What does the rising rate of inflation mean for you?

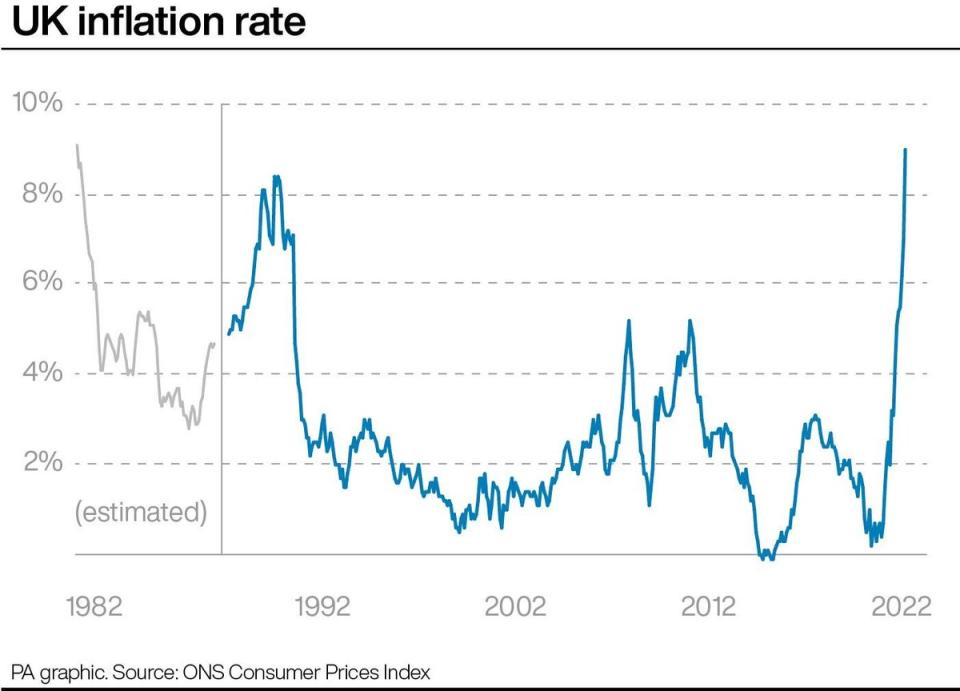

UK inflation has surged to 9.1 per cent for the 12 months to May, taking it to its highest level for 40 years, as the cost of living crisis continues to bite.

The situation will likely get worse before it improves, with the Bank of England already forecasting the rate of inflation to hit 11 per cent this year.

The present spike means that the price of everyday items like staple foods – particularly fruit and vegetables – fuel, clothing, shoes and furniture have all climbed over the last year, a development that threatens to hit low-income families hardest at a time when they can least afford it.

Charities have already reported increased sales of and demand for second-hand clothes in response to increased production costs driving high street fashion to its priciest levels since 1988 when records began.

“Clothing and footwear pushed inflation up this month and although there were still the traditional price drops, it was the smallest January fall since 1990, with fewer sales than last year,” said Grant Fitzner, chief economist at the Office for National Statistics (ONS).

“The rising costs of some household goods and increases in rents also pushed up inflation. However, these were partially offset by lower prices at the pump, following record highs at the end of 2021.

“Some annual changes this year are affected by last year’s lockdown, when many services were unavailable.”

Rising costs, staff shortages and supply chain disruption are known to be affecting both big name retail brands and small businesses alike, leaving them with little choice, as they see it, but to pass on price rises to consumers to ensure their own survival.

Cost of living: How to get help

The cost of living crisis has touched every corner of the UK, pushing families to the brink with rising food and fuel prices.

The Independent has asked experts to explain small ways you can stretch your money,including managing debt and obtaining items for free.

If you need to access a food bank, find your local council’s website usinggov.uk and then use the local authority’s site to locate your nearest centre.The Trussell Trust, which runs many food banks, has a similar tool.

Citizens Advice provides free help to people in need. The organisation can help you find grants or benefits, or advise on rent, debt and budgeting.

If you are experiencing feelings of distress and isolation, or are struggling to cope, The Samaritans offers support; you can speak to someone for free over the phone, in confidence, on 116 123 (UK and ROI), email jo@samaritans.org, or visit the Samaritans website to find details of your nearest branch.

Richard Walker, managing director of Iceland, responded to the latest hike by observing: “People who are already worrying about how to feed their families, while also wrestling with other rising living costs, will see these latest inflation figures as yet more cause for concern and anxiety.

“Sadly, it’s also a situation that I think will only worsen as the year progresses – and so the government, alongside retailers, must take action now to support hard-pressed customers.”

ONS data has meanwhile revealed the extent to which UK wages have stagnated, which meant that workers effectively took a pay cut in the final three months of 2021 when their daily living expenses outpaced salary growth.

Total pay growth did rise to 4.3 per cent for the quarter to December – from 4.2 per cent for the three months to November – but nevertheless continued to lag behind inflation, which was then at 5.4 per cent.

“The good news is that the UK economy is continuing to create jobs,” said Matthew Percival, director for people and skills at the CBI. “The bad news is that businesses are struggling to hire and pay is failing to keep up with inflation.”

All of this follows on from Ofgem’s announcement in February that the energy price cap, the maximum amount a utility company can charge an average customer per year, would rise by 54 per cent from 1 April in response to soaring global gas prices, landing UK households with an almost £700 annual increase in their electricity and gas bills.

Since that date, the cap has increased from £1,277 to £1,971 for a household on average usage. Prepayment meter customers have meanwhile seen an increase of £708 from £1,309 to £2,017.

Chancellor Rishi Sunak responded to that development by unveiling an aid package for British households worth a combined £350 in an attempt to soothe the “sting” of rocketing bills but, for many, his intervention was dismissed as a case of too little, too late.

Subsequently responding to the inflation rise, Mr Sunak said the government was listening to people’s concerns over what he insisted were “global challenges” and cited his discount and rebate bundle to address energy bills as evidence of state support for struggling families.

“We’re also helping people on the lowest incomes keep more of what they earn by cutting the universal credit taper rate and freezing alcohol and fuel duties to keep costs down,” he added.

“In total, we’re providing support with the cost of living worth over £20bn across this financial year and next.”

But that is likely to prove cold comfort to thousands of British consumers on flatlining wages facing higher costs for everything from food, clothing, petrol, heating, national insurance and housing and rent at a time when rising interest rates mean the cost of borrowing is going up too.

While the current outlook appears bleak indeed, consumers are being encouraged to treat the present adversity, which will ultimately pass, as an opportunity to reassess their personal circumstances, streamline their finances and cut out any inessential regular outgoings.

“The most important thing savers can do now is review how this environment will affect their finances, where they are keeping their savings, and make adjustments as necessary,” said Colin Dyer, client director at Abrdn Financial Planning.

“For example, holding significant amounts of cash in a deposit account is effectively losing money in an inflationary environment, so depending on attitude to risk, investing in a stocks and shares ISA may provide a greater return if investing for the longer term.”