Health Check: How Prudently Does China City Infrastructure Group (HKG:2349) Use Debt?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about. It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, China City Infrastructure Group Limited (HKG:2349) does carry debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for China City Infrastructure Group

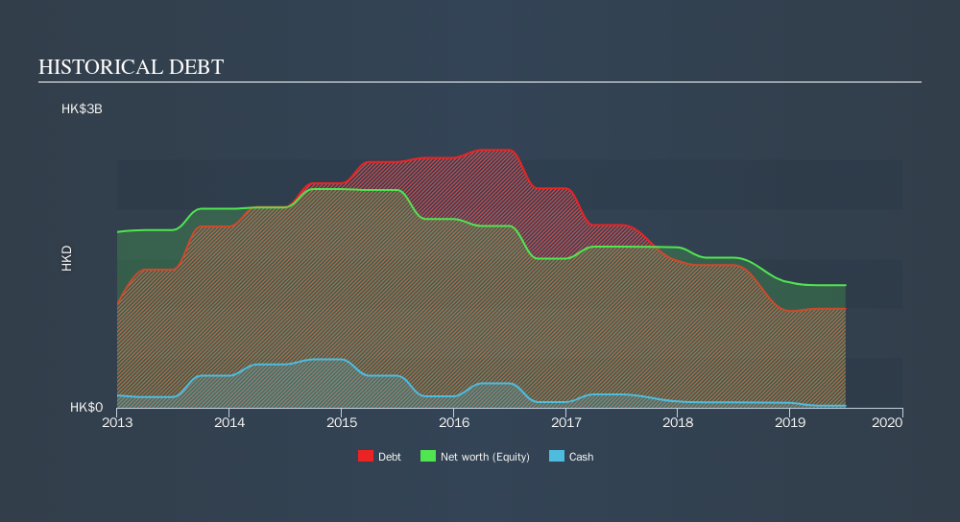

What Is China City Infrastructure Group's Net Debt?

You can click the graphic below for the historical numbers, but it shows that China City Infrastructure Group had HK$995.2m of debt in June 2019, down from HK$1.43b, one year before. However, it does have HK$22.0m in cash offsetting this, leading to net debt of about HK$973.2m.

A Look At China City Infrastructure Group's Liabilities

We can see from the most recent balance sheet that China City Infrastructure Group had liabilities of HK$795.0m falling due within a year, and liabilities of HK$871.5m due beyond that. Offsetting this, it had HK$22.0m in cash and HK$350.7m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by HK$1.29b.

The deficiency here weighs heavily on the HK$625.7m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet." So we'd watch its balance sheet closely, without a doubt After all, China City Infrastructure Group would likely require a major re-capitalisation if it had to pay its creditors today. When analysing debt levels, the balance sheet is the obvious place to start. But it is China City Infrastructure Group's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, China City Infrastructure Group made a loss at the EBIT level, and saw its revenue drop to HK$120m, which is a fall of 81%. To be frank that doesn't bode well.

Caveat Emptor

Not only did China City Infrastructure Group's revenue slip over the last twelve months, but it also produced negative earnings before interest and tax (EBIT). Indeed, it lost HK$52m at the EBIT level. Considering that alongside the liabilities mentioned above make us nervous about the company. We'd want to see some strong near-term improvements before getting too interested in the stock. It's fair to say the loss of HK$144m didn't encourage us either; we'd like to see a profit. In the meantime, we consider the stock to be risky. For riskier companies like China City Infrastructure Group I always like to keep an eye on whether insiders are buying or selling. So click here if you want to find out for yourself.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.