Here's Why Arrow Electronics (NYSE:ARW) Has A Meaningful Debt Burden

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Arrow Electronics, Inc. (NYSE:ARW) does carry debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Arrow Electronics

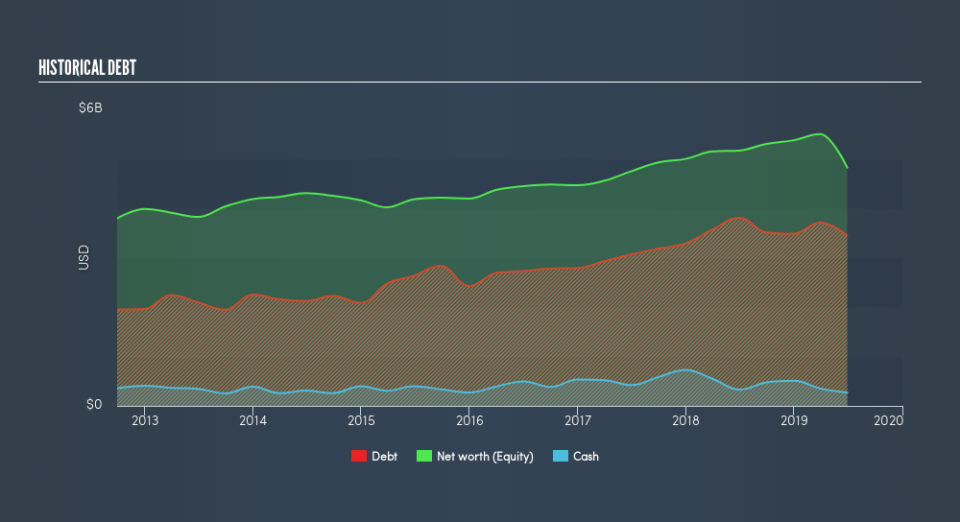

How Much Debt Does Arrow Electronics Carry?

The image below, which you can click on for greater detail, shows that Arrow Electronics had debt of US$3.45b at the end of June 2019, a reduction from US$3.81b over a year. However, because it has a cash reserve of US$270.0m, its net debt is less, at about US$3.18b.

A Look At Arrow Electronics's Liabilities

The latest balance sheet data shows that Arrow Electronics had liabilities of US$7.38b due within a year, and liabilities of US$3.82b falling due after that. Offsetting these obligations, it had cash of US$270.0m as well as receivables valued at US$7.98b due within 12 months. So its liabilities total US$2.96b more than the combination of its cash and short-term receivables.

This deficit isn't so bad because Arrow Electronics is worth US$5.63b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Arrow Electronics's debt is 2.6 times its EBITDA, and its EBIT cover its interest expense 4.9 times over. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. Unfortunately, Arrow Electronics saw its EBIT slide 4.5% in the last twelve months. If earnings continue on that decline then managing that debt will be difficult like delivering hot soup on a unicycle. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Arrow Electronics's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. In the last three years, Arrow Electronics created free cash flow amounting to 6.8% of its EBIT, an uninspiring performance. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Our View

Mulling over Arrow Electronics's attempt at converting EBIT to free cash flow, we're certainly not enthusiastic. But at least its interest cover is not so bad. Looking at the balance sheet and taking into account all these factors, we do believe that debt is making Arrow Electronics stock a bit risky. That's not necessarily a bad thing, but we'd generally feel more comfortable with less leverage. In light of our reservations about the company's balance sheet, it seems sensible to check if insiders have been selling shares recently.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.