Here's Why Cello Health (LON:CLL) Can Manage Its Debt Responsibly

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Cello Health plc (LON:CLL) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Cello Health

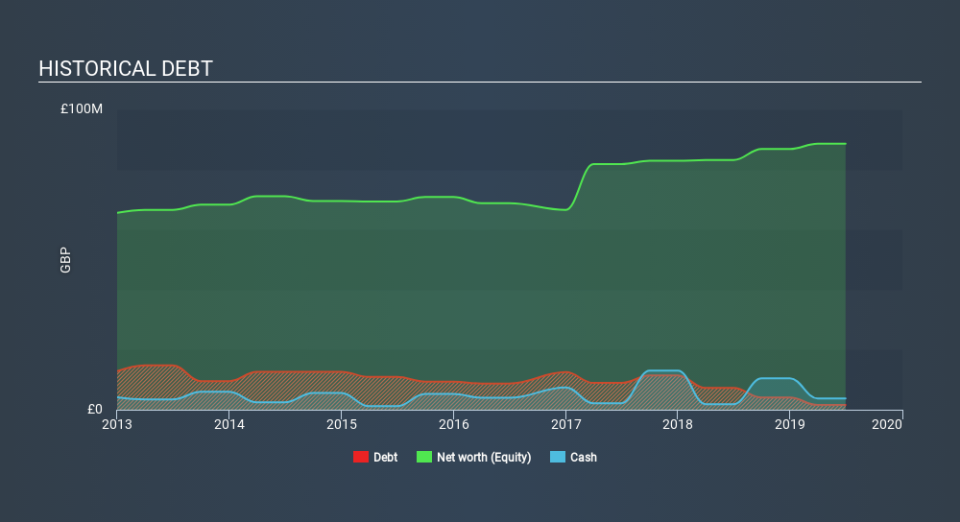

How Much Debt Does Cello Health Carry?

As you can see below, Cello Health had UK£1.57m of debt at June 2019, down from UK£7.29m a year prior. However, it does have UK£3.75m in cash offsetting this, leading to net cash of UK£2.18m.

How Healthy Is Cello Health's Balance Sheet?

The latest balance sheet data shows that Cello Health had liabilities of UK£37.5m due within a year, and liabilities of UK£11.1m falling due after that. Offsetting these obligations, it had cash of UK£3.75m as well as receivables valued at UK£43.1m due within 12 months. So it has liabilities totalling UK£1.72m more than its cash and near-term receivables, combined.

Having regard to Cello Health's size, it seems that its liquid assets are well balanced with its total liabilities. So while it's hard to imagine that the UK£139.7m company is struggling for cash, we still think it's worth monitoring its balance sheet. While it does have liabilities worth noting, Cello Health also has more cash than debt, so we're pretty confident it can manage its debt safely.

Fortunately, Cello Health grew its EBIT by 9.2% in the last year, making that debt load look even more manageable. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Cello Health can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Cello Health has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. In the last three years, Cello Health's free cash flow amounted to 33% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

Summing up

While it is always sensible to look at a company's total liabilities, it is very reassuring that Cello Health has UK£2.18m in net cash. On top of that, it increased its EBIT by 9.2% in the last twelve months. So we are not troubled with Cello Health's debt use. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of Cello Health's earnings per share history for free.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.