Emerald Expositions Events (NYSE:EEX) Takes On Some Risk With Its Use Of Debt

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk. So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Emerald Expositions Events, Inc. (NYSE:EEX) makes use of debt. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Emerald Expositions Events

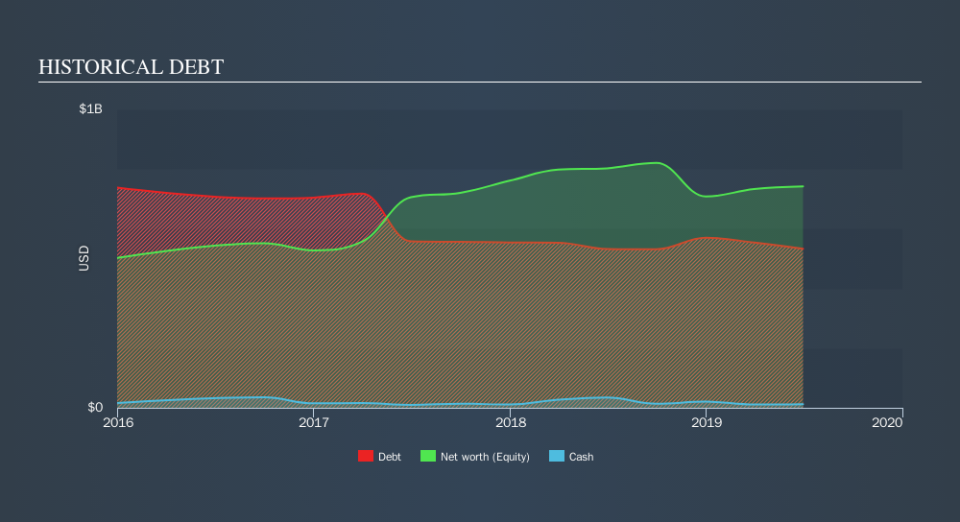

What Is Emerald Expositions Events's Debt?

The chart below, which you can click on for greater detail, shows that Emerald Expositions Events had US$532.7m in debt in June 2019; about the same as the year before. However, it does have US$12.4m in cash offsetting this, leading to net debt of about US$520.3m.

How Healthy Is Emerald Expositions Events's Balance Sheet?

According to the last reported balance sheet, Emerald Expositions Events had liabilities of US$209.4m due within 12 months, and liabilities of US$620.0m due beyond 12 months. On the other hand, it had cash of US$12.4m and US$75.3m worth of receivables due within a year. So it has liabilities totalling US$741.7m more than its cash and near-term receivables, combined.

Given this deficit is actually higher than the company's market capitalization of US$733.5m, we think shareholders really should watch Emerald Expositions Events's debt levels, like a parent watching their child ride a bike for the first time. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Emerald Expositions Events's debt is 3.5 times its EBITDA, and its EBIT cover its interest expense 3.3 times over. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. More concerning, Emerald Expositions Events saw its EBIT drop by 5.9% in the last twelve months. If that earnings trend continues the company will face an uphill battle to pay off its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Emerald Expositions Events's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. Over the last three years, Emerald Expositions Events recorded free cash flow worth a fulsome 84% of its EBIT, which is stronger than we'd usually expect. That puts it in a very strong position to pay down debt.

Our View

Neither Emerald Expositions Events's ability to handle its total liabilities nor its interest cover gave us confidence in its ability to take on more debt. But its conversion of EBIT to free cash flow tells a very different story, and suggests some resilience. When we consider all the factors discussed, it seems to us that Emerald Expositions Events is taking some risks with its use of debt. While that debt can boost returns, we think the company has enough leverage now. Even though Emerald Expositions Events lost money on the bottom line, its positive EBIT suggests the business itself has potential. So you might want to check outhow earnings have been trending over the last few years.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.