Florida’s biggest insurer wants 14% rate hike, warns of ‘hurricane tax’ if big storm hits

Millions of Florida homeowners could see their already skyrocketing insurance costs soar even higher.

The board overseeing Citizens, the state-run company that is Florida’s largest home insurer, voted Wednesday to seek a 14 percent rate increase. And the insurer also warns that it could need to impose what industry experts call a “hurricane tax” this year — a yet-to-be-determined fee imposed on all property insurance holders in the state.

All it would take to trigger the fee is another big expensive storm, or even a series of small ones, according to a new report from Citizens, which has increasingly become the only option for residents dumped by private insurers that have gone bankrupt or decided to shed high-risk properties.

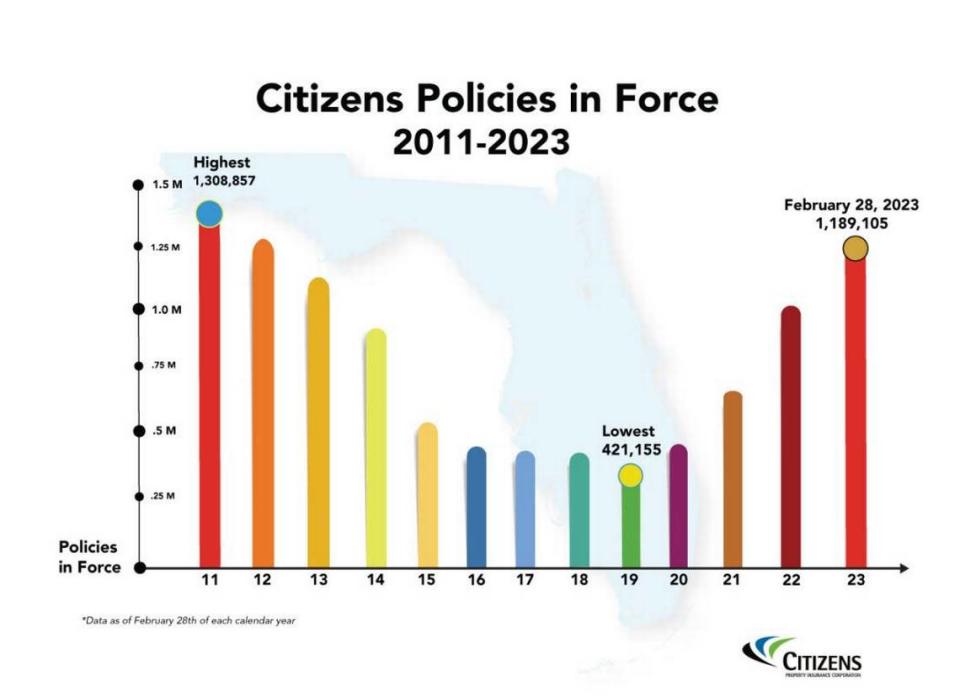

The reasons for the moves: Hurricane Ian put a multibillion-dollar dent in Citizens’ reserves at the same time hundreds of thousands of Floridians have flocked to the insurer of last resort, spurring record growth in policies. Citizens now insures 1.2 million owners — a 50 percent spike in a single year — with many of those homes in vulnerable coastal areas.

The latest fiscal report warned that Hurricane Ian “significantly depleted” Citizens’ financial resources, leaving the company with only $4.9 billion in surplus. That’s nearly $2 billion less than it had banked for the last two hurricane seasons.

“Currently, Citizens is projected to have a considerable portion of its surplus exposed in the 2023 storm season and has the potential for significant assessments for a 1‐100 year event or after multiple smaller events,” the report read.

Got hurricane insurance from Citizens? Here’s a new reason your bill may rise in Florida

Even Gov. Ron DeSantis has expressed concerns over the financial status of the largest home insurance firm in Florida.

“As most people know, Citizens has not been solvent,” he said at a news conference in Fort Myers earlier this month. “If you did have a major, major hurricane hit with a lot of Citizens property holders, it would not have enough to pay out.”

