Goldman Sachs Picks 2 Stocks to Buy (and 1 to Sell)

If anyone thought last week’s three days of positive trading indicated a trend reversal, or even more implausibly, an end to the recently launched bear market, they were rudely awakened on Friday. Markets tumbled as the US overtook previous pandemic hotspots China and Italy with the unwanted statistic of having the highest number of coronavirus infections on record.

It appears, then, that the new bear market will be around for a while, along with the accompanying bouts of volatility. How long will it last? Impossible to tell, but the new reality means estimates and forecasts have been getting readjusted all over the Street, and investment firm Goldman Sachs has joined the fray.

With COVID-19 restructuring the market, 5-star analyst from the firm, Heather Bellini, has been analyzing the tech names under the firm’s coverage and has reached new conclusions for a number of them. We ran three through TipRanks’ database to determine the rest of the Street’s sentiment. We found out that despite some reservations at Goldman Sachs towards one specific company, all are Buy-rated, with potential for at least 40% upside in the year ahead. Here are the details.

Workday Inc (WDAY)

Let’s start off with Workday, a large-cap software company. With a focus on the HCM (human capital management) market, the Pleasanton, California-based company offers cloud-based finance, HR, and planning system solutions mostly for medium and large sized enterprises.

Despite surging in last week’s market renaissance, WDAY stock is down by 17% year-to-date. In fact, take another step back and the share price has retreated by 39% since notching an all-time high last July.

So, what’s the problem?

There is no problem, says Bellini. The 5-star analyst adds Workday to a list that meets all her current investing criteria. Bellini argues that in the current “challenged IT spending environment”, the company is well set up. As budgets get slashed, Workday’s potent combination of recurring subscription revenue, which amounted to 85% in FY20, and low churn with a 95% gross retention rate, makes it resilient in such times. Also playing into her bullish thesis, Bellini notes Workday’s expanding product portfolio could achieve further penetration with its “planning and analytics” add ons.

The analyst said, “We continue to favor market leaders with a higher mix of recurring revenues and secular tailwinds from digital transformation initiatives and rising cloud adoption. To that end, while we do not think Workday will be insulated from COVID-19 and any corresponding impact to overall IT spend, we believe the company remains well positioned in its core HCM market where win rates remain high and well positioned to capitalize from growing cloud adoption within financials which continues to grow as a percentage of the overall mix.”

Bellini reiterates a Buy rating on WDAY, but the price target is slashed from $223 to $158 on account of “contraction in peer multiples and increased macroeconomic risk.” Expect returns in the shape of 16%, should Bellini’s forecast play out in the coming months. (To watch Bellini’s track record, click here)

Looking at the consensus breakdown, 13 Buys, 6 Holds and 1 Sell coalesce into a Moderate Buy consensus rating. The average price target is $200.25 and indicates potential upside of 47%. (See Workday stock analysis on TipRanks)

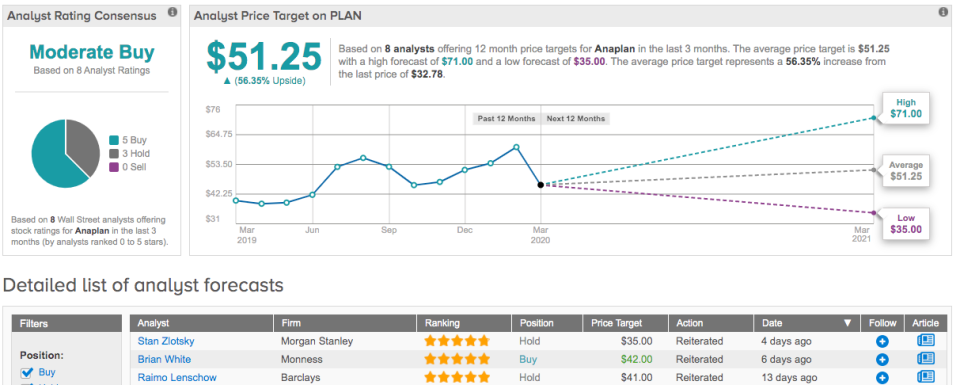

Anaplan Inc (PLAN)

