Flood-prone homeowners could see major rate hikes in FEMA flood insurance changes, new study finds

With a major overhaul of the nation’s flood insurance program just months away, new data released Monday by the First Street Foundation suggests hundreds of thousands of homeowners in the riskiest locations across America could face massive rate hikes starting in October.

The Brooklyn, New York-based research group estimates the average rate needs to more than quadruple on the nation’s most flood-prone homes under the ongoing effort to make the federal flood insurance program solvent and ensure homeowners most at risk are paying their fair share.

First Street data projects that the majority of homeowners won't see big rate changes, and others could see premiums decrease. But for some 265,000 properties, annual premiums would need to climb $10,000 or more to match the actual risk. Those with more expensive properties are estimated to see the biggest premium increases.

Any actual rate hikes adopted by the federal government would be slowly phased in for existing policyholders.

First Street’s calculations, which the group says are based on similar methodology to what the National Flood Insurance Program will use when it rolls out its new rating system on Oct. 1, reveal a major shift is needed in pricing policies. Such changes could level the playing field overall but depress home values in some areas.

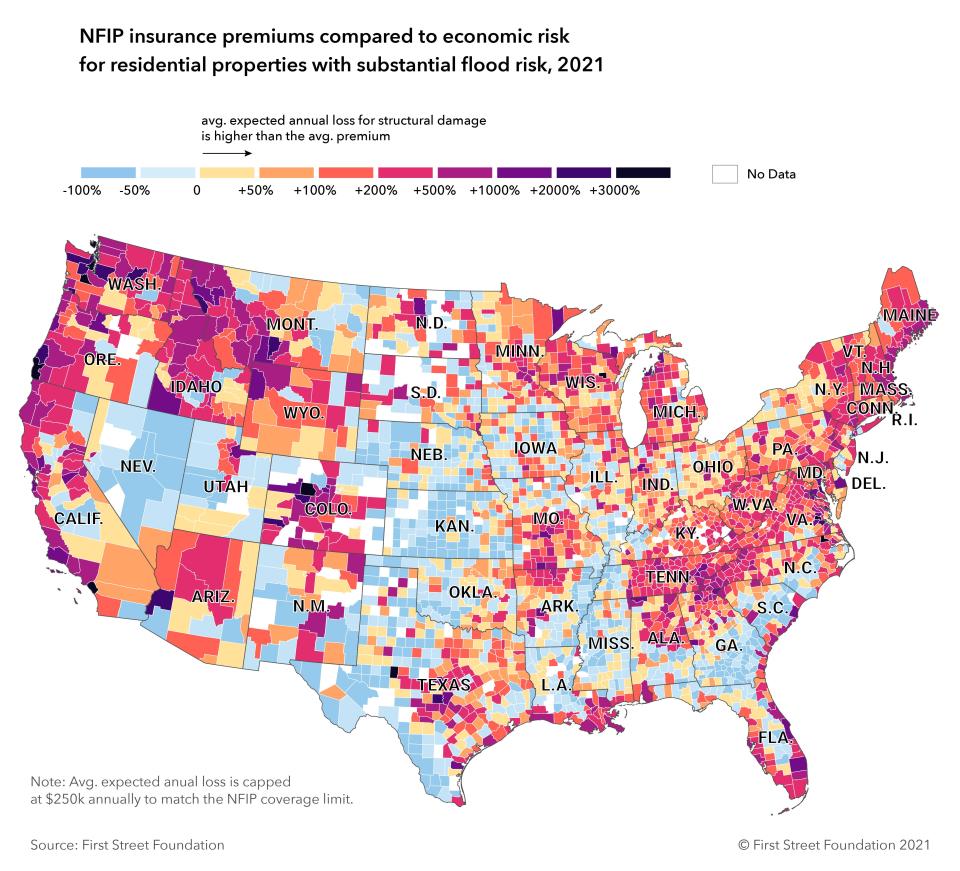

Some of the biggest gaps in current premiums versus actual risk appear in the Southeast and Mid-Atlantic regions in places such as Florida, South Carolina and New Jersey. Chasms also exist in pockets of California, Texas and Washington.

In the historic waterfront city of Charleston, South Carolina, for example, nearly four in 10 flood-prone homes would need to pay an average premium of $18,211 to cover the anticipated costs of flooding compared to the current average NFIP rate of $2,264, First Street data shows.

And almost every homeowner on the barrier island city of South Patrick Shores, Florida, would need to pay an average of $24,724 a year to adequately cover their risk. The average rate there now is $491, First Street data shows.

