Here's Why We Think Braime Group PLC's (LON:BMT) CEO Compensation Looks Fair for the time being

The share price of Braime Group PLC (LON:BMT) has increased significantly over the past few years. However, the earnings growth has not kept up with the share price momentum, suggesting that some other factors may be driving the price direction. Some of these issues will occupy shareholders' minds as the AGM rolls around on 23 June 2021. One way that shareholders can influence managerial decisions is through voting on CEO and executive remuneration packages, which studies show could impact company performance. In our analysis below, we show why shareholders may consider holding off a raise for the CEO's compensation until company performance improves.

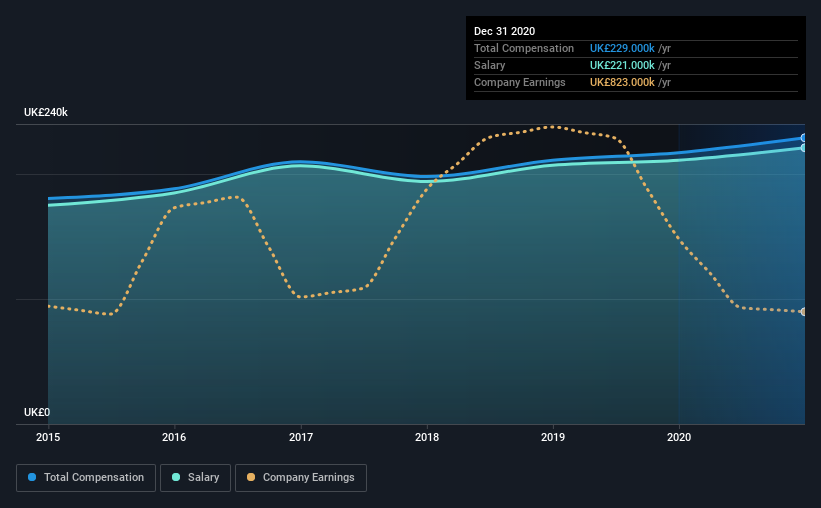

View our latest analysis for Braime Group

Comparing Braime Group PLC's CEO Compensation With the industry

According to our data, Braime Group PLC has a market capitalization of UK£33m, and paid its CEO total annual compensation worth UK£229k over the year to December 2020. That's just a smallish increase of 5.5% on last year. In particular, the salary of UK£221.0k, makes up a huge portion of the total compensation being paid to the CEO.

In comparison with other companies in the industry with market capitalizations under UK£142m, the reported median total CEO compensation was UK£236k. So it looks like Braime Group compensates Oliver Nicholas Braime in line with the median for the industry. Moreover, Oliver Nicholas Braime also holds UK£3.4m worth of Braime Group stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

Component | 2020 | 2019 | Proportion (2020) |

Salary | UK£221k | UK£211k | 97% |

Other | UK£8.0k | UK£6.0k | 3% |

Total Compensation | UK£229k | UK£217k | 100% |

On an industry level, around 61% of total compensation represents salary and 39% is other remuneration. Braime Group pays a high salary, concentrating more on this aspect of compensation in comparison to non-salary pay. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at Braime Group PLC's Growth Numbers

Over the last three years, Braime Group PLC has shrunk its earnings per share by 22% per year. Its revenue is down 1.9% over the previous year.

Few shareholders would be pleased to read that EPS have declined. This is compounded by the fact revenue is actually down on last year. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Braime Group PLC Been A Good Investment?

Most shareholders would probably be pleased with Braime Group PLC for providing a total return of 96% over three years. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

In Summary...

Oliver Nicholas receives almost all of their compensation through a salary. While the return to shareholders does look promising, it's hard to ignore the lack of earnings growth and this makes us question whether these strong returns will continue. Shareholders should make the most of the coming opportunity to question the board on key concerns they may have and revisit their investment thesis with regards to the company.

It is always advisable to analyse CEO pay, along with performing a thorough analysis of the company's key performance areas. In our study, we found 3 warning signs for Braime Group you should be aware of, and 1 of them is significant.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.