Here's Why Venture (SGX:V03) Can Manage Its Debt Responsibly

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk. It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Venture Corporation Limited (SGX:V03) does carry debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Venture

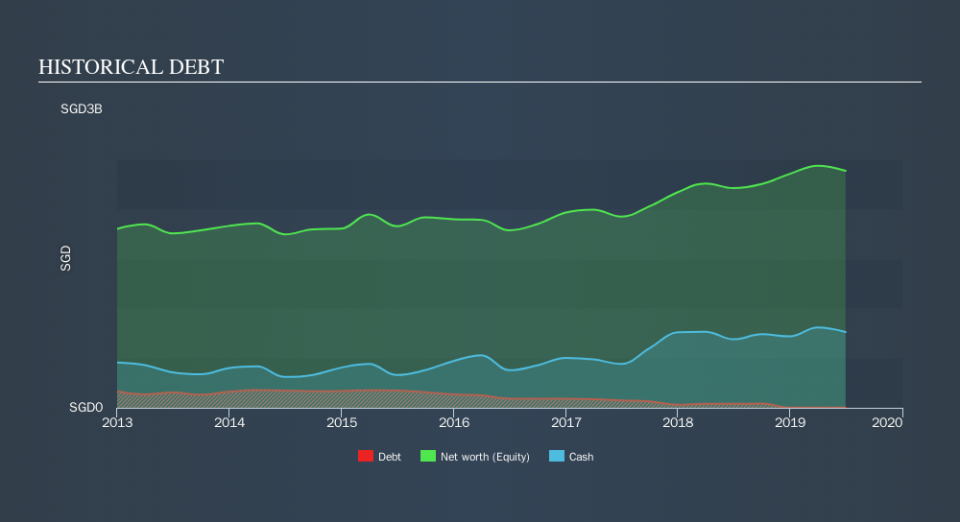

What Is Venture's Net Debt?

The image below, which you can click on for greater detail, shows that Venture had debt of S$1.57m at the end of June 2019, a reduction from S$41.7m over a year. However, its balance sheet shows it holds S$761.8m in cash, so it actually has S$760.2m net cash.

How Strong Is Venture's Balance Sheet?

We can see from the most recent balance sheet that Venture had liabilities of S$791.7m falling due within a year, and liabilities of S$11.2m due beyond that. On the other hand, it had cash of S$761.8m and S$761.0m worth of receivables due within a year. So it actually has S$719.9m more liquid assets than total liabilities.

It's good to see that Venture has plenty of liquidity on its balance sheet, suggesting conservative management of liabilities. Due to its strong net asset position, it is not likely to face issues with its lenders. Simply put, the fact that Venture has more cash than debt is arguably a good indication that it can manage its debt safely.

On the other hand, Venture's EBIT dived 15%, over the last year. We think hat kind of performance, if repeated frequently, could well lead to difficulties for the stock. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Venture's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Venture has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the most recent three years, Venture recorded free cash flow worth 76% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing up

While it is always sensible to investigate a company's debt, in this case Venture has S$760.2m in net cash and a decent-looking balance sheet. The cherry on top was that in converted 76% of that EBIT to free cash flow, bringing in S$308m. So is Venture's debt a risk? It doesn't seem so to us. Another positive for shareholders is that it pays dividends. So if you like receiving those dividend payments, check Venture's dividend history, without delay!

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.