Here's Why I Think BigBen Interactive (EPA:BIG) Is An Interesting Stock

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Some have more dollars than sense, they say, so even companies that have no revenue, no profit, and a record of falling short, can easily find investors. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.'

So if you're like me, you might be more interested in profitable, growing companies, like BigBen Interactive (EPA:BIG). While profit is not necessarily a social good, it's easy to admire a business than can consistently produce it. Loss-making companies are always racing against time to reach financial sustainability, but time is often a friend of the profitable company, especially if it is growing.

See our latest analysis for BigBen Interactive

How Quickly Is BigBen Interactive Increasing Earnings Per Share?

As one of my mentors once told me, share price follows earnings per share (EPS). It's no surprise, then, that I like to invest in companies with EPS growth. Who among us would not applaud BigBen Interactive's stratospheric annual EPS growth of 55%, compound, over the last three years? While that sort of growth rate isn't sustainable for long, it certainly catches my attention; like a glint in the eye of my lover.

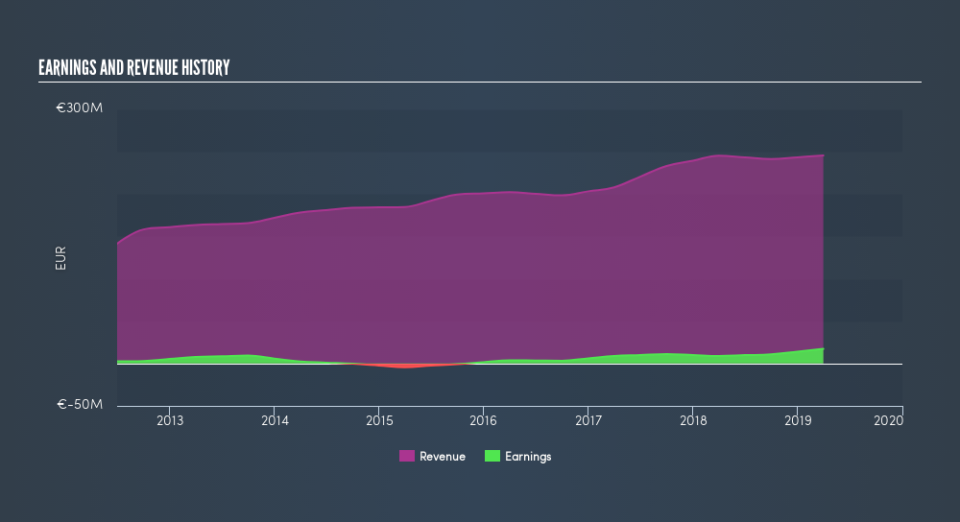

I like to see top-line growth as an indication that growth is sustainable, and I look for a high earnings before interest and taxation (EBIT) margin to point to a competitive moat (though some companies with low margins also have moats). This approach makes BigBen Interactive look pretty good, on balance; although revenue is flattish, EBIT margins improved from 6.2% to 8.8% in the last year. That's a real positive.

You can take a look at the company's revenue and earnings growth trend, in the chart below. To see the actual numbers, click on the chart.

The trick, as an investor, is to find companies that are going to perform well in the future, not just in the past. To that end, right now and today, you can check our visualization of consensus analyst forecasts for future BigBen Interactive EPS 100% free.

Are BigBen Interactive Insiders Aligned With All Shareholders?

It makes me feel more secure owning shares in a company if insiders also own shares, thusly more closely aligning our interests. So it is good to see that BigBen Interactive insiders have a significant amount of capital invested in the stock. Indeed, they hold €32m worth of its stock. That shows significant buy-in, and may indicate conviction in the business strategy. Those holdings account for over 14% of the company; visible skin in the game.

Should You Add BigBen Interactive To Your Watchlist?

BigBen Interactive's earnings per share growth has been so hot recently that thinking about it is making me blush. That sort of growth is nothing short of eye-catching, and the large investment held by insiders certainly brightens my view of the company. The hope is, of course, that the strong growth marks a fundamental improvement in the business economics. So yes, on this short analysis I do think it's worth considering BigBen Interactive for a spot on your watchlist. Of course, just because BigBen Interactive is growing does not mean it is undervalued. If you're wondering about the valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Although BigBen Interactive certainly looks good to me, I would like it more if insiders were buying up shares. If you like to see insider buying, too, then this free list of growing companies that insiders are buying, could be exactly what you're looking for.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.