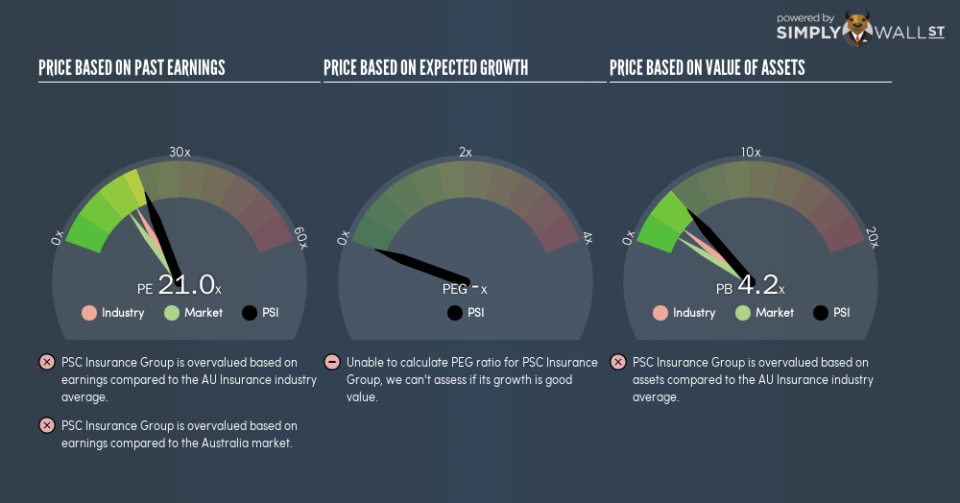

The goal of this article is to teach you how to use price to earnings ratios (P/E ratios). To keep it practical, we’ll show how PSC Insurance Group Limited’s (ASX:PSI) P/E ratio could help you assess the value on offer. PSC Insurance Group has a P/E ratio of 21.04, based on the last twelve months. In other words, at today’s prices, investors are paying A$21.04 for every A$1 in prior year profit.

View our latest analysis for PSC Insurance Group

Want to help shape the future of investing tools and platforms? Take the survey and be part of one of the most advanced studies of stock market investors to date.

How Do You Calculate A P/E Ratio?

The formula for price to earnings is:

Price to Earnings Ratio = Price per Share ÷ Earnings per Share (EPS)

Or for PSC Insurance Group:

P/E of 21.04 = A$2.44 ÷ A$0.12 (Based on the year to June 2018.)

Is A High Price-to-Earnings Ratio Good?

A higher P/E ratio means that investors are paying a higher price for each A$1 of company earnings. All else being equal, it’s better to pay a low price — but as Warren Buffett said, ‘It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.’

How Growth Rates Impact P/E Ratios

Earnings growth rates have a big influence on P/E ratios. That’s because companies that grow earnings per share quickly will rapidly increase the ‘E’ in the equation. Therefore, even if you pay a high multiple of earnings now, that multiple will become lower in the future. A lower P/E should indicate the stock is cheap relative to others — and that may attract buyers.

Notably, PSC Insurance Group grew EPS by a whopping 33% in the last year. And its annual EPS growth rate over 5 years is 28%. I’d therefore be a little surprised if its P/E ratio was not relatively high.

How Does PSC Insurance Group’s P/E Ratio Compare To Its Peers?

The P/E ratio essentially measures market expectations of a company. As you can see below, PSC Insurance Group has a higher P/E than the average company (17.1) in the insurance industry.

PSC Insurance Group’s P/E tells us that market participants think the company will perform better than its industry peers, going forward. Clearly the market expects growth, but it isn’t guaranteed. So further research is always essential. I often monitor director buying and selling.

Remember: P/E Ratios Don’t Consider The Balance Sheet

Don’t forget that the P/E ratio considers market capitalization. That means it doesn’t take debt or cash into account. Theoretically, a business can improve its earnings (and produce a lower P/E in the future), by taking on debt (or spending its remaining cash).

Such expenditure might be good or bad, in the long term, but the point here is that the balance sheet is not reflected by this ratio.

Is Debt Impacting PSC Insurance Group’s P/E?

Since PSC Insurance Group holds net cash of AU$107m, it can spend on growth, justifying a higher P/E ratio than otherwise.

The Bottom Line On PSC Insurance Group’s P/E Ratio

PSC Insurance Group’s P/E is 21 which is above average (14.6) in the AU market. With cash in the bank the company has plenty of growth options — and it is already on the right track. So it is not surprising the market is probably extrapolating recent growth well into the future, reflected in the relatively high P/E ratio.

Investors should be looking to buy stocks that the market is wrong about. As value investor Benjamin Graham famously said, ‘In the short run, the market is a voting machine but in the long run, it is a weighing machine.’ So this free report on the analyst consensus forecasts could help you make a master move on this stock.

But note: PSC Insurance Group may not be the best stock to buy. So take a peek at this free list of interesting companies with strong recent earnings growth (and a P/E ratio below 20).

To help readers see past the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price-sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned. For errors that warrant correction please contact the editor at editorial-team@simplywallst.com.