The Federal Emergency Management Agency, which operates the National Flood Insurance Program, has not publicly shared how its new "Risk Rating 2.0" overhaul will impact individual premiums. So it’s unknown how close First Street’s calculations will come to the real thing.

But FEMA said First Street's estimates are just that – estimates.

"Any entity claiming that they can provide insight or comparison to the Risk Rating 2.0 initiative, including premium amounts, is misinformed and setting public expectations that are not based in fact," said David Maurstad, senior executive for the National Flood Insurance Program. "While entities are free to suggest or estimate their opinion of what flood insurance premiums should be, they are offering exactly that – an opinion – and they do not have insight into the Risk Rating 2.0 initiative."

First Street agreed its numbers are estimates but said its modeling is comparable to any of the risk-based approaches that FEMA would use.

“Our data supports the idea that if insurance pricing is adjusted to match the risk from today's current and future climates, there will need to be significant adjustments," the group said in a statement.

How financial toll of flood damage is calculated

First Street calculated the property-level financial toll of flood damage by collecting home values and structural information for every single-family and small multi-unit dwelling in the nation and applying it to its previously published flood model with damage formulas.

With that information, the foundation compared current flood insurance premiums to what it says the federal government would have to charge to cover the expected damages each home could incur because of flooding.

Its data release marks the first time individual homeowners across the country will be able to see the estimated risk they face from flooding and what that risk translates to in terms of average annual financial loss – which will dictate potential insurance costs. The group allows property owners to look up that information on its website.

Increased NFIP premiums are a reckoning long overdue, said Carolyn Kousky, executive director of the University of Pennsylvania’s Wharton Risk Center and a First Street advisory board member.

Kousky said inaccurate pricing has left the NFIP in the red. Its coffers were wiped out by Hurricane Katrina in 2005. The program suffered additional hits from hurricanes Sandy, Harvey and Irma. Congress bailed out the program in 2017 with $16 billion in debt relief, leaving the ultimate cost of those storms on the backs of the American taxpayer.

Flood insurance premiums also will need to keep climbing over the next few decades, First Street said, as rising sea levels, climate change and rapid development in coastal regions exacerbate flood risks.

“Environmental change has already been happening for 50 years, and the policy structure hasn’t kept up with it,” said Matthew Eby, First Street’s founder and executive director. “FEMA is trying to compensate for five decades of mispriced insurance."

FEMA has for years been working on a new risk assessment and rating structure. When it’s implemented in October, Risk Rating 2.0 will be the biggest change to the NFIP since its inception more than 50 years ago.

For the first time, it will tie individual premiums to each property’s actual flood risk. It also will level the playing field so that properties with the highest risks and the biggest associated damages pay the most.

Currently, the program bases rates on the amount of insurance purchased for a home rather than its replacement cost. So the owner of a $2.5 million house with the same flood risks as the owner of a $250,000 house might pay the same rate even though repairs to the mansion would cost more.

“Over time, this has inadvertently caused a disparity – policyholders with lower-valued homes are paying more for their insurance coverage than they should while policyholders with higher-valued homes are paying less," Maurstad said. "There is also a disparity at the edge of flood map zones where neighboring property owners often have vastly different flood insurance costs for the relatively same level of risk."

FEMA said rate reductions would take effect immediately upon Risk Rating 2.0’s implementation. Rate hikes would be phased in slowly – a maximum 18% increase per year – for existing policyholders. Those buying insurance after Oct. 1 would pay the full amount.

Facing the biggest average rate hike are an estimated 4.26 million homes with a substantial risk of flooding that could cause structural damage. Substantial risk is defined as having a 1% annual chance of flood, otherwise known as a 100-year flood risk.

A third of those properties are in flood zones and required to buy flood insurance if they have a federally backed mortgage. If all of them got a policy, the average premium would need to rise from the current $1,884 a year to nearly $7,895 to cover the risk, First Street Foundation data shows.

The other two-thirds of those properties are outside the flood zone but still face a substantial risk of flooding resulting in structural damage. If all of those homeowners got a policy, the average rate would need to rise from $478 a year to roughly $2,484 to cover their risk.

No one ever wants to pay more for insurance, said Dawn Maletzke, who lives in South Patrick Shores, a community tucked between the Atlantic Ocean and the Banana River Lagoon. “I wouldn’t be happy about it, but if we don’t have a choice, we’ll pay it.”

Maletzke and her husband started buying flood insurance after several hurricanes swept through the area and forced evacuations, but she feels like at less than $400 a year, “it isn’t super expensive.” Even if their insurance doubled or tripled, she said, “it wouldn’t be a huge hardship.”

