Should Eckoh (LON:ECK) Be Disappointed With Their 26% Profit?

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

The simplest way to invest in stocks is to buy exchange traded funds. But investors can boost returns by picking market-beating companies to own shares in. For example, the Eckoh plc (LON:ECK) share price is up 26% in the last year, clearly besting than the market return of around -1.9% (not including dividends). That's a solid performance by our standards! In contrast, the longer term returns are negative, since the share price is 2.6% lower than it was three years ago.

See our latest analysis for Eckoh

We don't think that Eckoh's modest trailing twelve month profit has the market's full attention at the moment. We think revenue is probably a better guide. As a general rule, we think this kind of company is more comparable to loss-making stocks, since the actual profit is so low. For shareholders to have confidence a company will grow profits significantly, it must grow revenue.

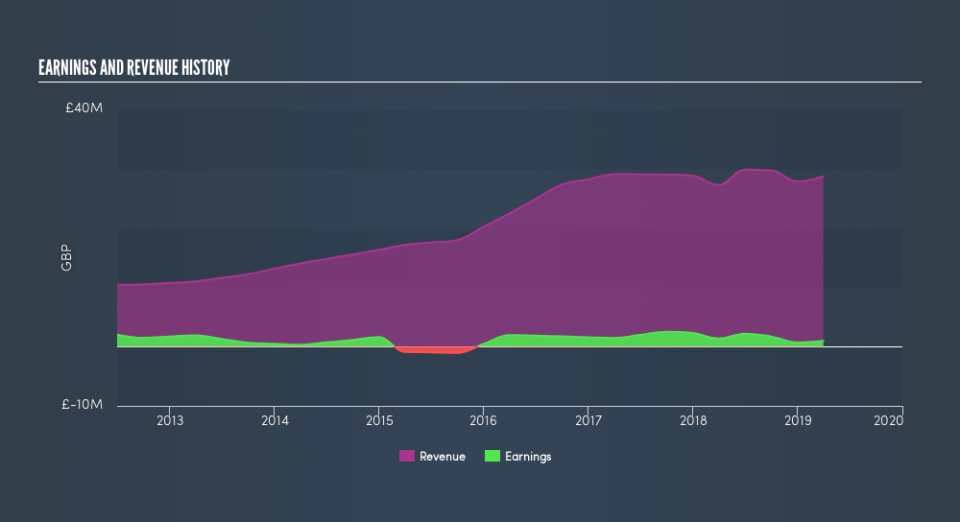

In the last year Eckoh saw its revenue grow by 5.4%. That's not great considering the company is losing money. In keeping with the revenue growth, the share price gained 26% in that time. While not a huge gain tht seems pretty reasonable. It could be worth keeping an eye on this one, especially if growth accelerates.

The graphic below shows how revenue and earnings have changed as management guided the business forward. If you want to see cashflow, you can click on the chart.

This free interactive report on Eckoh's balance sheet strength is a great place to start, if you want to investigate the stock further.

What about the Total Shareholder Return (TSR)?

We'd be remiss not to mention the difference between Eckoh's total shareholder return (TSR) and its share price return. The TSR is a return calculation that accounts for the value of cash dividends (assuming that any dividend received was reinvested) and the calculated value of any discounted capital raisings and spin-offs. Its history of dividend payouts mean that Eckoh's TSR of 28% over the last year is better than the share price return.

A Different Perspective

It's nice to see that Eckoh shareholders have received a total shareholder return of 28% over the last year. That's including the dividend. That's better than the annualised return of 2.3% over half a decade, implying that the company is doing better recently. Someone with an optimistic perspective could view the recent improvement in TSR as indicating that the business itself is getting better with time. Before spending more time on Eckoh it might be wise to click here to see if insiders have been buying or selling shares.

If you are like me, then you will not want to miss this free list of growing companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on GB exchanges.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.