Does PetroChina (HKG:857) Have A Healthy Balance Sheet?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital. It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies PetroChina Company Limited (HKG:857) makes use of debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for PetroChina

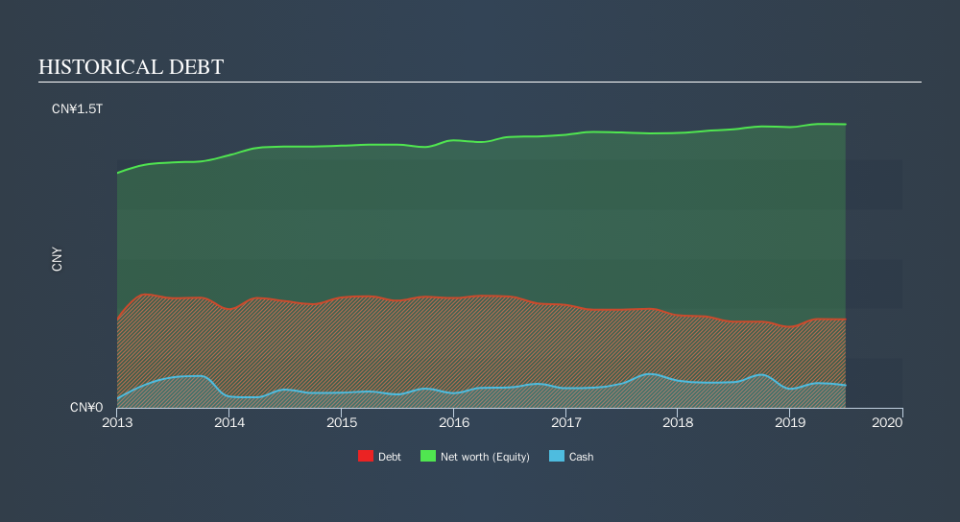

What Is PetroChina's Net Debt?

As you can see below, PetroChina had CN¥444.7b of debt, at June 2019, which is about the same the year before. You can click the chart for greater detail. However, because it has a cash reserve of CN¥112.8b, its net debt is less, at about CN¥331.8b.

How Healthy Is PetroChina's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that PetroChina had liabilities of CN¥602.3b due within 12 months and liabilities of CN¥609.3b due beyond that. On the other hand, it had cash of CN¥112.8b and CN¥82.8b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥1.02t.

This is a mountain of leverage even relative to its gargantuan market capitalization of CN¥1.06t. This suggests shareholders would heavily diluted if the company needed to shore up its balance sheet in a hurry.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

While PetroChina's low debt to EBITDA ratio of 0.88 suggests only modest use of debt, the fact that EBIT only covered the interest expense by 6.9 last year does give us pause. So we'd recommend keeping a close eye on the impact financing costs are having on the business. Another good sign is that PetroChina has been able to increase its EBIT by 29% in twelve months, making it easier to pay down debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if PetroChina can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, PetroChina recorded free cash flow worth a fulsome 82% of its EBIT, which is stronger than we'd usually expect. That positions it well to pay down debt if desirable to do so.

Our View

The good news is that PetroChina's demonstrated ability to convert EBIT to free cash flow delights us like a fluffy puppy does a toddler. But the stark truth is that we are concerned by its level of total liabilities. Looking at all the aforementioned factors together, it strikes us that PetroChina can handle its debt fairly comfortably. Of course, while this leverage can enhance returns on equity, it does bring more risk, so it's worth keeping an eye on this one. Another positive for shareholders is that it pays dividends. So if you like receiving those dividend payments, check PetroChina's dividend history, without delay!

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.