Does Estia Health Limited (ASX:EHE) Have A Place In Your Dividend Stock Portfolio?

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Dividend paying stocks like Estia Health Limited (ASX:EHE) tend to be popular with investors, and for good reason - some research suggests a significant amount of all stock market returns come from reinvested dividends. If you are hoping to live on the income from dividends, it's important to be a lot more stringent with your investments than the average punter.

With a goodly-sized dividend yield despite a relatively short payment history, investors might be wondering if Estia Health is a new dividend aristocrat in the making. We'd agree the yield does look enticing. Some simple research can reduce the risk of buying Estia Health for its dividend - read on to learn more.

Explore this interactive chart for our latest analysis on Estia Health!

Payout ratios

Companies (usually) pay dividends out of their earnings. If a company is paying more than it earns, the dividend might have to be cut. So we need to form a view on if a company's dividend is sustainable, relative to its net profit after tax. Estia Health paid out 99% of its profit as dividends, over the trailing twelve month period. With a payout ratio this high, we'd say its dividend is not well covered by earnings. This may be fine if earnings are growing, but it might not take much of a downturn for the dividend to come under pressure.

In addition to comparing dividends against profits, we should inspect whether the company generated enough cash to pay its dividend. Estia Health paid out 205% of its free cash flow last year, suggesting the dividend is poorly covered by cash flow. Paying out such a high percentage of cash flow suggests that the dividend was funded from either cash at bank or by borrowing, neither of which is desirable over the long term. Cash is slightly more important than profit from a dividend perspective, but given Estia Health's payouts were not well covered by either earnings or cash flow, we would definitely be concerned about the sustainability of this dividend.

Is Estia Health's Balance Sheet Risky?

As Estia Health's dividend was not well covered by earnings, we need to check its balance sheet for signs of financial distress. A rough way to check this is with these two simple ratios: a) net debt divided by EBITDA (earnings before interest, tax, depreciation and amortisation), and b) net interest cover. Net debt to EBITDA measures a company's total debt load relative to its earnings (lower = less debt), while net interest cover measures the company's ability to pay the interest on its debt (higher = greater ability to pay interest costs). Estia Health has net debt of less than two times its earnings before interest, tax, depreciation, and amortisation (EBITDA), which we think is not too troublesome.

Net interest cover can be calculated by dividing earnings before interest and tax (EBIT) by the company's net interest expense. With EBIT of 13.29 times its interest expense, Estia Health's interest cover is quite strong - more than enough to cover the interest expense.

We update our data on Estia Health every 24 hours, so you can always get our latest analysis of its financial health, here.

Dividend Volatility

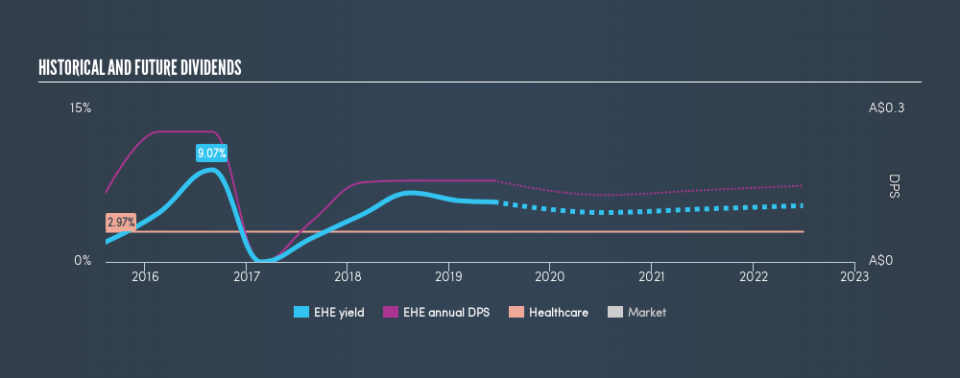

Before buying a stock for its income, we want to see if the dividends have been stable in the past, and if the company has a track record of maintaining its dividend. Estia Health has been paying a dividend for the past four years. It has only been paying dividends for a few short years, and the dividend has already been cut at least once. This is one income stream we're not ready to live on. During the past four-year period, the first annual payment was AU$0.14 in 2015, compared to AU$0.16 last year. This works out to be a compound annual growth rate (CAGR) of approximately 4.1% a year over that time. The growth in dividends has not been linear, but the CAGR is a decent approximation of the rate of change over this time frame.

We're glad to see the dividend has risen, but with a limited rate of growth and fluctuations in the payments, we don't think this is an attractive combination.

Dividend Growth Potential

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. It's good to see Estia Health has been growing its earnings per share at 67% a year over the past 5 years. Earnings per share have been growing very rapidly, although the company is also paying out virtually all of its profit in dividends. Generally, a company that is growing rapidly while paying out a majority of its earnings, is seeing its debt burden increase. We'd be conscious of any extra risk added by this practice.

Conclusion

Dividend investors should always want to know if a) a company's dividends are affordable, b) if there is a track record of consistent payments, and c) if the dividend is capable of growing. It's a concern to see that the company paid out such a high percentage of its earnings and cashflow as dividends. Next, earnings growth has been good, but unfortunately the dividend has been cut at least once in the past. With this information in mind, we think Estia Health may not be an ideal dividend stock.

Companies that are growing earnings tend to be the best dividend stocks over the long term. See what the 6 analysts we track are forecasting for Estia Health for free with public analyst estimates for the company.

We have also put together a list of global stocks with a market capitalisation above $1bn and yielding more 3%.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.