What Georgia residents need to know about flood insurance prices and why they need it

For the average homeowner, few activities sound more tedious than spending an afternoon reviewing insurance policies.

Deciding what kind of risks your home has and how much you're willing to dish out on a possible incident is a growing concern for many Georgians as storms and flooding become more frequent.

Rising tides, rising risks

Storms are becoming stronger than they once were, and scientists note they are slowing down, causing storms to dump more water on concentrated areas and worsening floods.

Coupled with other climate change related threats like sea-level rise in coastal communities and development, which can pave over soils that help absorb flood water, insurance agencies are forecasting more flooding, and more risk for their customers and businesses.

Savannah's storm history: A look back at a century of (mostly) near misses from hurricanes

Big storms brewing: '500-year hurricanes?' Give or take 490 years, as Ian showed in ravaging Florida

Storms in Georgia:

Savannah’s storm history: A look back at a century of (mostly) near misses from hurricanes

'500-year hurricanes?' Give or take 490 years, as Ian showed in ravaging Florida

The Federal Emergency Management Agency is already reconsidering how it manages flood risk given the future's forecast. The agency operates the National Flood Insurance Program, where most homeowners get their flood insurance via a network of more than 50 insurance companies and NFIP Direct. The program reevaluated how it prices insurance policies to plan for future floods and last year rolled out Risk Rating 2.0.

While the old FEMA analysis considered a home's elevation, Risk Rating 2.0 takes a wider scope, taking into account historical flood frequency, the type of flood — river, rainfall, coastal flooding — as well as a home's distance to water sources and the cost to rebuild.

Georgians may already have seen the shift in their flood insurance policies. According to FEMA, 24.3% of NFIP policies in Georgia had their premium prices decrease in the first year of the new risk rating system.

Counting the costs

According to the experts, insurance — and its prices — all boil down to risk.

Rob Hoyt is chair of the Risk Management and Insurance Department at the University of Georgia. He said that storm severity and flooding is a major consideration for insurers now more than ever and it is going to hit Georgians in the pocketbook.

More on insurance: UGA engineers launch new project to insure salt marshes for their environmental benefits

Flooding on Georgia's coast: Tropical Storm Ian: Georgia's seasonal high tides will cause flooding as storm comes ashore

"One thing that's important to understand is that we've seen multiple years of increasing catastrophe, losses that have impacted the insurance industry, and certainly the people that are exposed to those events," Hoyt said.

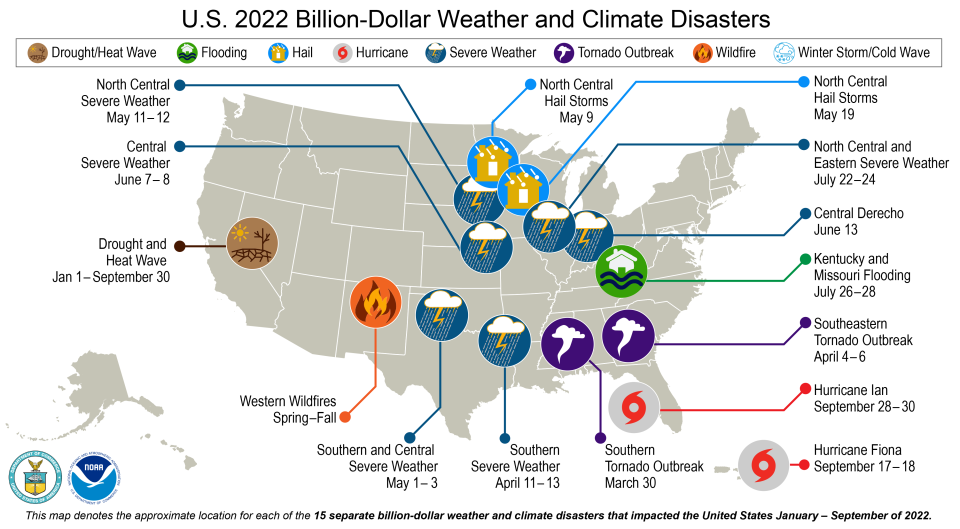

According to the National Oceanic and Atmospheric Administration, nationwide in 2022 there have already been $15 billion disasters. The consequence of that is an insurance industry rethinking how risky weather events really are for homeowners.

When companies insure a home, Hoyt said they are assuming financial risk that in the event of a flood, they'll be paying out funds, meaning companies are expecting to pay out more money as the number of flood incidents increases.

Some Georgia homeowners might not realize that flooding isn't covered by regular home insurance, Hoyt said, and that it is an extra purchase to be budgeted for.

Hoyt said another important part of the price-equation is reinsurance, where companies themselves are buying insurance and transferring part of the risks that they have by writing insurance policies to other companies. Reinsurance is good in that it distributes and diversifies risk, making insurance companies less likely to fold. But it will make insurance more costly for Georgians in the long run.

Prices on the rise

In the past, FEMA subsidized flood insurance, said Tom McDonald, city of Savannah floodplain manager. For coastal residents and those in special flood hazard areas, McDonald said flood insurance rates were relatively low and didn't dissuade people from building in some high-risk areas.

"The Flood Insurance Program through the years ... it's just constantly in a hole because of all these disasters," McDonald said.

With the adjusted Risk Rating 2.0, he said the agency will move from subsidized insurance to actual rates with prices climbing 18% per year until Georgians hit the actual rate.

With those hiking prices, McDonald does share concern that some homeowners will drop their flood insurance. The most expensive policies will be where people are most vulnerable, and it only takes one strong hit for those properties to experience catastrophic damage.

If a homeowner has a federally backed mortgage and is in a high risk flood area, then flood insurance is also required as part of that loan. Private lenders can also stipulate flood insurance.

When buying a house, McDonald said it's important to look into whether the structure has flooded in the past and to call up the city floodplain manager's office to learn more about risks. Before buying any insurance, homeowners should consult with their insurance agent or company to learn more.

For homeowners struggling with repeated flooding, McDonald said the city has some options, including FEMA grants. He said the city will evaluate the house and present an offer to buy out homeowners looking to leave repeatedly flooding properties. This only happens when FEMA grants are available, and homes are prioritized based on the severity of each case.

Worth the investment

While it may seem obvious, McDonald said flooding is expensive, and far more expensive than miscalculating the need for flood insurance. For each flood event in a house, he said NFIP could be paying up to $40,000, a cost that taxpayers are footing. But homeowners shouldn't expect insurance to resolve all the financial fallout from a flood.

"FEMA is not gonna get you out of this," McDonald said. "FEMA might come in, give you a low-interest loan to repair your building, but now you got your mortgage and a low-interest loan."

Marisa Mecke is an environmental journalist. She can be reached at mmecke@gannett.com or by phone at (912) 328-4411.

This article originally appeared on Savannah Morning News: Georgia flood insurance prices may rise due to climate change