Does Valmet Oyj (HEL:VALMT) Have A Healthy Balance Sheet?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Valmet Oyj (HEL:VALMT) makes use of debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Valmet Oyj

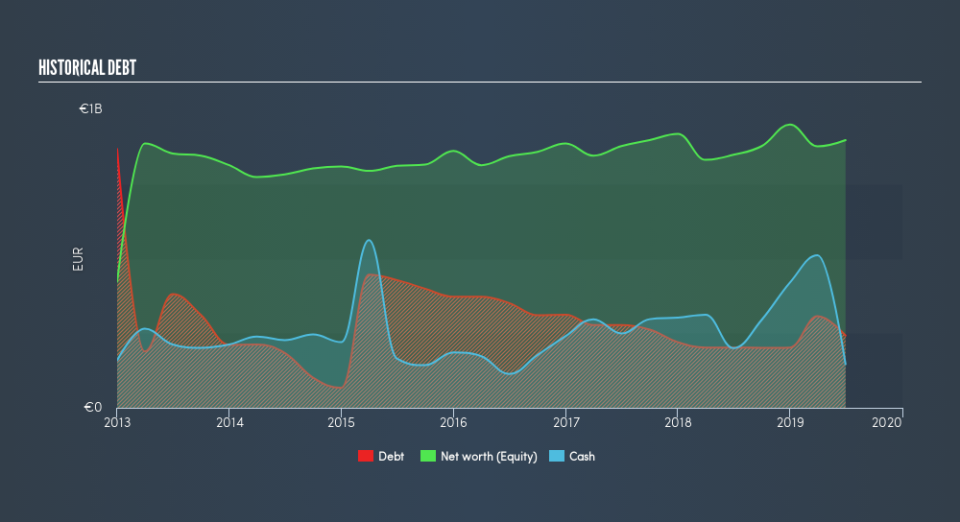

What Is Valmet Oyj's Net Debt?

The image below, which you can click on for greater detail, shows that at June 2019 Valmet Oyj had debt of €242.0m, up from €202.0m in one year. However, it also had €146.0m in cash, and so its net debt is €96.0m.

How Strong Is Valmet Oyj's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Valmet Oyj had liabilities of €1.77b due within 12 months and liabilities of €504.0m due beyond that. Offsetting these obligations, it had cash of €146.0m as well as receivables valued at €958.0m due within 12 months. So its liabilities total €1.17b more than the combination of its cash and short-term receivables.

Valmet Oyj has a market capitalization of €2.63b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Valmet Oyj's net debt is only 0.29 times its EBITDA. And its EBIT easily covers its interest expense, being 88.7 times the size. So we're pretty relaxed about its super-conservative use of debt. In addition to that, we're happy to report that Valmet Oyj has boosted its EBIT by 39%, thus reducing the spectre of future debt repayments. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Valmet Oyj can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, Valmet Oyj recorded free cash flow worth a fulsome 90% of its EBIT, which is stronger than we'd usually expect. That positions it well to pay down debt if desirable to do so.

Our View

The good news is that Valmet Oyj's demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. But, on a more sombre note, we are a little concerned by its level of total liabilities. Zooming out, Valmet Oyj seems to use debt quite reasonably; and that gets the nod from us. After all, sensible leverage can boost returns on equity. Another positive for shareholders is that it pays dividends. So if you like receiving those dividend payments, check Valmet Oyj's dividend history, without delay!

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.