On Wednesday, Citizens’ board of governors approved a 14% rate request, which the state still must approve. It’s the highest rate increase the company has asked for since 2009, when the state capped rate increases at 10%. It’s not guaranteed that Citizens will be allowed to raise rates that high. Last year, Citizens asked the state for an 11% increase but was only approved for 6.4%.

President Tim Cerio said the rate hike was part of the insurer’s mission this year to push policies into the private market.

“The larger we grow, the greater our exposure, and the greater our exposure, the greater our risk to the taxpayers of an assessment,” he said. “We’re going to work hard to depopulate and truly return to being the state’s residual insurer, or insurer of last resort.”

How do we get to a hurricane tax?

Citizens has been warning of the risk of statewide hurricane taxes for years, especially as the number of policies has ballooned. But this latest report is the first in recent years to show that that risk exists for even a relatively small storm, known in the industry as a 50-year storm, or a hurricane that has a 1 in 50% chance of happening in a given year.

Previous reports showed it would take a far stronger storm, like a 1-in-100 or 1-in-250, to trigger any sort of assessment.

This report shows that if a 1-in-50-year storm were to occur this hurricane season, Citizens could face a $1.5 billion budget shortfall after it burns through all its options, including that estimated $4.9 billion cash surplus, insurance it purchased from other companies and a statewide hurricane fund.

Homeowners insurance in Florida is a precarious mess that was years in the making

A 1-in-100-year storm could cause an estimated $2.8 billion shortfall, and a 1-in-250-year storm could leave Citizens $13.8 billion in the red.

Shahid Hamid, chair of Florida International University’s Department of Finance, said Citizens is “quite resilient” financially, but it’s clear that an expensive storm could tip the scales into assessment territory.

“It all depends upon whether we get a major hurricane this year. If we don’t get one, we’re OK. If we get one, especially multiple, it will happen,” he said.

If that happens, Citizens has three options. Its first resort is to raise rates on its own policyholders to make up the difference, potentially as much as 30%. If that doesn’t do it, Citizens can levy an up to 2% fee on every home insurance policy in the state, even those with private companies.

The final, and most drastic, option is a tax on nearly every insurance policy in the state of Florida, including renters, boat and auto insurance. In the industry, it’s been dubbed a “hurricane tax,” and it’s what makes certain Citizens can never go bankrupt like other insurance companies.

High costs force some homeowners to choose: Drop insurance, sell or leave Florida

The last time Floridians faced it was after the infamous 2004 and 2005 hurricane seasons when home insurance policies statewide were saddled with a 1% charge on their insurance policies for eight years to cover Citizens’ losses. So, for a $5,000 policy, that would add $50 a year.

While the risk of a hurricane happening in any given year remains steady, Hamid said, the sheer dollar value of properties at risk has leaped up over the past decade. Also, the number of people in risky coastal areas is rising, and the increase in fraudulent lawsuits over the last few years has driven litigation costs higher for Citizens and other insurers.

“The financial risk has gone up,” Hamid said.

Growing numbers of policyholders

A big, expensive hurricane would be a blow to the state-backed insurer, and that risk only grows as the number of policies swells. Multiple insurance companies have gone bankrupt or cut back on their policies in risky coastal spots in the last few years, sending hundreds of thousands of Floridians to the far-cheaper Citizens.

Currently, there are 1.2 million policyholders with Citizens, compared to 800,000 one year ago or 550,000 two years back. The company estimates it could have 1.5 million policies by the end of the year, surpassing its record high in 2011 of 1.3 million.

In Citizens’ ideal world, that number would hover around 450,000, Cerio has said.

Recent efforts to kick people off the Citizens rolls include requiring mandatory flood insurance (even for condo dwellers or people outside of flood zones) and requiring policyholders to get a quote from a private wind insurer before they’re allowed to renew. If that quote is within 20% of the price they pay Citizens, they’re required to take it.

Another tweak now allows Citizens to hike premiums on vacation and investment homes up to 50% every year, while primary homes are capped at a 12% raise.

These jumps in premium prices are supposed to help Citizens catch up with the rest of the private insurance market, which charges far higher prices. An analysis last year found that Citizens charges an average of 44% less than some of the biggest companies in the market.

“Citizens’ rates are artificially low. That throws off the private market and distorts competition,” Cerio said. “That’s unfair.”