She doubts it would be an issue for anyone who buys a home in her neighborhood either, because there’s such a demand for homes on the barrier islands along Florida’s east coast.

“People want to live here, and people who do aren’t worried about those things," she said. "They’ll pay the cost to live here. It’s a lifestyle.”

Conversely, more than one in four counties across the U.S. would see lower rates, according to First Street’s model. They include dozens of counties in central South Carolina, the inland portions of southeast Georgia and the Florida panhandle.

Many of the mostly rural counties along the Mississippi River from Missouri’s boot heel south to the Delta could also see lower premium prices.

For example, owners of some of the most at-risk residential properties in East Baton Rouge Parish, Louisiana, could see rates more in line with the $326 average annual loss First Street calculated for their homes. That's compared to the current average NFIP premium of $814 per year.

Caveats and Congress

In preparation for its expected rollout, FEMA is sharing details of the program with the insurance industry to get feedback, said Joe Rossi, a flood specialist for Rogers Gray Insurance, executive director of the Massachusetts Coastal Coalition and chairman of the National Flood Association’s flood committee.

Rossi has seen the program and the rate structure, but like others in the industry, he is under a non-disclosure agreement regarding the details and rates.

“I personally think Risk Rating 2.0 is a real positive change,” Rossi said. “I say we’re in uncharted territory because this is the first time in 52 years that the NFIP has made this big of a change.”

Rossi is among those who will get a full update on Risk Rating 2.0 on March 3.

First Street and independent experts interviewed by USA TODAY say there are caveats to the group’s study. All modeling is subject to error, and First Street doesn’t directly predict premium increases. It instead assesses how much money is needed annually to pay for estimated damages over the course of a 30-year mortgage. This is consistent with how FEMA says it will calculate its new rates.

NFIP premiums also may be higher after adding in fees or operating costs. Or, they may be lower if a homeowner increases their deductible or obtains discounts for flood protection measures. FEMA caps payouts for structural damage at $250,000 regardless of a home's value.

Those watching FEMA also say a lot can change between now and October.

Rossi said he has heard the rollout could be delayed, or that some of the parameters might be adjusted “so the industry can kind of grapple a little bit more with the change.”

Congress could still take action that affects the rollout.

“FEMA said it’s a programmatic change and they’re allowed to do it, but if we get a reform bill passed in June and that dictates something different, then there could be a delay," he said. "Congress may come out and say the maximum amount of increase in a year, which right now is 18%, is 10%, so that changes the dynamic as well.”

What the new model does

The National Flood Insurance Program, implemented in 1968, provides about 95% of the nation's flood insurance policies – some 5.1 million.

The rating structure hasn’t changed since the 1970s. It assesses premiums based on whether properties are in a flood zone, the occupancy type and the structure’s elevation. It also takes into account just two types of flood risks: those from rising rivers or coastal storm surge.

That system fails to accurately assess the real risk of flooding and the associated damages, experts say. As a result, the NFIP collects only about $4.6 billion in annual revenue – 80% from premiums; the rest from fees and surcharges – even though it provides more than $1.3 trillion in coverage.

The 2.0 model aims to bring the program more in line with actual risks by calculating premiums based on each home’s specific structural features and its replacement value. It also will include a broader range of flooding events, such as heavy rainfall, tsunamis and coastal erosion.

FEMA’s existing flood zones will not factor into rate calculations, so properties outside the zones won't automatically pay lower premiums. Homeowners inside those zones will still be required to buy flood insurance if they have federally backed mortgages.

SUBSCRIBE: Help support quality journalism like this.

First Street estimates the flood zones include about 3.8 million single-family and two- to four-unit residential structures. The majority face no significant flood risk and should see flat or even declining premiums.

About 1.5 million of those homes, however, carry substantial flood risk that could cause structural damage. First Street data shows their premiums should rise an average of 4.2 times to cover current risk.

An additional 2.7 million residential properties outside the flood zones are at risk of flood-induced structural damage. Their rates should climb 5.2 times, First Street estimates.

Faced with such soaring prices, some experts predict homeowners could drop their flood coverage, leaving themselves vulnerable to potentially catastrophic flooding with no insurance to protect them.

Florida in the crosshairs

No state faces greater ramifications than Florida, First Street data shows.

About 900,000 properties in the state are at risk of structural damage from floods, which would require $7.5 billion to adequately insure. That’s nearly 40% of the nation’s total $18.8 billion in risk, according to First Street data.

