Can Dongyue Group Limited’s (HKG:189) ROE Continue To Surpass The Industry Average?

While some investors are already well versed in financial metrics (hat tip), this article is for those who would like to learn about Return On Equity (ROE) and why it is important. By way of learning-by-doing, we’ll look at ROE to gain a better understanding of Dongyue Group Limited (HKG:189).

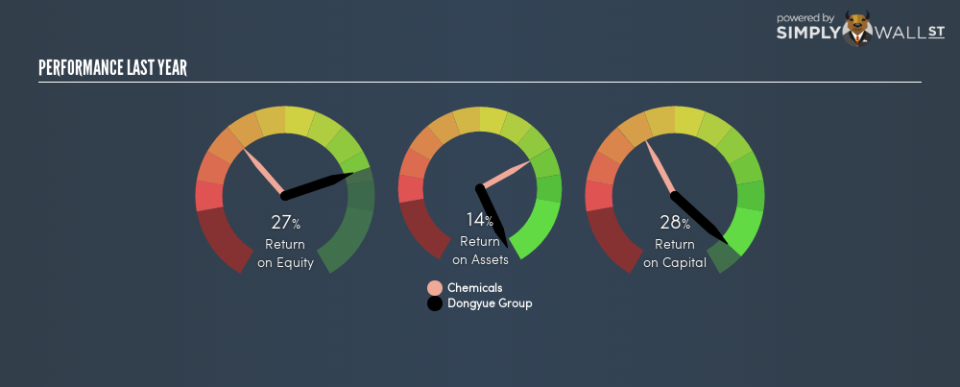

Dongyue Group has a ROE of 27%, based on the last twelve months. One way to conceptualize this, is that for each HK$1 of shareholders’ equity it has, the company made HK$0.27 in profit.

Check out our latest analysis for Dongyue Group

Want to help shape the future of investing tools and platforms? Take the survey and be part of one of the most advanced studies of stock market investors to date.

How Do I Calculate ROE?

The formula for return on equity is:

Return on Equity = Net Profit ÷ Shareholders’ Equity

Or for Dongyue Group:

27% = 2098.267 ÷ CN¥8.4b (Based on the trailing twelve months to June 2018.)

Most know that net profit is the total earnings after all expenses, but the concept of shareholders’ equity is a little more complicated. It is all earnings retained by the company, plus any capital paid in by shareholders. You can calculate shareholders’ equity by subtracting the company’s total liabilities from its total assets.

What Does Return On Equity Mean?

ROE measures a company’s profitability against the profit it retains, and any outside investments. The ‘return’ is the profit over the last twelve months. A higher profit will lead to a higher ROE. So, as a general rule, a high ROE is a good thing. That means it can be interesting to compare the ROE of different companies.

Does Dongyue Group Have A Good ROE?

Arguably the easiest way to assess company’s ROE is to compare it with the average in its industry. However, this method is only useful as a rough check, because companies do differ quite a bit within the same industry classification. Pleasingly, Dongyue Group has a superior ROE than the average (9.4%) company in the Chemicals industry.

That is a good sign. I usually take a closer look when a company has a better ROE than industry peers. For example, I often check if insiders have been buying shares .

Why You Should Consider Debt When Looking At ROE

Most companies need money — from somewhere — to grow their profits. The cash for investment can come from prior year profits (retained earnings), issuing new shares, or borrowing. In the case of the first and second options, the ROE will reflect this use of cash, for growth. In the latter case, the debt used for growth will improve returns, but won’t affect the total equity. Thus the use of debt can improve ROE, albeit along with extra risk in the case of stormy weather, metaphorically speaking.

Combining Dongyue Group’s Debt And Its 27% Return On Equity

Although Dongyue Group does use debt, its debt to equity ratio of 0.26 is still low. When I see a high ROE, fuelled by only modest debt, I suspect the business is high quality. Conservative use of debt to boost returns is usually a good move for shareholders, though it does leave the company more exposed to interest rate rises.

The Bottom Line On ROE

Return on equity is useful for comparing the quality of different businesses. In my book the highest quality companies have high return on equity, despite low debt. If two companies have around the same level of debt to equity, and one has a higher ROE, I’d generally prefer the one with higher ROE.

But ROE is just one piece of a bigger puzzle, since high quality businesses often trade on high multiples of earnings. The rate at which profits are likely to grow, relative to the expectations of profit growth reflected in the current price, must be considered, too. So I think it may be worth checking this free this detailed graph of past earnings, revenue and cash flow .

If you would prefer check out another company — one with potentially superior financials — then do not miss this free list of interesting companies, that have HIGH return on equity and low debt.

To help readers see past the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price-sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned. For errors that warrant correction please contact the editor at editorial-team@simplywallst.com.