Staying in cloud services, we move on to Anaplan. The company operates in a similar niche to Workday, helping companies streamline operations and make better business decisions through its “connected planning” offerings. With a market cap of $4.4 billion, the mid-cap is significantly smaller than WDAY, and has also taken a heavier beating in the pandemic-stricken climate. PLAN stock is down by a massive 38% year-to-date.

It is worth bearing in mind, though, that following Anaplan’s IPO in late 2018, its share price surged last year by a market trouncing 125%. Clearly, the growth-oriented SaaS company has fans on the Street.

Bellini is among them. Despite lowering year-over-year revenue growth estimates for CY20 from 34% to 22%, the 5-star analyst sees the company’s software as “best in class” and reckons churn will remain low due to “the strategic nature of its software”.

The numbers are encouraging, too. In the company’s latest quarterly statement, total revenue grew by 42% to reach $98.2 million – including a 50% year-over-year increase in subscription revenue totaling $89.5 million.

Bellini further added, “We continue to view Anaplan as well positioned despite an expected impact of COVID-19 on its results this year. We see its planning software as helping companies to become more well run and increase their agility as they benefit from a connected planning process. With a growing number of global systems integrators expanding their practices on its software, we see its ability to bounce back from expected spending dislocations faster than many others.”

Bottom line, what is the implication for investors? Bellini maintains a Buy rating, but the price target is reduced from $68 to $51. From current levels, the potential upside is still a plentiful 56%.

As for the rest of the Street, PLAN’s Moderate Buy consensus rating is based on 5 Buys and 3 Hold ratings. With an average price target of $51.25, the analysts foresee upside of 56%. (See Anaplan price targets and analyst ratings on TipRanks)

Dropbox Inc (DBX)

Compared to the two previous names on Bellini’s list, Dropbox stock has fared far better in regards to the coronavirus’ eviscerating effect. While tech stocks have plunged all around it, DBX’s share price has weathered the storm so far, with a year-to-date loss of less than 1%. Looking further back, though, since its IPO in May 2018, DBX stock has been in decline. Does its current resilience in the face of the coronavirus indicate a bottom has been met? Not according to Bellini.

At Goldman, DBX gets a downgrade from Neutral to Sell along with a price target haircut – trimmed from $23 to $17. The negative sentiment is based on “contraction in peer multiples, increased macroeconomic risk and heightened competition”, and the new target implies further downside of 4%.

There are a number of reasons Bellini cites as back up for the negative thesis. For starters, Dropbox is heavily reliant on SMBs (small to medium sized businesses). These are the companies that will be most heavily affected by the viral outbreak. Individual plans make up 65% of Dropbox’s paying users and 60% of ARR (annual recurring revenue.) Last May’s 20% price hike won’t help matters, either, as smaller businesses could move to cheaper offerings such as Microsoft’s OneDrive (bundled in with Office365), or another rival in an increasingly competitive landscape with lower priced alternatives.

Bellini concluded, “While the new Dropbox does create the possibility to drive incremental subscriber adds alongside the ability to advertise potential upsell and cross-sell opportunities, efforts remain in early innings and we believe this ultimately expands the potential set of competitors in an increasingly crowded landscape. Since the February market peak, DBX has traded 3%-plus versus an average 16% decline across our coverage universe, and we believe risk/reward skewed to the downside from current levels.

What does the Street have in mind for the file hosting specialist? 5 Buys, 2 Holds and 2 Sells all add up to a Moderate Buy consensus rating. Other Street analysts differ from Goldman not only in rating criteria, but in price targets, too, as the average price target hits $25.57, and implies potential upside of 44% in the coming months. (See Dropbox price targets and analyst ratings on TipRanks)