Duxton Broadacre Farms (ASX:DBF) Is Making Moderate Use Of Debt

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about. So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Duxton Broadacre Farms Limited (ASX:DBF) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Duxton Broadacre Farms

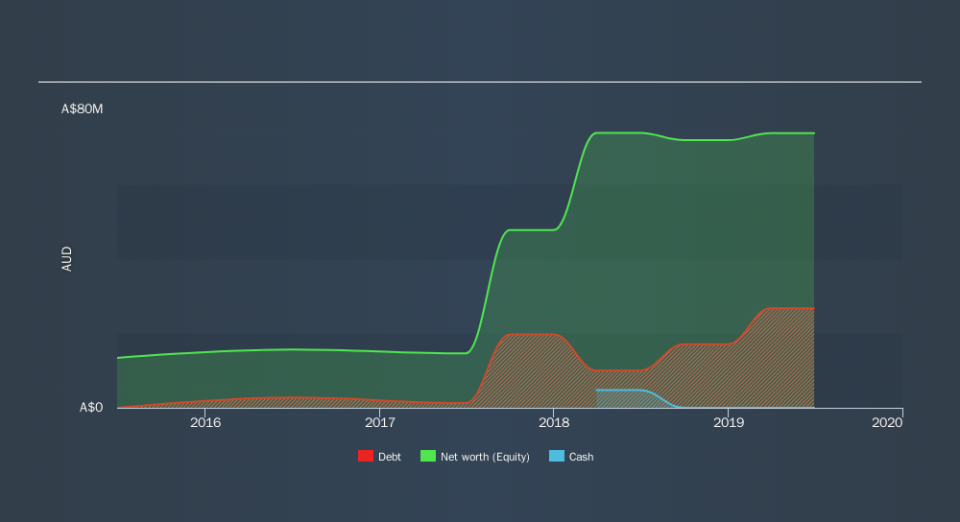

What Is Duxton Broadacre Farms's Net Debt?

As you can see below, at the end of June 2019, Duxton Broadacre Farms had AU$26.7m of debt, up from AU$11.0m a year ago. Click the image for more detail. Net debt is about the same, since the it doesn't have much cash.

A Look At Duxton Broadacre Farms's Liabilities

We can see from the most recent balance sheet that Duxton Broadacre Farms had liabilities of AU$5.22m falling due within a year, and liabilities of AU$27.6m due beyond that. Offsetting these obligations, it had cash of AU$12.0k as well as receivables valued at AU$3.17m due within 12 months. So its liabilities total AU$29.6m more than the combination of its cash and short-term receivables.

This deficit isn't so bad because Duxton Broadacre Farms is worth AU$49.8m, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. When analysing debt levels, the balance sheet is the obvious place to start. But it is Duxton Broadacre Farms's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Duxton Broadacre Farms had negative earnings before interest and tax, and actually shrunk its revenue by 6.4%, to AU$14m. That's not what we would hope to see.

Caveat Emptor

Importantly, Duxton Broadacre Farms had negative earnings before interest and tax (EBIT), over the last year. To be specific the EBIT loss came in at AU$2.1m. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. However, it doesn't help that it burned through AU$23m of cash over the last year. So suffice it to say we consider the stock very risky. When I consider a company to be a bit risky, I think it is responsible to check out whether insiders have been reporting any share sales. Luckily, you can click here ito see our graphic depicting Duxton Broadacre Farms insider transactions.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.