With EPS Growth And More, Garden Reach Shipbuilders & Engineers (NSE:GRSE) Is Interesting

Some have more dollars than sense, they say, so even companies that have no revenue, no profit, and a record of falling short, can easily find investors. Unfortunately, high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson.

In contrast to all that, I prefer to spend time on companies like Garden Reach Shipbuilders & Engineers (NSE:GRSE), which has not only revenues, but also profits. Now, I'm not saying that the stock is necessarily undervalued today; but I can't shake an appreciation for the profitability of the business itself. In comparison, loss making companies act like a sponge for capital - but unlike such a sponge they do not always produce something when squeezed.

Check out our latest analysis for Garden Reach Shipbuilders & Engineers

How Fast Is Garden Reach Shipbuilders & Engineers Growing Its Earnings Per Share?

Even modest earnings per share growth (EPS) can create meaningful value, when it is sustained reliably from year to year. So it's no surprise that some investors are more inclined to invest in profitable businesses. Like a falcon taking flight, Garden Reach Shipbuilders & Engineers's EPS soared from ₹7.17 to ₹11.14, over the last year. That's a impressive gain of 55%.

I like to see top-line growth as an indication that growth is sustainable, and I look for a high earnings before interest and taxation (EBIT) margin to point to a competitive moat (though some companies with low margins also have moats). Garden Reach Shipbuilders & Engineers shareholders can take confidence from the fact that EBIT margins are up from -2.8% to 1.8%, and revenue is growing. Ticking those two boxes is a good sign of growth, in my book.

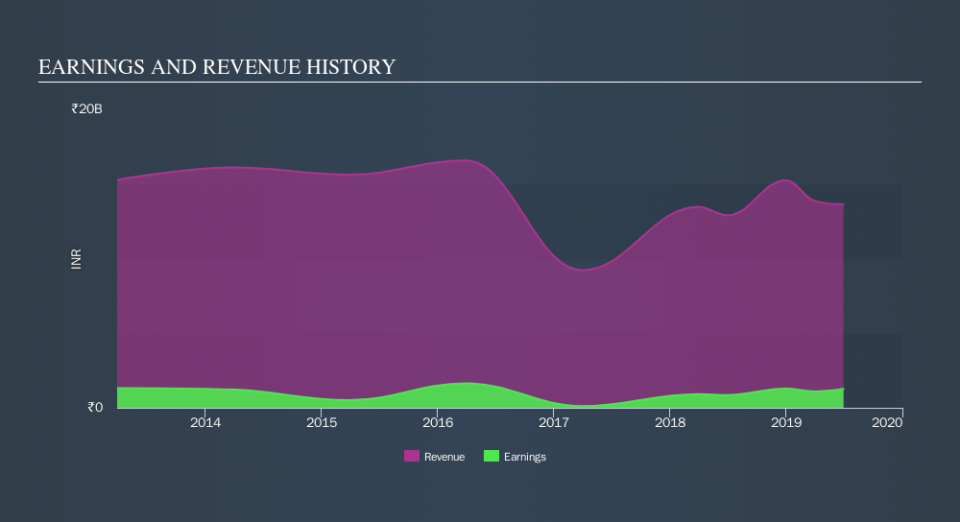

You can take a look at the company's revenue and earnings growth trend, in the chart below. Click on the chart to see the exact numbers.

Since Garden Reach Shipbuilders & Engineers is no giant, with a market capitalization of ₹20b, so you should definitely check its cash and debt before getting too excited about its prospects.

Are Garden Reach Shipbuilders & Engineers Insiders Aligned With All Shareholders?

As a general rule, I think it worth considering how much the CEO is paid, since unreasonably high rates could be considered against the interests of shareholders. For companies with market capitalizations between ₹7.1b and ₹28b, like Garden Reach Shipbuilders & Engineers, the median CEO pay is around ₹20m.

The Garden Reach Shipbuilders & Engineers CEO received total compensation of just ₹5.0m in the year to March 2019. That looks like modest pay to me, and may hint at a certain respect for the interests of shareholders. While the level of CEO compensation isn't a huge factor in my view of the company, modest remuneration is a positive, because it suggests that the board keeps shareholder interests in mind. It can also be a sign of a culture of integrity, in a broader sense.

Is Garden Reach Shipbuilders & Engineers Worth Keeping An Eye On?

Given my belief that share price follows earnings per share you can easily imagine how I feel about Garden Reach Shipbuilders & Engineers's strong EPS growth. With swiftly growing earnings, it probably has its best days ahead, and the modest CEO pay suggests the company is careful with cash. So I'd argue this is the kind of stock worth watching, even if it isn't great value today. Now, you could try to make up your mind on Garden Reach Shipbuilders & Engineers by focusing on just these factors, or you could also consider how its price-to-earnings ratio compares to other companies in its industry.

Of course, you can do well (sometimes) buying stocks that are not growing earnings and do not have insiders buying shares. But as a growth investor I always like to check out companies that do have those features. You can access a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.