Broward County, home to Fort Lauderdale on the Atlantic coast north of Miami, faces more than $1.2 billion in risk, the highest of any county in the country. At-risk properties there should average at least $12,000 a year in premiums, First Street data shows, a ten-fold increase over current estimated rates.

Florida’s Pinellas, Miami-Dade, Charlotte, Lee, Brevard and Sarasota counties also appear in the top 10 nationally for the total value of real estate at risk.

Experts say huge premium increases could deflate home values in some communities. Homebuyers might pass on a property if they’re required to purchase a flood insurance policy that costs tens of thousands of dollars annually.

It’s a difficult pill to swallow but an unfortunate reality, experts say.

“You’re going to have some people having a harder time selling their home, but some people will have a much better time,” said Elliott Hagood, a real estate broker who sells homes in a two-county area on the east Central Florida coast.

Hurricane storm surge has flooded many of the area’s homes, including one that Hagood had under contract in Daytona Beach. The owner dried it out and the sale went through as planned, he said.

“If you have a multimillion-dollar home that tends to flood more often than not,” Hagood said, “then maybe it’s a good thing that you pay a higher premium, which would either force you to build up to the new code and everyone else doesn’t have to keep paying to rebuild your million dollar house.”

So far in his region, flooding has had only minor impacts on the market, said Hagood, who recently served on a municipal panel looking at flood map issues. “A house on the river, whether it has been flooded or not, is still a house on the river.”

But as climate change brings sea level rise, record storm surges and increased rainfall, it could become too expensive to keep rebuilding and repairing.

“There’s a focus on premiums, as if they’re somehow divorced from the underlying risk,” Kousky said. “The question should be, how do we reduce this risk? Are these areas where we should have development?”

Low-income areas could suffer

While high-end property owners might face the greatest rate hikes, even a modest increase could prove difficult for lower-income communities.

And unlike coastal areas where developers chose to build in floodplains, some communities are at risk due to political decisions outside their control, said Eric Tate, a University of Iowa professor who researches inequities in flooding. He cited flood-prone neighborhoods in central Houston as an example.

“Many neighborhoods weren’t originally in a floodplain, but development at the upper ends of the basin added impervious cover,” Tate said. “It’s not really having anything to do with the choices they made. … The floodplain grew into them.”

USA TODAY’s review of First Street data found some places with low home values, including those along the Appalachian river valleys, facing potentially large premium increases.

Dauphin County, seat of Pennsylvania’s capital along the Susquehanna River, tops the list. Its median household income is about $10,000 less than the national average. A third of its population is nonwhite.

First Street data shows that one in 10 of the homes there faces flood risks that would cost, on average, $5,364 in annual premiums to cover the costs. That’s 709% higher than current NFIP rates for those properties.

Three hours to the southwest in Monongalia County, West Virginia, more than a fifth of households fall below the federal poverty level. The most severe flood-prone homes there would have to pay premiums 527% higher than today to cover the risk, First Street data shows.

In Louisiana, a series of parishes surrounding New Orleans, Lake Pontchartrain and bayous to the south could see a doubling of premiums. That could be particularly troubling for New Orleans, where a quarter of households are below the poverty line.

FEMA itself “does not currently have the authority to implement an affordability program, nor does FEMA’s current rate structure provide the funding required to support an affordability program,” according to a recent Congressional Research Service report about Risk Rating 2.0. But in 2018, the agency provided Congress an analysis of the places most impacted by insurance costs and offered options for an affordability program.

SUBSCRIBE: Help support quality journalism like this.

Congress could take up the issue when it considers bills reauthorizing the flood insurance program.

Kousky, with the Wharton Risk Center, said she thinks Congress should create a means-based test to couple with premium increases. But she hopes those discussions don’t delay or derail implementation of Risk Rating 2.0.

Doing so would be “a terrible idea,” she said. Without appropriately priced insurance and a discussion about how to reduce the risks, she and other experts said, people will keep building where they shouldn’t, and taxpayers will continue bailing them out.

The problem will worsen as a changing climate and rising sea levels bring greater flood risks.

“It’s going to be hurting communities,” Kousky said. “And so we need to start having that national conversation: How do we grapple with this risk that we’re facing as a country and develop some policy solutions to really help people transition in the face of this growing risk?

“Even if you delay Risk Rating 2.0, you’re not delaying the increasing risk,” she said. “You’re just putting your head in the sand and trying to ignore it.”

This article originally appeared on USA TODAY: FEMA flood insurance rates could spike for some, new study shows