Here's Why Alaska Air Group (NYSE:ALK) Has A Meaningful Debt Burden

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Alaska Air Group, Inc. (NYSE:ALK) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Alaska Air Group

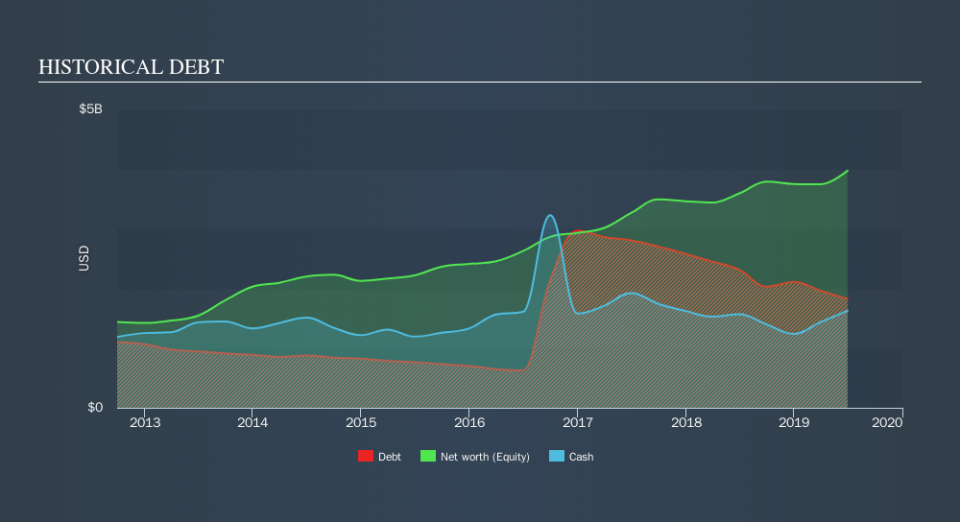

How Much Debt Does Alaska Air Group Carry?

The image below, which you can click on for greater detail, shows that Alaska Air Group had debt of US$1.83b at the end of June 2019, a reduction from US$2.31b over a year. However, because it has a cash reserve of US$1.63b, its net debt is less, at about US$199.0m.

A Look At Alaska Air Group's Liabilities

The latest balance sheet data shows that Alaska Air Group had liabilities of US$3.53b due within a year, and liabilities of US$5.44b falling due after that. Offsetting these obligations, it had cash of US$1.63b as well as receivables valued at US$389.0m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$6.96b.

This is a mountain of leverage relative to its market capitalization of US$7.96b. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Alaska Air Group's net debt is only 0.15 times its EBITDA. And its EBIT easily covers its interest expense, being 31.1 times the size. So you could argue it is no more threatened by its debt than an elephant is by a mouse. On the other hand, Alaska Air Group saw its EBIT drop by 6.4% in the last twelve months. That sort of decline, if sustained, will obviously make debt harder to handle. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Alaska Air Group can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Over the most recent three years, Alaska Air Group recorded free cash flow worth 50% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

While Alaska Air Group's level of total liabilities does give us pause, its interest cover and net debt to EBITDA suggest it can stay on top of its debt load. Looking at all the angles mentioned above, it does seem to us that Alaska Air Group is a somewhat risky investment as a result of its debt. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. In light of our reservations about the company's balance sheet, it seems sensible to check if insiders have been selling shares recently.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.