Here's Why I Think Propel Funeral Partners (ASX:PFP) Is An Interesting Stock

Some have more dollars than sense, they say, so even companies that have no revenue, no profit, and a record of falling short, can easily find investors. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses.

If, on the other hand, you like companies that have revenue, and even earn profits, then you may well be interested in Propel Funeral Partners (ASX:PFP). While profit is not necessarily a social good, it's easy to admire a business that can consistently produce it. While a well funded company may sustain losses for years, unless its owners have an endless appetite for subsidizing the customer, it will need to generate a profit eventually, or else breathe its last breath.

Check out our latest analysis for Propel Funeral Partners

Propel Funeral Partners's Improving Profits

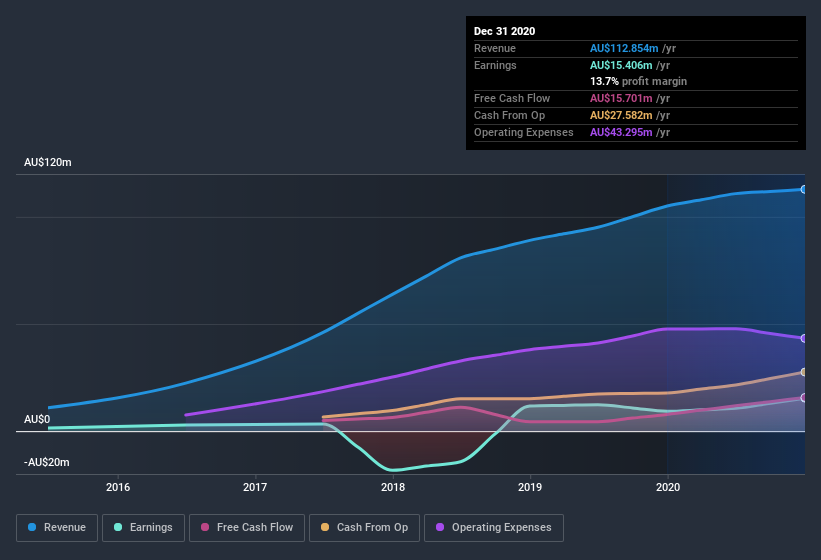

Over the last three years, Propel Funeral Partners has grown earnings per share (EPS) like young bamboo after rain; fast, and from a low base. So I don't think the percent growth rate is particularly meaningful. Thus, it makes sense to focus on more recent growth rates, instead. Like a falcon taking flight, Propel Funeral Partners's EPS soared from AU$0.094 to AU$0.16, over the last year. That's a commendable gain of 65%.

I like to take a look at earnings before interest and (EBIT) tax margins, as well as revenue growth, to get another take on the quality of the company's growth. The good news is that Propel Funeral Partners is growing revenues, and EBIT margins improved by 5.3 percentage points to 22%, over the last year. That's great to see, on both counts.

The chart below shows how the company's bottom and top lines have progressed over time. For finer detail, click on the image.

You don't drive with your eyes on the rear-view mirror, so you might be more interested in this free report showing analyst forecasts for Propel Funeral Partners's future profits.

Are Propel Funeral Partners Insiders Aligned With All Shareholders?

Like that fresh smell in the air when the rains are coming, insider buying fills me with optimistic anticipation. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. Of course, we can never be sure what insiders are thinking, we can only judge their actions.

Not only did Propel Funeral Partners insiders refrain from selling stock during the year, but they also spent AU$149k buying it. That's nice to see, because it suggests insiders are optimistic. Zooming in, we can see that the biggest insider purchase was by Head of Mergers & Acquisitions Fraser Henderson for AU$83k worth of shares, at about AU$2.78 per share.

The good news, alongside the insider buying, for Propel Funeral Partners bulls is that insiders (collectively) have a meaningful investment in the stock. Indeed, they hold AU$27m worth of its stock. That shows significant buy-in, and may indicate conviction in the business strategy. That amounts to 8.9% of the company, demonstrating a degree of high-level alignment with shareholders.

Is Propel Funeral Partners Worth Keeping An Eye On?

Given my belief that share price follows earnings per share you can easily imagine how I feel about Propel Funeral Partners's strong EPS growth. Not only that, but we can see that insiders both own a lot of, and are buying more, shares in the company. So it's fair to say I think this stock may well deserve a spot on your watchlist. It is worth noting though that we have found 2 warning signs for Propel Funeral Partners that you need to take into consideration.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Propel Funeral Partners, you'll probably love this free list of growing companies that insiders are buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.