Does FNM (BIT:FNM) Have A Healthy Balance Sheet?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies FNM S.p.A. (BIT:FNM) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for FNM

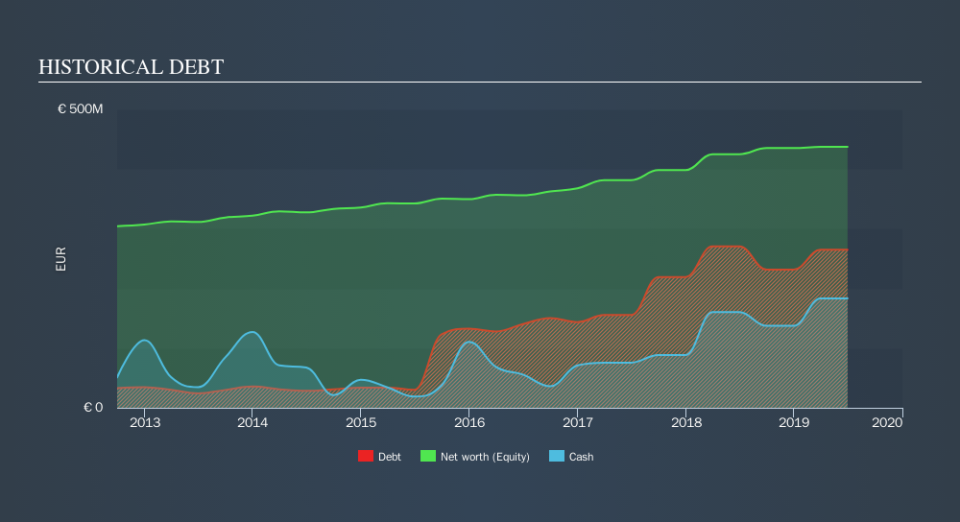

How Much Debt Does FNM Carry?

The image below, which you can click on for greater detail, shows that FNM had debt of €264.9m at the end of June 2019, a reduction from €282.2m over a year. However, because it has a cash reserve of €183.4m, its net debt is less, at about €81.5m.

How Healthy Is FNM's Balance Sheet?

According to the last reported balance sheet, FNM had liabilities of €305.8m due within 12 months, and liabilities of €218.5m due beyond 12 months. Offsetting these obligations, it had cash of €183.4m as well as receivables valued at €181.9m due within 12 months. So it has liabilities totalling €159.1m more than its cash and near-term receivables, combined.

This deficit is considerable relative to its market capitalization of €230.1m, so it does suggest shareholders should keep an eye on FNM's use of debt. This suggests shareholders would heavily diluted if the company needed to shore up its balance sheet in a hurry.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

FNM's net debt is only 1.2 times its EBITDA. And its EBIT covers its interest expense a whopping 18.6 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. Fortunately, FNM grew its EBIT by 6.7% in the last year, making that debt load look even more manageable. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since FNM will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Looking at the most recent three years, FNM recorded free cash flow of 38% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Our View

On our analysis FNM's interest cover should signal that it won't have too much trouble with its debt. However, our other observations weren't so heartening. For example, its level of total liabilities makes us a little nervous about its debt. Looking at all this data makes us feel a little cautious about FNM's debt levels. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. Given FNM has a strong balance sheet is profitable and pays a dividend, it would be good to know how fast its dividends are growing, if at all. You can find out instantly by clicking this link.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.